JainMatrix Investments presents an Industry report on the Indian IT Services sector. It’s a sector that is growing at 8-10% annually and has significant share in global outsourcing. An ecosystem of good college education and a large pool of talent, feed a clutch of globally competitive Indian IT Service firms. The digital demand has only grown post-covid, so the industry is looking at many years of global growth in early double digits. See the Conclusion section for our recommended IT Services portfolio.

We make our 11th Jan 2021 IT Services sector report public for your investing pleasure and success.

Additional sector reports: Happiest Minds IPO – Ride the Digital Wave – Sept 2020

LT Tech Services IPO – The Make in India Firm – Sept 2016

Introduction and Profile

- Indian IT services industry started over 30 years ago, but is now very large with revenues US$ 191 billion (INR 14 lakh crores). About 81% of revenues are from exports. See Fig 1a.

- It has 17,000 firms & is an emerging global hub for Digital Skills, with 75% of global digital resources.

- IT Services have contributed 7.7% to the India GDP in 2019 which is expected to grow to 10% by 2025 (IBEF). In FY19, the industry employed 41 lakh people. It is also fueling innovation, as there are around 5,300 tech start-ups in India.

- Exports rose at a CAGR of 8.05% during FY16-19. Export of IT services has been the major contributor, accounting for 54% of total IT export (including hardware) during FY19.

- Globally, the sector is headed towards achieving USD 1 trillion (INR 75 lakh crores) of revenues by 2022.

Fig 1a – Market Size in India and Fig 1b – Share of Demand by Country

- USA dominates global Country Share of demand, with EU, China and Japan coming next, see Fig 1b.

- In Fig 1b, market share of Indian IT industry looks small but this is domestic demand in USD. India is a dominant supplier of IT services globally and has the fastest growing industry in the world with most key players having a HQ or development centers here.

- BFSI is a key business vertical for IT & BPM industry, in terms of major revenue-share. Adoption of new technologies is needed for growth & competitive advantage in Banking & Insurance domain.

- Other important sectors are Life Sciences & Healthcare, Retail & CPG, Communications & Media, Manufacturing, Telecom and Technology & Services.

- Indian IT industry’s USP is cost competitiveness, good skills, resource availability and project management skills for providing IT services.

- Tier II and III cities are gaining traction among IT firms aiming to grow business in India, facilitated by skilled local resources, affordable real estate, favorable Govt. regulations, tax breaks and SEZ schemes. A hub and spoke model is developing with Tier I city as hubs and tier II, III and IV as spokes.

- India is a top location for Global Capability Centers (GCCs), which concentrate on workers and infra to handle operations (back-office, corporate business-support, accounting & finance, transaction processing and contact centers) and IT support (app. development and maintenance, remote IT infra, and help desks), to enhance productivity. Some large companies use GCCs as a center of excellence for innovation and research.

- About 70% of India-based GCCs belong to US companies, 20% European and 10% Asia-Pacific.

- According to Nexdigm, India is home to over 1,750 GCCs, which is 50% of all such centers globally. GCCs here employ over 10L employees, generating a total economic value of around $28.3 billion.

- IT Services in India are growing at a fast pace due to the globally competitive firms that provide world-class services. The Human talent pool available in India is highly skilled and trainable, a key strength of the IT Services sector. The IT infra here has also developed to global standards.

IT Sector Progress and News

- NASSCOM (National Assn. of Software & Services Cos.) launched an online platform to up-skill 40 lakh tech professionals. It partnered with GE Healthcare for digital healthcare solutions for the market.

- IT service firm DXC Technology, will set up its first global analytics unit in Bengaluru.

- Govt. of India (GoI) announced a national program on AI (artificial intelligence) and a new National AI portal. GoI has identified IT as one of 12 champion service sectors for developing an action plan. It has set up a ₹5,000 crore ($ 745 m) fund for realizing the potential of these champion service sectors.

- As of Feb’20, there were 421 approved SEZs (Special Economic Zone) across the country, and of these, 276 are from IT & ITeS. These provide tax incentives for exports. Software Technology Parks of India (STPI) has set up 57 centers for single window clearance and infra facilities, and for Excise Duty exemptions on buying local goods.

