Here is an Industry report on the Indian Automobile sector. It’s a sector that suffered weak sales post covid, but has recovered quite sharply in the last few months. The growing confidence and global growth plans of Indian auto firms can see the rise of many Indian auto MNCs in the next few decades. We recommend investors buy an Auto portfolio of Escorts Ltd., Eicher Motors, Bajaj Auto, Hero Motocorp, and Maruti Suzuki.

We make our Dec2020 Auto sector report public for your investing pleasure and success.

Additional sector reports: Eicher Motors – It’s Firing On Both Engines

Hero Motocorp – A Splendid Core Holding

Introduction

- The automobile industry of India is in the top 5 markets in the world. It is one of the driving forces of the Indian economy, contributing 49% to the mfg. GDP and 7.5% to overall GDP. The sector’s value chain employs about 3.2 crore people, directly or indirectly.

- The auto sector can be divided into four sub-segments: Passenger cars, Two- Wheelers, Tractors and Commercial Vehicles (PC, 2W, TT and CV). The segment shares by volume is depicted in Fig. 1

- 2W and PC dominate the domestic Indian auto market. Passenger car sales are dominated by small and mid-sized cars. 2W and PCs together had a combined sale of over 2.01 crore vehicles in FY20.

Sector Market Shares

- The brand which dominates in the 2W segment is Hero MotoCorp having 36% market share, as depicted by Fig. 2a. In the case of TT, it is (M&M) Mahindra and Mahindra (41.17%), see Fig 2b.

Fig 2a and 2b – Market share by firms – 2W and Tractors; Fig 2c and 2d – PC and CVs

- In the PC Vehicles, it is Maruti Suzuki (51.30%), Fig 2c, and in case of CVs, it is M&M with a market share of 35.04%, Fig. 2d.

- Electric Vehicles – In the year 2020 the electric vehicle market in India took off. The Auto Expo 2020 in Feb saw the introduction of many EVs of different sizes and prices from the automakers. The models that were soon commercially launched were Tata Nexon EV, Morris Garages ZS EV and Mahindra eVerito. M&M also launched the Mahindra eKUV100 at the Auto Expo 2020 and has priced the car from ₹8.25 lakhs making it the most affordable electric car in India.

- The shift of industry towards electric vehicles has brought uncertainty in the sector. Govt. goal of 100% electrification in auto industry has open doors for the new products in India.

- However, electrification is the initial phase in India. EVs may find it difficult to grow significant share without 1) Tax benefits from GoI 2) an EV make, charge and repair ecosystem 3) the entry of luxury EV products from Tesla, JLR (Tata Motor) and Audi, that can make the products attractive.

Auto Industry Updates

- Auto exports reached 47.7 lakh vehicles in FY20, growing at a CAGR of 6.94 % during FY16-FY20. 2W were 73.9% of vehicles exported, PCs were 14.2%, three wheelers at 10.5% and CVs at 1.3 %.

- In Nov’20, FM announced the ₹2 lakh crore production-linked mfg. incentives (PLI) to encourage companies in 10 sectors to boost local mfg. and increase exports. The auto sector, including vehicle makers and parts suppliers, will receive the biggest share at ₹57,000 cr. The export-related revenue and localization of production are the two primary criteria for benefits.

Fig 3 – Sector Wise Sales

- The Corona pandemic caused a 2020 slowdown of Auto Industry, which was already been performing poorly in FY20. In FY21 auto companies are expected to have weaker sales numbers. Trading tension between India and China, can also affect the Industry, as 27% of auto parts are and imported from China. Indian mfg firms are looking for alternative to Chinese imports.

- Millennials don’t prefer owing a car due to high maintenance cost and availability of local taxi rides.

- Fig 3 explains the sales pattern of four sub-sectors of automobile sector for the period of five financial years. Figure clearly depicts that Indians preferably choose two-wheelers. Every sub sector has seen a downfall in FY20 after the increase in the recent years.

- Two Wheelers – India is the largest mfg. of 2W in the world. 2W market has grown rapidly for Indians because of convenience and low cost of ownership and is expected to grow at a CAGR of 7.33%. Recently, industry has seen a downturn due to rising fuel prices, safety concerns, BS-VI norms and covid uncertainties. Motorcycle consisted of around 65% of the total 2W sales in the FY20, followed by Scooters and Mopeds with contribution of 32% and 3% respectively.

