- Date 01st Dec; IPO Opens 2-4th Dec, at ₹59-60/share

- Small Cap: ₹ 2,438 cr. Mkt cap

- Sector – Restaurant chain, QSR

- Valuations: P/E negative, P/B 10.5 times, EV/EBITDA 4.4.

- Loss making entity; profit looks 2 years away, so this is a private equity type, high risk investment

- Advice: SUBSCRIBE

Summary

- Why Buy Now: The Burger King chain is at an early stage of growth in India. The organization and structure set up looks good to handle the growth imperatives.

- The Burger King brand is quite strong in India.

- We expect profitability in BKG in 2 years, by FY23, even as it grows rapidly in revenues and outlets. Once this happens, BKG valuations will rise and this IPO entry price will look attractive.

- Relative to other MNC QSR chains in India, BKG valuations look reasonable.

- It has handled the covid period well, reducing costs and getting by. We expect normalcy in revenues to return in H2FY21.

- Risks: 1) Loss making entity; profitability looks 2 years away, so this is a private equity type, high risk investment 2) Intense competition from Indian and MNC QSR chains in Tier 1 towns 3) Covid induced challenges – demand from customers as well as employee health. 4) High royalties to Principal.

- Opinion: Investors can SUBSCRIBE to this IPO with a 2 year perspective.

JainMatrix Subscription Pricing and Payment Options

JainMatrix Investments reports….

Here is a note on Burger King India IPO (BKG) IPO.

IPO Highlights

- The IPO opens from 2-4th Dec 2020 in a Price Band of ₹ 59-60 per share

- The IPO includes a Fresh Issue of ₹ 450 cr. and Offer for Sale (OFS) of 6 cr. shares. So the total IPO size is max 810 cr. of about 13.5 cr. shares, and about 35.5% of the equity share capital.

- The promoter is QSR Asia and it owns 94% in BKG which will fall to 60% post-IPO.

- The main objects of Fresh Issue are funding new Company-owned Burger King Restaurants by 1) Repayment of borrowings taken for this of ₹ 165 cr. and 2) Capex for new Restaurants ₹ 177 cr. 3) Remaining ₹ 108 cr. are for general corporate purposes like paying for this IPO.

- The promoter is a PE firm and the listing will help to monetize and profit from investments.

- The lot size is 250 shares and Face Value ₹ 10 per share

- The IPO share quotas for QIBs: Non-Institutional Investors: Retail is 75:15:10%.

- The unofficial/ grey market premium of BKG is ₹ 20-25 /share over IPO price. This is a positive.

Introduction

- Burger King India is one of the fastest growing international QSR (Quick Service Restaurant) chains in India, started in Nov 2014.

- In FY20 the Revenues, EBITDA and Profits of BKG were ₹ 847 crore, ₹ 105 cr. and ₹ (77) cr. resp.

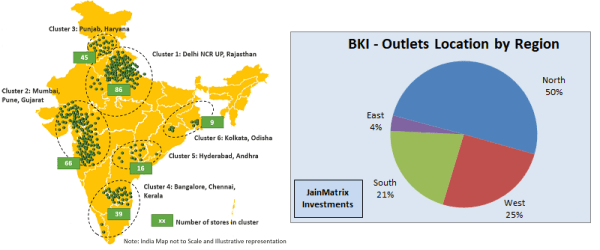

- It already has 261 restaurants across 57 cities, including Delhi-NCR, Mumbai, Pune, Chennai, Hyderabad, Bengaluru, Chandigarh and Ludhiana.

- The restaurants serve food and beverages, see Fig 1a, with offerings like:

Fig 1a – Menu Range, Fig 1b – Cluster Map and Fig 1c – Outlets by Region

- The globally recognized Burger King brand, also known as the “HOME OF THE WHOPPER®”, was founded in 1954 in USA and is owned by Burger King Corp., a subsidiary of Restaurant Brands Intl. Inc. The Burger King brand is the #2 largest fast food burger brand globally by number of restaurants, with a network of 18,000 restaurants in 100 countries and USA.

- BKG has used a well defined restaurant roll out and development process. The Principal (BKG AsiaPac) helps and supports in this process.

- BKG AsiaPac has to be paid monthly royalty (of 4-5% of sales annually). BKG is also required to pay BKG AsiaPac a non-refundable one-time fee on opening each new BK Restaurant of US$15k (₹11.25L), increasing to $25k (19L) from CY 2020-22 and US$35k (26L) for all periods thereafter.

