- Date: 3rd April 2016

- IPO price range Rs 109 – 110, Apply from 5-7th Apr 2016

- Industry: BFSI – Small Finance Bank

- Mid Cap: Rs 3,560 cr Mkt Cap

- Advice: BUY

![]()

Summary

- Overview: Equitas Holdings is a financial services firm that has extended beyond microfinance to MSME, CV and housing loans to people that are underserved by formal financing channels.

- Equitas had revenues of Rs 756 cr. and profits of Rs 107 cr. in FY2015. The topline and PAT have grown by 56.1% and 39.2% respectively CAGR over the last four years.

- Why BUY: 1) Equitas has a good record of business so far, in terms of growth, segment diversification and profits. 2) In terms of valuations, Equitas has priced the shares attractively, leaving something on the table for investors.

- Key risks: are geographic concentration and impending SFB structural changes.

- Retail Investors can BUY this IPO.

Here is a note on Equitas Holdings Limited (Equitas)

IPO highlights

- The IPO is open from 5-7th Apr 2016 with Issue Price band: Rs.109-110 per share

- It will raise Rs 2,177 cr. totally, as Offer for Sale (1457 cr.) and fresh issue (720 cr.)

- No of Shares offered to public are 19.8 crore of Face Value: Rs.10. These are 59.07% of the equity base, and include OFS from shareholders (13.2 cr.) and a fresh issue (6.6 cr.).

- Market Lot: 135 shares and in multiples of 135 shares there off

- Objects of the issue are – reduction in foreign shareholding – In Sept 2015, the firm received approval from RBI for a small finance bank. But foreign shareholders held 93% of the firm. As per the current FDI policy, the foreign investment in a private bank will be a maximum of 49%. So the IPO will help reduce foreign stake to below 49%. It will also provide an Exit opportunity for current shareholders.

- The funds raised in the fresh issue (Rs 720 cr), would be used to set up the Small Finance Bank (Rs 620 cr), set off the IPO expenses, and extend loans to the subsidiaries (Rs 100 cr.).

To download the PDF version of report, proceed to bottom of this page.

Introduction to Equitas

- Equitas is a financial services firm into microfinance, MSE Finance, CV and housing loans. Total Income in FY15 was Rs 756 crore and Net Profits stood at Rs 107 cr.

- Equitas revenues and PAT grew at 56.1% and 39.2% resp. CAGR over four years.

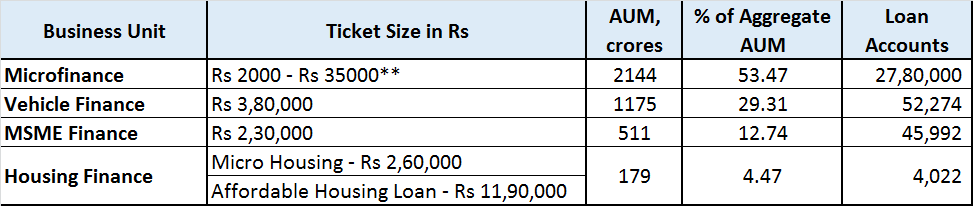

- The HQ is in Chennai, and operations are spread across 11 states, one UT and Delhi. Equitas has 539 branches and 8,067 employees. The loan portfolio in FY2015 was Rs 4,185 cr. See Fig 1

- Equitas had been granted approval by RBI for setting up a SFB. It is the fifth-largest MFI behind Bandhan (Bank), SKS (NBFC-MFI), Janalakshmi (SFB) and Ujjivan (SFB).

- The capital adequacy ratio (CAR) of EMFL (microfinance) and EFL (vehicle finance and MSE finance) was 21.02% and 31.45%, resp. as of Q3 FY2015, compared to the RBI mandated CAR of 15%. The CAR of EHFL (housing finance) was 32.1%, compared to the requirement of 12%. These look comfortable.

- The Gross NPAs ratio to On-Book AUM was 1.33%, while Net NPAs to On-Book AUM was 0.97%.

- Leadership is Mr P.N. Vasudevan (MD), N Rangachary (Non-exec chairman) & S Bhaskar (CFO).

- Foreign ownership in Equitas, currently at 92.6%, will drop below 49% after IPO.

Business News and Updates

- In Dec 2015 Equitas informed BSE of the proposed amalgamation with EHFL with EFL subject to approval of RBI and High Court of Madras.

- Equitas’ proposal to be a SFB was assessed of financial soundness, proposed business plan and fit and proper status based on due diligence reports. The RBI received 72 applications for small finance banks, and granted the status to just 10.

- India’s second largest MF house and two of the largest private life insurers were in final stages of talks to buy stake in Equitas for a total of Rs 300 cr as on 30/3/2016.

- Equitas founder Vasudevan’s vision is to create a widely owned firm run by professionals.

- Equitas will open SFB branches in all the 11 states, in which it has presence.

- Equitas has introduced two products, loan against gold jewellery and two-wheeler loans.

Industry Outlook

- Three developing economies, namely China, India and Indonesia, account for 38% of the world’s unbanked, wherein India is home to 21% of the world’s unbanked adults.