- 2W sales in India reached an all-time high in 2019, when they sold some 2.1 crore units. This figure is almost double the 2011 sales, when just 1.18 cr. two-wheeler units were sold in India.

- Passenger Cars – In Nov’20, India’s domestic PV sales rose 12.73%, due to ease in lockdown restrictions & increase in demand due to festive season. Maruti Suzuki has been a dominant player in PV sector, owning a market share of more than combined of all the rivals. Motor vehicle sales in India have doubled between 2008 and 2018, but has been seeing downward trend recently. Various regulatory norms have impacted the automobile sector to change their production methods leading to increase in cost.

- Commercial Vehicles – In 2018, India was the world’s 3rd largest CVs market and the fastest growing globally. Various factors affect the sales of CVs i.e., mfg. and agricultural output. India has faced the shift of emission standards from BS IV to BS VI from April 2020 leapfrogging BS V, a move that is aimed to curb threatening levels of air pollution in urban areas. Many CV mfg firms are looking to adopt EV tech, keeping the future developments in consideration. Majority of the CVs are Load Carrier Light CVs (LCVs) followed by Medium & Heavy CVs (M&HCVs).

Fig 4 – Tractor Market

- Tractors – The tractors market is quite dependent on the seasonal rainfall, overall GoI MSP and pricing, and demand conditions. This year has been positive for agriculture sector with good rainfall (in fact floods in some areas), firm GoI pricing and otherwise healthy demand. The migration of workers from urban to rural in May-June this year also helped in labour availability. The rural economy was relatively unaffected by lockdowns and covid. See Fig 4 – Tractor Market.

- The tractor market was impacted by closure of dealerships, but rebounded well by June itself.

- The new trend is development and export of cutting edge new tractors from India.

Why is Auto sector doing well in India?

- The sector has grown on account of traditional strengths in mfg., and cost advantages of abundant low-cost skilled labor, and significant foreign direct investment (FDI) inflows.

- The GoI has allowed 100% FDI under the automatic route. The GoI aims to develop India as a global mfg. center and a R&D hub. Under NATRiP, the GoI is planning to set up R&D centers at a cost of US$ 388.5 m to enable the industry to be on par with global standards.

- With a population of more than 130 cr. people, the addressable market for vehicle sales is large. A growing working population and expanding middle-class have been the demand drivers for auto in India. We have the second largest road network in the world at 4.7m km. The GoI policy to set aside substantial investment layout for infra development in every 5-year plan has included the focus on roads. This has given a fillip to the demand for cars and other vehicles.

- The global auto industry has embraced digital. Revenues generated by online vehicle retail, after-sales, and services are likely to grow almost five times, from about $120 billion in 2018 to about $605 billion by 2025. Volkswagen launched the Digital Workplace initiative across its dealerships in India around two years ago.

- There are various developments in Indian Auto sector which has triggered its growth. In Sept 2020, Toyota Kirloskar Motors announced investments of more than ₹2,000 cr. in India directed towards electric components and technology for domestic customers and exports. Also, M&M signed a MoU with Israel-based REE Automotive to collaborate and develop commercial EVs. In April 2020, TVS Motor Company bought UK’s iconic sporting motorcycle brand, Norton, for a sum of about ₹153 cr., making its entry into the top end (above 850cc) segment of the superbike market.

- India has engineering and design centers for many global auto firms. Here maintenance and upgrade work of current models as well as planning & engineering work for new launches, and product development work is done by skilled engineers in an IT enabled environment in close coordination with teams in many countries. Thus an auto ecosystem has developed in India of skills, local manufacturing, OEMs, components, and global business centers.

- India also has various cost advantages. Auto-firms save 10-25% on operations vis-à-vis Europe and Latin America. India has a well-developed, globally competitive Auto Ancillary Industry and established automobile testing and R&D centers.

- India is a prominent auto exporter and this segment may grow in the near future.

