Tag: JainMatrix Investments

-

Laser Power IPO: A Good Conductor: Video

We share a short video of this IPO. Summary IPO highlights Introduction to Laser Fig 1a – Products of Laser Download the PDF report here – Disclaimers and Disclosures Punit Jain discloses that he has no shareholding in Laser, or any group company. In addition, JainMatrix Investments Bangalore (JMI) and its promoters/ employees also have…

-

Laser Power IPO: A Good Conductor

See Update with Video on Laser Power IPO Summary IPO highlights Introduction to Laser Fig 1a – Products of Laser Download the PDF report here – Disclaimers and Disclosures Punit Jain discloses that he has no shareholding in Laser, or any group company. In addition, JainMatrix Investments Bangalore (JMI) and its promoters/ employees also have…

-

-

-

The Four SuperTrends that Indian Investors must know

The Indian economy is undergoing massive changes. On one hand the GDP growth recently accelerated to over 7.8% in Q3FY26. Capex budgets are increasing. Spending on infra and transportation is rising. MNCs are setting up Global Competency Centers in India at a record pace. On the other hand, we have the Indian Rupee weakening against…

-

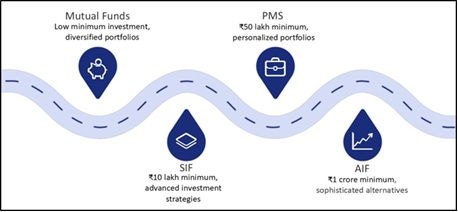

SIF – An Exciting Product Innovation from MFs

Summary: Specialised Investment Funds (SIF) are a new SEBI introduced investment category that bridges Mutual Funds and PMS/AIF. They offer advanced investment strategies, smaller minimum investment, greater flexibility, and a regulated structure, making SIF an interesting new investment product. Here is a deep dive into this new category. Introduction to SIFs Specialized Investment Funds (SIFs)…

-

CMI IPO – Self Sufficiency in Fuels – Buy

IPO highlights Introduction News, Updates and Strategies Industry Overview Market Trends: Financial Performance and Stock Evaluation Overall, CMI’s financials reflects strong profitability, efficient capital utilization, and stable operations. SWOT Analysis Benchmarking CMI is compared with peers in engineering, consultancy, project & analytical services. See Fig 4b. Opinion, Outlook and Recommendation Disclaimers and Disclosures