Tag: equity research

-

-

The Four SuperTrends that Indian Investors must know

The Indian economy is undergoing massive changes. On one hand the GDP growth recently accelerated to over 7.8% in Q3FY26. Capex budgets are increasing. Spending on infra and transportation is rising. MNCs are setting up Global Competency Centers in India at a record pace. On the other hand, we have the Indian Rupee weakening against…

-

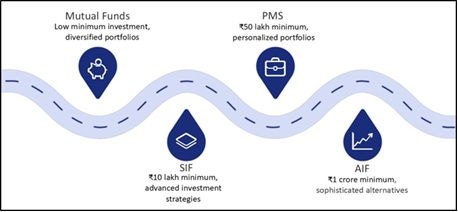

SIF – An Exciting Product Innovation from MFs

Summary: Specialised Investment Funds (SIF) are a new SEBI introduced investment category that bridges Mutual Funds and PMS/AIF. They offer advanced investment strategies, smaller minimum investment, greater flexibility, and a regulated structure, making SIF an interesting new investment product. Here is a deep dive into this new category. Introduction to SIFs Specialized Investment Funds (SIFs)…

-

CMI IPO – Self Sufficiency in Fuels – Buy

IPO highlights Introduction News, Updates and Strategies Industry Overview Market Trends: Financial Performance and Stock Evaluation Overall, CMI’s financials reflects strong profitability, efficient capital utilization, and stable operations. SWOT Analysis Benchmarking CMI is compared with peers in engineering, consultancy, project & analytical services. See Fig 4b. Opinion, Outlook and Recommendation Disclaimers and Disclosures

-

Indian REITs & InvITs Sector – Investment Report

A short video about our recent reports Disclaimers and Disclosures

-

Schneider Electric Infra Ltd. – March 2026

Investors, Here is a message regarding Schneider Electric from JainMatrix Investments. Report dated 27th Feb 2024 This report was published for Subscribers initially, and is released now for public viewing. The analysis, and the price target, are still valid. Summary Here is an investment research report on Schneider Electric Infrastructure Ltd (SEIL). SEIL – Description…

-

JainMatrix announcement

As an Indian investor, you need to safeguard your portfolio and investment expenses. You should only engage with certified and approved advisers, mutual funds, research analysts and market intermediaries. One initiative by SEBI is the creation of @valid UPI IDs to help investors identify genuine and approved parties, and make payments to them through proper…