- Date: 25th Oct 2016; IPO Period: 25-27th Oct

- IPO Price: Rs. 750-775; P/E 39.2 and P/B 2.45 times

- Mid Cap: Rs 12,800 crore Mkt cap

- Industry – Housing Finance NBFC

- Advice: Investors may BUY with a 1 year perspective

Summary

- Overview: PHF is the 5th largest housing finance company by loan portfolio. Over 5 years, PHF has implemented a business process transformation and re-engineering program, which contributed to them becoming the fastest growing large HFC in India. PHF’s revenue and PAT have grown 55.6% and 43.4% CAGR from FY12 to FY16. PHF’s loan portfolio also grew at 61.8% CAGR in this period. The operations have become broad based and cover North, West and South India quite equally.

- At a FY16 P/B post IPO of 2.45 times, the valuations are reasonable. The P/E at 39 (ttm) does look stretched but with good growth and margin expansion, this will stay in a good range.

- The risks that must be understood include high competition and a flat housing market.

- Opinion: As an investment, the PHF IPO is rated a medium risk, high return type of offering. Investors may BUY PHF with a 1 year perspective.

Here is a note on PNB Housing Finance (PHF).

IPO highlights

- This IPO opens: 25-27thOct 2016 with the Price band: Rs.750 – 775 per share.

- Shares offered to public number 3.87 cr. (UMP). The FV of each is Rs. 10 and market Lot is 19.

- Shares offered are 23.4% of equity. The IPO will collect Rs 3,000 cr. with a fresh issue of shares. The IPO shares are available to institutional, non-institutional and retail in ratio of 50:15:35.

- PNB Bank holds 51% stake of PHF, and 49% is held by Destimoney Enterprise Ltd (DEL). DEL got sold to Quality Investments Holding in Feb2015, an affiliate of the Carlyle Group, a global investment firm. Post IPO s’holding will be PNB 39%, DEL 38%, QIB 12%, retail 8% and NIB 3%

- PHF would benefit from the IPO as it is a fresh issue of shares. The IPO proceeds of Rs 3,000 cr. would improve capital adequacy of PHF and help fund the growth for the next few years.

Introduction

- PHF is the 5th largest HFC in India by loan portfolio and 2nd largest by deposits. PHF offers “housing loans” for the purchase, construction, extension or improvement of residential properties or for the purchase of residential plots, and “non-housing loans” in the form of loans against property.

- Over 5 years, PHF has implemented a business process re-engineering (BPR), and transformation program, which helped them become the fastest growing large HFC in India.

- Total income for FY16 was Rs 2,697 cr. and profit Rs 326 cr. The HFC’s AUM was Rs. 27,000 cr.

- PHF’s loan portfolio was at Rs 27,177 cr. in FY16, a 61.8% CAGR in 4 years. By June 2016, it further increased to Rs 30,900 cr.

- PHF’s has an operating model which includes branches (47) across the north, west and south of India, processing hubs (16) which include three co-located zonal offices and one central support office in New Delhi.

- Branches act as the primary point of sale and assist with origination, collection processes, sourcing deposits and enhancing customer service. The processing hubs and zonal offices provide support functions, such as loan processing, credit appraisal and monitoring, and their CSO supervises their operations nationally. There are totally 847 employees.

- In FY16, the sources of funds were NCD’s (33.5%), deposits (27.2%) and comm. paper (19.2%).

- Regional: the loan portfolio origination is from north – 39.7%, west 30.4% and south 29.9%.

- Leadership: Sanjay Gupta is MD; Jayesh Jain (CFO) and Shaji Varghese (Business Head).

Promoter (Punjab National Bank) – Snapshot and Financials

- PNB is a full service public sector bank. It provides a wide range of banking services such as digital banking, personal banking, social banking, micro, small and medium enterprises banking, etc.

- PNB operates through 4 segments: Treasury, Corporate/Wholesale, Retail and others.

- Income grew by 8.5% CAGR over 5 years. But PAT and EPS fell due to losses in Q4 FY16.

- Major cleansing had happened in the NPA books of PNB. The gross NPA of the bank increased by Rs. 30,000 cr. in 2015-16 to Rs. 55,818 cr., which was 12.9% of its gross advances. Net NPAs jumped to 8.61% as against 4.06%. The share price also corrected sharply. See Fig 4.