- Everstone Capital, the Singapore-HQ India-focused mid-market PE firm, owns 99.39% stake in BKG India, through investment vehicle QSR Asia Pte Ltd.

- As of Sept 30, the number of BKG employees was 4,836.

- Key leaders: Shivakumar Pullaya Dega (Chairman and Independent Director), Rajeev Varman (CEO and Whole Time Director) and Abhishek Gupta (Chief of Biz. Dev. and Operations).

News, Updates and Strategies

- Burger King India aims to have 370 stores (101 additional) by Dec 2022. Under the Master Franchise and Development Agreement (MDA), BKG is required to develop and open 700 restaurants (both Company-owned and Sub-Franchised) by Dec 2026. This agreement renewal is by Dec 31, 2039.

- Fund raising through the IPO will be used for expanding its store base in India and reducing debt.

- The Indian promoter is a private equity firm Everstone Capital, even as BKG works under a MDA with Burger King Corp. USA.

- Based on the FIFO methodology, Everstone will earn 3.58 times returns on its 7-year investment. Its cost of investment (of the IPO shares) is pegged at ₹ 110 cr. In return, it will fetch ₹ 360 cr. from the partial exit at upper end of IPO band, per VCCircle.

- The company’s average meal ticket size is ₹ 500-550.

- Covid had a massive impact on BKG, as first a lockdown, and later the containment zones, lack of permission from authorities and public fear of infection kept away dine in customers.

- BKG responded by reducing costs: it negotiated with landlords on rentals, reduced inventories, etc.

- In Sept 2020, the number of BKG employees decreased to 4,836 employees compared to 6,141 in Mar due to attrition, effect of Covid, and redundancies.

- On date of RHP of 25th Nov., out of 268 total restaurants, only 249 are operational.

- BKG has a strong supply chain for all food ingredients and raw materials, to ensure traceability, freshness, long term contracts, low prices and quality ingredients.

Food Industry Outlook in India

- The Indian food service sector can be divided into 4 segments, see Fig 2.

- QSR have fast food cuisines and minimal table service, and cater to youngsters and working professionals, offering quick delivery of food, good ambience and option of home delivery. QSRs generally target people in the 16-35 years range. Frequency of eating out (4-5 per month) is low so there is headroom to grow.

- QSRs are the most preferred destination, followed by casual dining restaurants when it comes to eating out, per the India Food Services Report 2016, made by the National Restaurants Association of India (NRAI) and consulting firm Technopak Advisors Pvt. Ltd.

- The most popular eating out options in India are North Indian food (28% of the time), followed by Chinese (19%) and South Indian style (9%), according to a Livemint.com report.

- Restaurants, cafes and international fast food outlets have proliferated in India and eating out has become popular. About 81% of consumers prefer to eat out, and 19% get delivery or takeaway.

- The QSR segment is nascent and has a lot of scope for growth in India. A large number of global QSRs have established their outlets with franchise rights of various companies like McDonalds, KFC, Pizza Hut, Subway, Taco Bell, Burger King and Domino’s, in addition to Indian QSRs.

- BKG has a 5% market share in India’s ₹ 34,800 crore QSR market.

- With factors such as urbanization, rising income levels and improved investment climate, the food service sector holds a huge opportunity. The sector has observed tremendous development in the past 3 years, which grew at 11% CAGR during 2015-19. The sector is estimated to grow at a 9% CAGR by 2022-23 (Source: NRAI India Food Services, IFSR 2019).

- GST rate cut from 18% to 5% for the restaurant business was a significant tailwind for the sector, and generally led to a sharp recovery in SSSG’s.

Financials of BKG

- BKG revenues, EBITDA and PAT over the years are in Fig 3a. The firm grew revenues well over 3 years, and is EBITDA positive but loss making.

- A possible profit in FY21 quickly became a loss in H1 due to Covid.

- In Fig 3b we can see that from a FCF positive FY18, the firm has made many investments and become FCF negative in FY19-20. We can also see the number of outlets by FY.

Fig 3a – BKG Financials and Fig 3b – Free Cash Flow

Benchmarking

We benchmark BKG against listed food service firms, entertainment firms and the principals. See Fig 4.

Fig 4 – Benchmarking

- As a loss making firm, PE is negative for BKG. So valuations are tracked using P/B and EV/EBITDA. On these parameters, the valuations of BKG are lower than the others. This is positive.