- Technology for many businesses was considered a support function. This has changed as tech. has become business critical, enabling employee productivity, revenue growth from eCommerce, cost savings and faster customer support & communication.

- TCS took the #1 spot with M-cap of $144 b among IT Services organizations, dethroning Accenture which is trailing by just $1b (Dec ‘20).

Impact of Covid

- In Q1FY21, Indian IT sector has emerged as a winner post lockdown. With Work from Home (WFH) at 95%, all the big IT firms saw robust demand from clients, particularly cloud & automation. Infosys gained in revenue and profits; IT index gained 22% in July. Similarly in Q2FY21, IT sector gained due to increased tech spending by clients in digital transformation.

- Due to automation, spending on IT infra has outpaced HR. Job creation has been limited with offers being rolled out more on contractual basis than full-time, in both emerging & developed markets.

- Many firms found that WFH employees are equally productive & this saves real estate costs as well. It also relieves firms of covid related responsibility and litigation.

- IT Deals – Indian IT stocks jumped by 50%, on an average, between Mar-Sept ’20. Top IT firms have been closing deals – Infosys closed 2 big deals, Vanguard and Consolidated Edison (digital transformation); TCS won deals from Phoenix Group (life insurance and pension) for client analytics tool, and Morrisons (retail); Wipro from Marelli (auto software engg.) and HCL Tech from Ericsson.

- Broker comments: Girish Pai of Nirmal Bang said that global clients shifted spending from internal IT, selling, general and administrative (SG&A) and hardware, to outsourcing and digital, to speed up the digital transformation processes such as migration to cloud.

- Motilal Oswal, a brokerage firm, said that demand & utilization has normalized to pre-Covid levels with discussions being revived for deferred deals and margins expected to be resilient as well.

Relative Price Performance

- The graph in Fig 2 – Relative Share shows the stock returns given by listed Indian IT Services firms over Oct’18 – Jan’21.

- We can see that performance was steady for these firms till early 2020 in a +25 to -10% ranges, then there was a sharp fall due to Covid. Recovery came by July’20 and in next 6 months there was a dramatic price rise for many of them.

- On the right side we can see the resultant share performance by order for the 2+ years.

- Among large caps, L&T Infotech is #1, marked L1, Infosys #2, HCL Tech #3 and next are Wipro #4, TCS #5 and Tech Mahindra #6. Among mid-caps, the rankings are Persistent is #1, marked M1, others are Mindtree #2, Mphasis #3, LTTS #4 and Sonata Software #M5.

- Even so, the entire IT Services pack has performed very well as even the lowest performance was 42% gains over 2+ years, while the highest is an amazing 179% gain.

Fig. 2 – Relative Share Price

Large Cap Firms – Benchmarking and Sales Charts

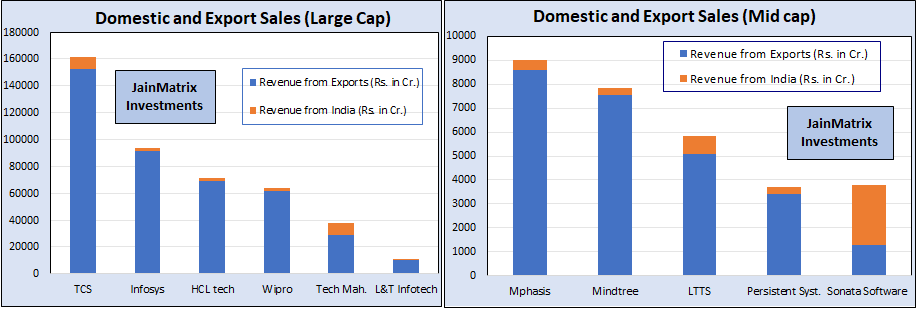

Fig 3a – LC revenue and Fig 3b – MidCap

In Fig 3a we map the FY20 revenues for Large Cap Firms. Revenue from exports is the major source.

- TCS has the highest sales by value, almost two-fold to the nearest competitor Infosys.

- In terms of India revenues, Tech Mahindra has the highest domestic sales followed by TCS.

Fig 4a – LC Benchmarking

- In Fig. 4a – Benchmarking, we compare large cap IT services firms on key financial parameters.