- There was a weakening in the balance sheets of many banks over FY11-15. Some of this was RBI driven, as the policy focus was to clean the books of all banks.

- However post this IPO PHF will no longer be a subsidiary of PNB, so we downplay the influence and effects of PNB as a promoter. In fact PNB products portfolio does overlap with that of PHF already.

News and Updates for PHF

- The BPR undertaken by PHF over 4-5 years included investments in a scalable operating model, an integrated infotech platform, centralization and standardization of back-end processes, the hiring of experienced personnel and subject matter experts, hikes in salaries and other employees benefits, the refurbishment of offices, and repositioning of the “PNB Housing” brand.

- PHF has a strong distribution network with over 7,110 channel partners across different locations in India, including the in-house sales team, external direct marketing associates, deposit brokers and national aggregator relationships with reputed brands. In recent months they sourced 56.5% of new loans from their in-house channels and the rest from external sources.

- Currently PHF’s housing loans constitute 70.3% of total loan portfolio and retail constituted 86.5% of the housing loan portfolio. The average loan size (at origination) of the retail housing loans was Rs 31.8 lakh, with a weighted average loan-to-value ratio of 66.1%. The loan size of retail non-housing loans is Rs 56.8 lakh, with a weighted average LTV ratio of 46.5%.

- Total borrowings are Rs 30,045 cr. and average cost of borrowings was 8.65%. During the same period the spread was 1.93% and the cost to income ratio stood at 25.03%.

- PHF’s gross NPAs as % of total loan portfolio were 0.2% in FY15 and 0.27% as of June 2016, which was the lowest among the leading HFCs in India. Also the overall Capital to Risk (Weighted) Assets Ratio (“CRAR”) and Tier I Capital CRAR were 13.04% and 8.4%, resp.

- PHF is planning to grow in Indian tier-II and tier-III. From the present 48 branches at 28 locations, they will expand to 60 more locations with a population of more than 80-90 lakhs.

- PHF received high credit ratings for deposits, long-term loans, NCDs (secured & unsecured) and commercial paper from agencies like CRISIL, ICRA, CARE and India Ratings (Fitch). This helped raise low cost deposits in high volumes.

- PHF had raised Rs.500 cr. in April 2016 from International Finance Corporation (IFC) by issuing secured fixed rate non-convertible debentures (NCDs) to fund green residential projects.

- As of June 2016, 12.6% & 87.4% of the portfolio were fixed & variable interest rate loans, resp.

- PHF selected AuthShield in Aug 2016 as a security installation to safeguard customers accounts. With hacking cases, better security has become vital for financial service providers.

- The unofficial/ grey market premium for this IPO is in the range of Rs 50 – 52. This is a positive.

Indian Housing Finance Industry Outlook

- In India, the housing industry is significant contributor to the country’s development and GDP.

- Total outstanding housing loans in FY15 were Rs 11.3 lakh crores, a 17.7% increase since FY11.

- Still, India has a low mortgage-to-GDP ratio. As of FY15, India’s mortgage-to-GDP ratio was 9% compared to China 18%, Thailand 20%, Germany 45% and USA 62%. (CRISIL/ RHP).

- Banks held 63% of the housing finance market in FY15, based on loan assets. The higher market share of banks is due to big networks, broad customer bases and relationships.

- The key growth drivers in the housing finance industry in India include:

- Low mortgage penetration and housing shortage;

- Urbanization; Population growth and changes in demographics.

- Slowing average loan ticket size growth; Tax benefits and

- Government implemented schemes (including Smart Cities and Housing for All by 2020)

- The NHB was established pursuant to the NHB Act to operate as a principal agency and statutory body to promote housing finance institutions and to provide financial and other support to such institutions. The NHB is wholly-owned by the RBI. Under the provisions of the NHB Act, it regulates how HFCs conduct business in India. Through its refinance schemes, the NHB has made cumulative disbursements (from its inception until June 2014) of Rs 1,204 bn.

- In the last 15 years, the total outstanding housing loans of HFCs and banks has increased at a CAGR of 23.4% from Rs 439 bn in FY00 to Rs 10,205 bn in FY15.