- Sales growth has been good at BKG. On Profits BKG is in the negative.

- D/E ratio is low, may fall after IPO. One of the objects of the fresh issue in IPO is to reduce debt.

- Margins are still on the lower side as BKG is building scale for its operations.

- Return ratios are low due to losses.

- The Revenue per outlet is low, perhaps reflecting BKG is a newer restaurant chain.

- Putting this together, we sense that BKG is an asset available at low valuations due to current losses. It’s entirely possible that if not for covid, BKG may have been much less lossmaking by now. Post covid, BKG should focus on growth, with branch expansion, brand building and consumer loyalty.

Positives for BKG and the IPO

- Burger King is a strong global brand. It’s been handled well so far in India with high street, airport and malls locations of restaurants, good visibility and positive customer reviews.

- As a customer, my visit to BKG in 2018 in Bangalore was memorable and the focus is excellent with burgers available in both veg. and non veg. It was tasty and fairly priced, and a good experience.

- The core offering of burgers can work for both snacks and meals for the Indian palate. Traditional consumers may not be satisfied as it’s a light fried meal, but others can find it novel and tasty. The BKG brand is well positioned for the millennial customers.

- The global franchise model has succeeded for competitors in Indian markets, and the BKG rollout looks like a lower risk proposition that has a fairly unique offering and good chance of success.

- The growth plans of 700 outlets by 2026 looks achievable and necessary to get a scale of operations.

- The firm has an experienced, passionate and professional management team

- Due to the covid infection, BKG has been able to bring down its costs structures. In particular, real estate costs for QSR may reduce and stay low for some time. Employee nos too have reduced.

- BKG has an MDA with Burger King USA is till 2039, giving a good visibility.

Risks & Negatives for BKG in the IPO

- The covid pandemic has been a blow as BKG has switched from a growth mode to a ‘cutting costs’ and survival mode for H1, to get by during this dip. Even today after most of the outlets reopened, there is a demand issue as customers are worried about public gatherings and infection spread. The economic impact of covid means that people celebrate less and even eating out may be done at more ‘economic’ or ‘reasonable’ priced outlets than BKG. At the luxury end, demand is down.

- Having said this, our opinion is that in T1 cities, demand will normalize in Q3FY21 and a combination of takeaway and home delivery should be able to bring demand back.

- BKG has not declared a profit so far in all these years. As a result, the IPO has been allowed by SEBI but the Retail portion is retained at the lowest, 10% of shares offered, due to higher risks.

- So on PE we have a negative value, but on other valuation parameters like PB and EV/EBITDA, BKG looks attractive and undervalued.

- BKG directly competes with McDonalds and Subway in India on bread based light food options. Thus this QSR food subcategory looks a little crowded and top heavy.

- BKG is at an early growth phase in its Indian network. There is a possibility that it may take several years to make a profit or dividend as it opens new outlets and invests in branding and supply chain.

- Investors looking for normal valuation parameters may not find this attractive. Conversely this investment may only give good gains over several years.

- Food delivery aggregators like Swiggy and Zomato intensify competition by offering massive choice and delivery to customers. BKG partners with them, but they get large commissions on orders.

- Royalties for BK USA are high and a big hurdle to franchisee profitability. In FY18-20 they were ₹ 12, 24 and 34 crores for BKG.

Overall Opinion and Recommendation

- QSR has a good future in India with improving affluence, and a growing eating out culture. Beyond the FY21 covid blip, this category should grow fast.

- The social type businesses like BKG have been hardest hit by covid. As a result, the BKG IPO offering is undervalued. Most stock investors today are ignoring H1FY21 results, and high but temporary valuations, and expecting a full recovery by H2.

- On a big picture basis, BKG is at an early stage of growth in India. The organization and structure set up looks good to handle the growth imperatives.

- We expect profitability in BKG in 2 years, by FY23, even as it grows rapidly in revenues and outlets. Once this happens, BKG valuations will rise and this IPO entry price will look reasonable.

- Risks: 1) Loss making entity. Profitability also looks 2 years away, so this is a private equity type, risky investment opportunity. 2) Intense competition from Indian and MNC QSR chains in Tier 1 towns 3) Covid induced challenges – demand from customers as well as employee health. 4) High royalties.

- Opinion: Investors with a risk appetite can SUBSCRIBE to this IPO with a 2 year perspective.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake ownership or financial interests in BKG or any group company. Punit Jain intends to apply for this IPO. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

Leave a comment