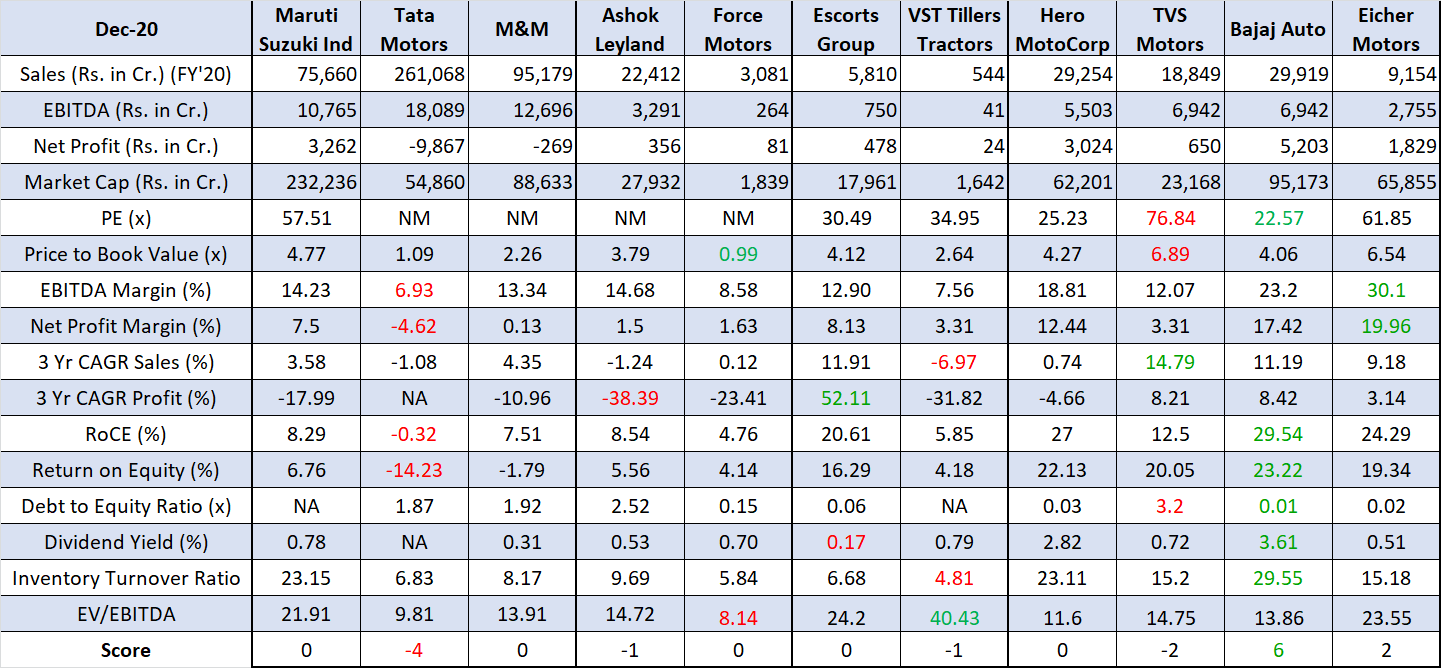

Benchmarking of Key Players

We have done a benchmarking of selected Auto sector players. Fig. 5 depicts the comparison between the selected Indian companies on basis of key parameters.

Fig. 5 – Benchmarking

- In this peer group, Bajaj Auto showed best returns (ROCE & ROE) & even dividend yield, and is the lowest in terms of debt as well as being undervalued. Eicher Motor and Escorts were not far behind.

- Profitability was negative in FY20 for Tata Motors & Mahindra and 3 year cagr profit is negative for many firms. The leader on this parameter is Escorts.

- Margins are the best for Eicher Motor and next for Bajaj Auto. Eicher Motor has operations in niche high margin segment while Bajaj clearly shows once again its efficiency in operations.

- Among these auto companies, the best positive outcomes and Score are of Bajaj Auto and Eicher Motors in two-wheeler segment, Escorts in Tractors and Maruti Suzuki in Passenger Car segment. TVS Motors and Tata Motors appear weak from this group.