- Among lenders, HFCs have better capitalised on the demand in non – metro cities, and grew their disbursements by 20.1% YoY. By contrast, banks’ advances grew at 14% YoY.

- The distinguishing feature of the housing loan portfolio in India is the low NPA level, which is partially the result of financiers’ adequate appraisal systems and effective recovery mechanisms, as well as greater information availability. In FY15, the gross NPA level for HFCs in housing loans was estimated at 0.5% while it was slightly higher for banks, at 1.6%.

- NPAs are likely to decline marginally in FY16 and FY17 owing to economic recovery, lower interest rates, better control, system checks, follow-ups, and improvement of job security.

- The housing finance market in India is forecast to grow 20-22% over FY15 to FY20.

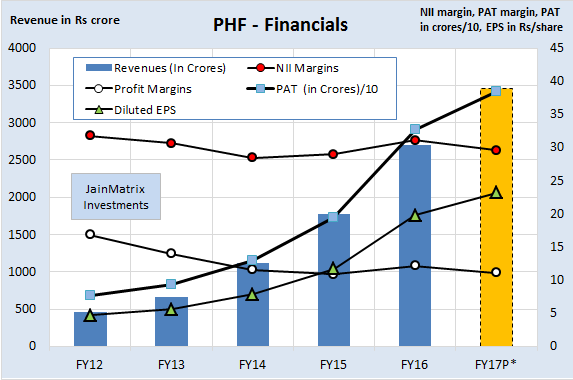

Financials of PHF

- PHF’s revenue and PAT have grown 55.56% and 43.41% CAGR from FY12 to FY16. (Note: The projected FY17 data is a simple extrapolation from the Q1 FY17 results, see Fig 5).

- The revenue growth is high, as is absolute PAT over FY12-16. We can see that the diluted EPS has grown at a slower pace. This is because of a flat to falling NII and Profit Margins in this period. In addition, there have been several dilutions to the equity base since FY12.

- PHF has a ROE of 17.6% (FY16) which is good, however not the best in the industry.

- We have assumed an IPO dilution of equity base to 16.56 crore shares to recalculate EPS in Fig 5. In addition, since the IPO premium will flow into the balance sheet of PHF, we recalculated the Book Value post IPO at the upper end of price band. The BV increases to Rs 316/share. Basis these, the P/E will be 39.19 times FY16 earnings and the P/B will be 2.45 times.

- The dividend has been rising – PHF declared dividend of Rs 3.4 in FY16, a yield of 0.44% which is low. The dividend growth rate has been moderate at 11.5% CAGR from FY12 to FY16.

- Net interest margin has improved from 2.93% (FY14), 2.94% (FY15) to 2.98% (FY16).

- The NHB directions require HFCs to comply with a CRAR where an HFC’s Tier I and Tier II capital may not be less than 12% of sum of HFC’s risk-weighted assets and the risk adjusted value of off-balance sheet items. As of June 30, 2016, PHF’s CRAR was 13.04%. This is low, but will be boosted by the IPO.

Benchmarking

We benchmark PHF against listed housing finance, microfinance and BFSI peers. See Fig 6.

- PHF appears to have high valuations in terms of PE. But in terms of P/B, the IPO will add to the net worth of the company and make the P/B very reasonable at 2.45 times.

- PHF has the highest sales and PAT growth among peers, a positive. EBITDA margins are high.

- But profit margins are on the lower side. RoE too looks low. Dividend yield is low too.

- PHF will use the IPO to augment its capital base so post IPO capital adequacy will improve.

- PHF has moderate margins. PHF has a low RoE in the industry. PHF has a low dividend yield (0.44%) amongst its peers which is a negative.

Positives for PHF and the IPO

- High growth in revenues & profits for PHF combined with low NPAs is a wonderful combination.

- PHF is the 5th largest HFC in India and the fastest growing among large HFCs. It has also broad based its growth equally across North, West and South India.

- The Punjab National Bank brand is strong and rubs off feelings of confidence and trust. PHF has a PSB brand but is a well-managed private sector HFC, so it may have the best of both worlds.

- PHF has a strong distribution network with penetration of key Indian urban centers. It also has a very efficient employee workforce with just 847 employees.

- It has a scalable operating model and centralized and streamlined operational structure.