- Indian MFI sector is set to grow at 30-40%. The Loan Portfolio in Urban areas is Rs 35,320 cr (72%) and in Rural is Rs 13,563 cr (28%). (Source: The Bharat Microfinance Report 2015).

- Average loan outstanding per borrower has been an important metric for MFIs. Average loan size in FY2015 was nearly Rs 13,000 which rose 31% YoY. Average loan size in Northeast is highest at Rs 16,200 followed by North at Rs 14,300. The loan size is larger in Northeast as the economic activities in this region require higher outlays due to the hilly terrain.

- The total credit made available to poor /financially excluded clients had crossed Rs 48,882 cr. and number of clients benefited crossed 3.7 cr. by Mar2015. NBFC MFIs have CAR of 21.5%.

- The eight MFIs (Bandhan, Janalakshmi, Equitas, Equitas, ESAF, Utkarsh, Suryoday and RGVN) accounted for 26% of MFI assets in FY2015. They will convert into SFBs along with Bandhan (a bank, with 20% of AUM), so the NBFC-MFI industry size will halve.

- Outreach grew by 13% and loan outstanding grew by 33% in FY15 over FY14. The South continues to have the highest share of both outreach and loans outstanding, followed by East. However growth rates are higher in the Northeast and Central regions.

- CRISIL expects the loan book of NBFCs to post 15-17% growth till FY 2017. The MFI Industry is expected to grow at 28-30% over next 2 years. (Source: CRISIL MF Opinion, 2015).

- In the aftermath of the AP microfinance crisis, the Malegam Committee was established to review the MFI sector in India. It highlighted concerns included the high rates of interest charged, the lack of transparency in fixing of interest rates and other charges, multiple loans, upfront collection of security deposit, over borrowing, ghost borrowers and coercive methods of recovery. The Malegam Committee report resulted in the introduction of the NBFC – MFI guidelines which lay down a stringent regulatory regime for the MFI industry.

- The GoI and RBI have created conducive policy and regulatory framework for MFIs to operate in the country, by setting up MUDRA for refinancing and regulating the microfinance sector.

- The net loan portfolio as on Mar 2015 for the MFI’s stood at Rs 34,344.64 cr. Equitas thus has a market share of 6.2% in the microfinance sector.

Financials of Equitas

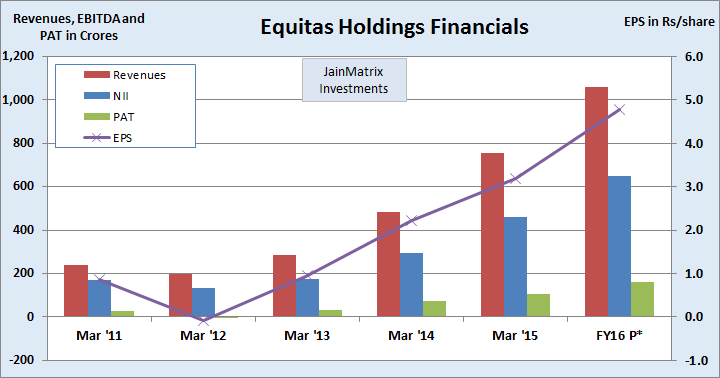

- Equitas Revenue, EBITDA and PAT has grown 56.1%, 41.1% and 39.2% CAGR over the last 4 years. This is a very high growth rate. See Fig 4.

- The operating margin increased from 49.2% in 2011 to 61.7% today. Also for Q3FY16 the figure stands was 63.6%. The profit margin increased from 11.9% in 2011 to 14.2%. NIM dropping from 21.9% in 2011 to 11.6% in 2015. This is the effect of high growth.

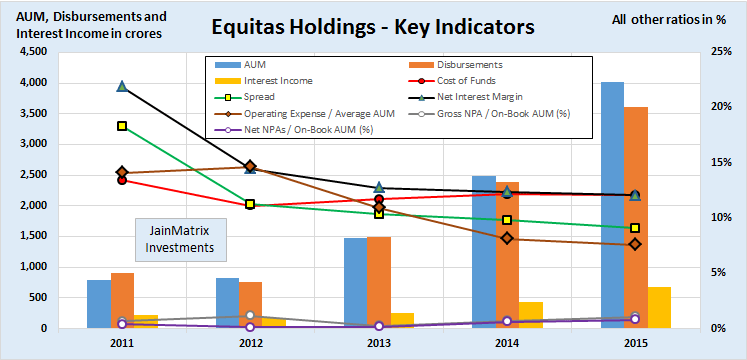

- The AUM, disbursements and interest income have grown fast over 4 years, a positive, Fig 5.

- The cost of funds has been flat over the years, but the spread has fallen slightly due to fall in the yields. So the interest margins have declined. However it is not a cause for concern.

Spread is the difference between the Yield and the Cost of Funds

Positives for the IPO

- The revenue, EBITDA and EPS growth rate have been very good over the last 4 years.

- Equitas won the SFB license approval in Sept 2015. This is a good validation of the firm’s financial soundness, business model and practices.