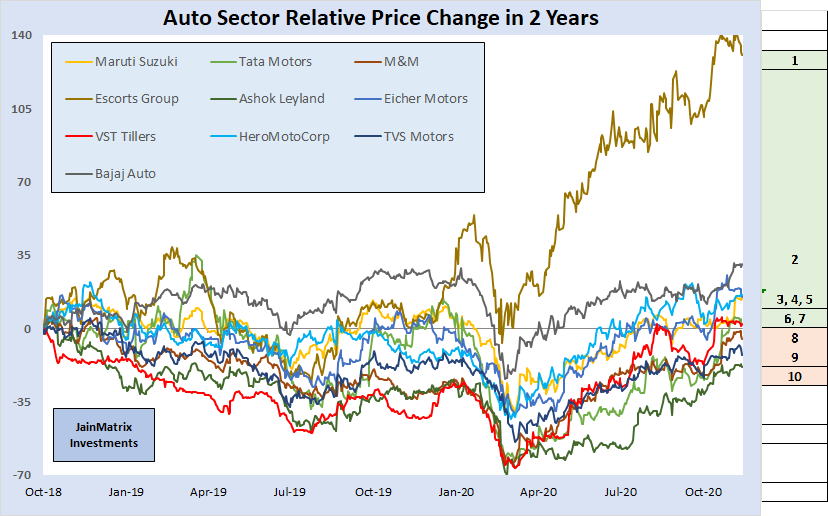

Relative Prices

Fig 6 – Relative Prices

- Fig 6 – Relative Prices shows the stock returns given by major listed Indian auto firms by keeping the base of prices as 29th Oct 2018. On the right side we can see the share price performance by order.

- The share prices fell sharply when the first lockdown started, but soon had a V-shaped recovery. We can see that 7 of the 10 firms have emerged in the positive by now, over a 2 year period.

- Escorts Group is the #1 in this group and has posted high returns of 140% gains. The agriculture sector has done well even in lockdown times and there has been a good rainfall too. Escorts Group has been increasing its market share by launching new models recently.

- In the group #2 is Bajaj Auto, #3 is Eicher Motors, #4 is Hero Motocorp, and #5 is Maruti Suzuki. Relative underperformers are Ashok Leyland, Tata Motors and TVS Motors.

Future of the Indian Auto Industry

- A young population, rising GDP and growing middle class will drive domestic demand for automobiles in India. This will be aided by a healthy domestic industry that is innovative and producing at scale.

- Several Indian automobile firms have global expansion plans for sales, mfg. and exports. These include Eicher Motors, Hero Motocorp and Bajaj Auto. Maruti, Hyundai and Escorts among others use India facilities for exports.

- India is expected to emerge as the world’s third-largest PC market by 2021. In FY 2018-19, sale of PC has increased by 2.70%, 2W by 4.86% and 3W by 10.27% as compared to FY 2017-18.

- From just small cars, India will grow as a hub for design, components and mfg. of all automobiles.

- Auto companies like Kia Motors, MG have entered the Indian market with premium vehicles and are making a mark by selling in higher volumes. Many automotive companies are looking to enter the business in India which can result in cut-throat competition, and will push Indian companies to innovate and increase the quality of their product to retain their market share.

Conclusion

- Automobile sector will continue to grow in India due to rising domestic demand, growing strengths in outsourcing of engineering services to India, and global growth plans of Indian OEMs. The supporting ecosystem of auto component manufacture too is developing in tandem.

- The weak INR may help India to be a good base for manufacture and global exports.

- In 2W India is already #1. In the PC and CV categories, India became the #4 largest market in 2019 displacing Germany with about 3.99 m units sold. India may displace Japan for #3 by 2021.

- The growing confidence and global growth plans of Indian auto firms can see the rise of many Indian auto MNCs in the next few decades.

- The key new auto sector trends of digitalization, software based auto controls and EVs can also be accelerated by India based R&D and developer firms.

- We can see from Fig 5 – Benchmarking and Fig 6 – Relative Prices that 6-7 firms out of the selected 10 for this study are performing well on many parameters and should continue to lead.

- We recommend investors buy an Auto portfolio of Escorts Ltd., Bajaj Auto, Eicher Motors, Hero Motocorp, and Maruti Suzuki in equi-weight mode.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Punit Jain has stock ownership positions in Escorts Ltd. (since Feb 2017) and Eicher Motors (since June 2017) out of all firms mentioned in this report, and they are small (<1%). Other than this, JM has no known financial interests in any firm mentioned here. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JM at punit.jain@jainmatrix.com.

Leave a comment