- The leader is marked in green and the laggard in red. The sum total of these parameters is the Score.

- We can see that TCS is a clear leader, including RoCE and Return of Equity, while Wipro lags on this comparison amongst 6 large cap firms. L&TI however appears as a growth and profit leader.

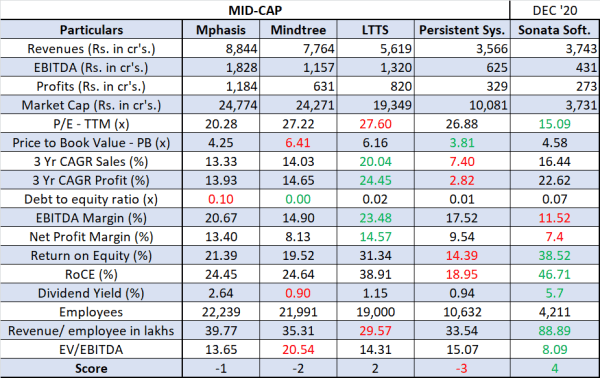

Mid-Cap Firms – Benchmarking and Sales Charts

- In a similar manner, we compare mid cap IT services firms. In Mid-cap basket, Sonata is the leader on financial parameters, including RoCE and RoE, whereas Persistent lags among the 5 firms.

Fig. 4b – Mid-caps Benchmarking

- Among mid-caps, Mphasis has the highest revenues or sales, followed by Mindtree.

- Sonata Software has the highest domestic sales by value and proportions.

- Fig 4b above captures the MidCap firms revenue by domestic and exports.

Future of the Indian IT Services Industry

- The comparative advantages of the country are – young population, good college education and ample science and technical courses. These feed this sector with quality resources.

- India is developing as a critical part of execution and delivery of global business and IT Services, across industries & locations. Firms like TCS are covering more countries & expanding the market.

- The growth of Telecom networks like 2G-4G and now 5G are bringing the world closer.

- Covid has actually accelerated the rise of digital, eCommerce, internet and the IT Services industry. As larger firms enforced WFH for their employees’ safety, the physical presence has become unnecessary for work, for large swathes of industry.

- TCS as the #1 firm globally in terms of market capitalization has been able to sustainably mix high margins, high growth and a global vision. The other firms in the industry are growing in its wake and developing their own niches and strengths.

- The industry is looking at many years of global growth in early double digits, even as IT services take early baby steps of growth in its own backyard, India. With programs like Aadhar card, UPI payments, GST, digital tax filing and FASTag, technology is proving the best way to transact at scale with speed and transparency, and also reduce corruption.

- The success of the Indian IT Services firms has spawned the second generation of services firms such as Syngene Intl. (pharma R&D) and Tata Elxsi & LTTS (Engineering R&D) which are niche services players by technology or industry.

- The key new IT services trends are WFH, cloud services, AI, IoT, robotics, mobile apps and machine learning.

Conclusion:

- IT Services firms are always going to be needed to stitch together solutions for large Enterprises, and to help them navigate, evaluate and deploy in complex IT landscapes with multiple technology options.

- Indian IT services companies have time and again proven their mettle and have the skilled resources and project management skills to deliver successfully. It is a dynamic, globally focused sector.

- The 11 firms had an excellent share price performance range of 42% to 179% gains over 2+ years.

- The weak INR may help India to continue to be a good base for service delivery teams and exports.

- Large Caps: A LC IT Services portfolio will be more stable and safer for investors. We conclude from Fig 2, Fig 3a, and Fig 4a that of the 6 LC firms, the best 3 are L&T Infotech, TCS and Infosys.

- Mid-Caps: A MidCap IT Services portfolio will be more volatile, but possibly provide better returns. We can see from Fig 2, Fig 3b and Fig 4b that of the 5 LC firms, the best 2 are Mindtree and LTTS.

- We recommend investors to buy this 5 firm portfolio in an equi-weight mode.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Punit Jain has equity holdings in LTTS, Sonata Software, TCS and L&T Infotech, all <1%. Punit Jain has worked at TCS (1995-2002) and in Sonata Software (2003-2012). Other than this, JM has no known financial interests in any of these firms. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JM at punit.jain@jainmatrix.com.

Leave a comment