- Equitas as a SFB may now have access to lower cost funds, which can improve margins.

- Equitas is quite diversified in its business areas. Hence it has the flexibility to change focus segments in case of a changed business outlook.

- Equitas has a senior mgt. team with rich experience in financial services, that has developed and implementing the business strategy with a commitment to fair and transparent business practices while maintaining effective risk management and competitive margins.

- Equitas MD P.N. Vasudevan is going to sell only 1,80,000 shares, a small percentage of his holding. The company will continue to benefit from the founder’s ‘skin in the game’.

- Equitas has robust corporate governance standards, transparent operations and customer goodwill. “Equitas” in Latin means fair & transparent. Since inception, Equitas has attempted to comply with corporate governance standards applicable to publicly listed companies.

- Equitas had received the CRISIL Governance and Value Creation Level 2 rating. Also their wholly owned subsidiary EHFL received a CRISIL rating of A-/Stable in Oct 2015.

- Equitas has a large customer base of over 27 lakhs and provides wide range of credit products. The company can leverage its customer base to grow faster. As indicated by the management, once the company becomes a SFB, it intends to leverage its strength by providing agri based loans.

Internal Risks

- Political Risk: In 2010, the adverse financial conditions in Andhra Pradesh and debt related suicides by farmers led to bad publicity for the MFI sector. Subsequently, the AP govt froze the MFI loans and operations, causing extensive losses and damage to current operators. Thereafter regulatory condition improved and RBI issued MFI and SFB regulations. But the sector retains a political risk.

- In future, growth is likely to happen in two phases. Equitas has a deadline of 18 months for it to comply with the requirements under the RBI – SFB Guidelines and fulfil various conditions. Thus until next year Equitas may witness high growth as seen in the past. However post setting up of the SFB, the growth may slow as the firm adjusts to the new structure and conditions. Equitas will be required to maintain CRR and SLR, which may impact on their business operations.

- While current leadership lead by Mr. P.N. Vasudevan is excellent, the next phase of growth for Equitas requires a strong next line of management /leadership.

External Risks

- Geographic concentration: Their business is heavily dependent on their operations in Tamil Nadu (63% of loans), and any adverse changes in this region will impact business.

- Equitas is present in 12 more states, and growth there should reduce this dependence.

- SFB Challenges: The SFBs will be required to extend Priority Sector Lending to identified sectors, which may have higher delinquency rates and lower returns. If Equitas is unable to comply with these PSL requirements, then they will need to invest in funds with lower than market returns.

- The regulatory framework to govern SFBs is uncertain, due to the absence of administrative, operational or judicial precedent, in terms of regulatory non-compliances and penal actions.

- If Equitas is not able to set up its SFB structure and processes within the 18 months timelines prescribed, it will have an adverse effect on their SFB status and approvals.

- Listing issues: In the IPO, foreign investors may not be able to participate freely under the QII and NII categories as the firm is trying to reduce foreign ownership, see Fig 3. This may reduce demand.

- Competition: The MFI industry is at an early stage of growth and enjoys high margins and growth rates. However competition is intensifying as related sectors of NBFCs and Banks may diversifying into this sector. It is likely that margins may be reduce in a few years, as also industry growth rates.

Benchmarking

We compare Equitas with peers in the microfinance and rural lending space.

- Equitas leads on PE, P/B, growth and D/E parameters.

- The margins that Equitas enjoys seem low compared to these peers. This could be due to the diversified loan book of Equitas.

Overall Opinion

- Microfinance in India is a sunrise industry. In an underbanked country, availability of credit for self-employed persons in rural areas is very low.

- In this scenario Equitas follows SKS Microfinance to be the second listed company in this space. It is also the first (of 10 approvals) of Small Finance Bank in India to list.

- Equitas has a good record in terms of growth, segment diversification and profits.

- In terms of valuations, Equitas has priced the shares attractively, leaving something on the table for investors. The P/E and especially P/B appear at a discount to the peers.

- Key risks are geographic concentration and impending SFB structural changes.

- The IPO is rated a medium risk, high return offering. Retail Investors can BUY it.

Request for a PDF file of this report

JainMatrix Knowledge Base:

See other useful reports

- JainMatrix Investments Announcements

- A Superior Investing Process – Do a DIP SIP

- Rajesh Exports – a Golden Acquisition

- Engineers India FPO

- JainMatrix Investments presents the Investment Outlook for 2016

- Track Record – Dec 2015

- Dr Lal Pathlabs IPO

- Goods And Services Tax (GST): Integration And Efficiency

- Indigo IPO – Flying High, Wide And Handsome

- Café Coffee Day IPO – Very Hot Coffee

- Syngene IPO: Good Pharma R&D spinoff from Biocon.

- JainMatrix IPO Reports deliver 60.5% returns

Search for companies/ sectors of your interest in Search box in the right panel.

Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

Do you find this site useful?

- Visit the Investment Service page to find how you can get more. Or Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer:

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no known financial interests in Equitas Holdings or any related group. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst (SEBI Registration No. INH200002747) under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com .