- It is managed by experienced and qualified professionals with strong industry expertise. Many from top management have held senior positions at leading banks and NBFCs.

- The 5 year financial performance of the company is outstanding with strong revenue, EPS and PAT growth. Clearly it is a growth stock and is placed well in a high potential industry.

- The RBI has reduced interest rates in recent quarters. In this scenario, with transmission to home loan customers, the loan products become more attractive and demand grows rapidly.

- The weak performance by PSBs in the last year was due to high NPAs and an attempt by the regulator to clean the books of banks. PSBs look weak, loss making and undercapitalized, and GoI is not in a position to fund them back to health. We may actually be seeing a massive permanent loss of market share by PSBs to private – banks, HFCs and NBFCs. This of course benefits PHF.

Risks and Negatives for PHF and the IPO

- The recent crackdown by GoI on black money and tax evaders has resulted in housing prices going flat to negative across India. Its possible that housing prices are artificially high in relation to income levels and the related housing rental market. We may be at the start of a multi-year price correction. This could affect housing loan demand for PHF.

- The pricing and valuations of PHF look stretched in comparison to peers. The P/E of 39 times (of post IPO capital base and FY16 EPS) is high. However a more critical parameter is P/B and at 2.45 times post IPO, this is reasonable. See Exhibit 6.

- The growth rate of PHF over the past 5 years may be difficult to continue over the next 5 due to high competition from banks and HFCs, and the natural high base effect.

- Margins appear low for PHF compared to peer group. This is acceptable with high revenue growth rates, but if growth slows down, PAT will slow sharply and affect perceived valuation.

- The banking sector offered limited competition to HFCs with few new licenses given by RBI. However this is changing with RBI doling out 20+ new licenses to Payment Banks and Small Finance Banks. See article New Banks: Big Changes In Small Change. RBI is also moving towards Bank licenses on tap in future. This can intensify competition over the years for PHF.

- A slowdown in economic growth in India or global economic instability could result in an adverse effect on their business, financial condition and results of operations.

Overall Opinion and Recommendation

- India’s housing sector will remain high growth for many years given low penetrations. The best way for investors to play this opportunity has been through HFCs. Their stocks have done exceedingly well over the last decade. Regulatory, tax and interest environments are also benign for HFCs.

- The BFSI industry is a proxy to the overall economy, and one can expect, as a thumb rule, the industry to grow at 2-3 times the GDP growth. The Indian economy is growing at 7-7.5%, so the HFC sector may see a 20%+ p.a. growth over the next few years.

- In this space, PHF has over the last five years implemented a business process transformation and re-engineering program with very strong growth from a small base. The firm looks quite capable of expanding to new locations and continuing the high growth momentum.

- At a FY16 P/B post IPO of 2.45 times, the current valuations are reasonable. The P/E parameter at 39 does look stretched but with good growth and margin expansion, this will stay in an acceptable range.

- There are a few risks that must be understood, like higher competition and flat housing prices.

- We feel this offering is attractive for investors. As an investment, the PHF IPO is rated a medium risk, high return type of offering.

- Investors may BUY PHF with a 1 year perspective.

JAINMATRIX KNOWLEDGE BASE

See other useful reports:

- Balmer Lawrie – Is Traveling Fast Now

- Endurance Technologies IPO

- ICICI Prudential Insurance IPO – An Expensive BUY

- GNA Axels IPO

- L&T Technology Services IPO

- RBL Bank IPO

- New Banks: Big Changes in Small Change

- Equitas IPO – Leader in SF Banks

- Dilip Buildcon IPO

- Do you want to be a value investor?

- Mahanagar Gas IPO

- How will Brexit impact Indian investors?

- A Repurpose for our PSUs

- How to Approach the Stock Market – A Lesson from Warren Buffet

- Thyrocare IPO – Wellness for your Wealth

- Announcement – SEBI approval as a Research Analyst

- Alkem Labs IPO

- Goods And Services Tax (GST): Integration And Efficiency

- Syngene IPO: Good Pharma R&D spinoff from Biocon

- Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

DO YOU FIND THIS SITE USEFUL?

- Visit the Investment Service offering page to find how you can get more.

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no known financial interests in PNB Housing Finance Ltd. or any group company. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.