- Date 9th Dec 2015

- Price range: Rs. 540-550 and application period: 8-10th Dec

- Industry: Pharma – Diagnostic services

- Mid Cap – Rs 4550 cr Mkt Cap

- Advice: Retail Investors can BUY with a 2-3 year perspective

Summary

- Overview: DLP is provider of diagnostic and related healthcare tests and services.

- DLP’s Revenue, EBITDA and EPS have grown at 29.2%, 29% and 33.9% CAGR over 4 years.

- Key strengths are a proven, robust ‘hub and spoke’ model which allows consistent service levels and rapid growth. It is the #2 player in this space, with a strong North India presence. It has a good brand in this niche, which can be leveraged. DLP’s model is scalable; its reach can be expanded rapidly. Also it’s not a discretionary service, more like an essential service.

- In terms of valuations, DLP has an asking PE of 54.5 times FY16 (P) which looks expensive. However we feel that the business can be valued closer to retail food services than hospitals.

- As an investment, the DLP IPO is rated a medium risk, high return type of offering.

- Opinion: Investors can subscribe to this IPO for a 2-3 year perspective.

Here is the investment note on Dr Lal Pathlabs (DLP).

IPO highlights

- IPO is open from 8-10th Dec 2015 with Issue Price band: Rs.540-550 per share

- Shares offered are 1.16 cr. of FV: Rs. 10 per share, and amount to be raised: Rs.638 cr. via OFS route. Shares offered as portion of equity post issue: 14.1%.

- Market Lot: 20 shares and in multiples of 20 shares thereof.

- There is a Rs 15 discount for Retail.

- Objects of the issue: Promoters, promoter group and investors are exiting partially from their investments. No funds raised in IPO will benefit the company directly.

- The promoter stake will reduce from 63.7% to 58.7% post IPO. Also the Pre IPO shareholding of the private investors/ VCs was 32.2% which would get reduced to 23.2% once the shares get listed.

Introduction

- DLP is a Delhi based provider of diagnostic and related healthcare tests and services.

- DLP had revenues, EBITDA and profits of Rs 662 cr, Rs 158.9 cr and Rs 95 cr. in FY15.

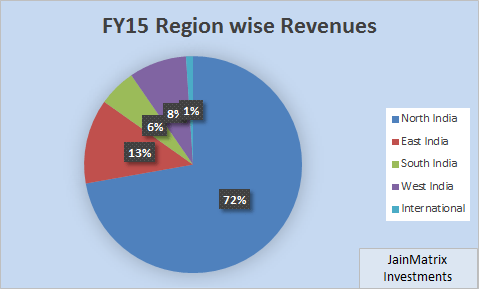

- DLP’s network includes National Reference Lab in New Delhi, 171 clinical labs, 1,554 patient service centers and 7,000 pickup points. Network is all India, but unevenly spread, see Fig 1-2.

- Customers include individual patients, hospitals, other healthcare providers and corporates.

- DLP is staffed with 3,253 full-time employees and 83 full-time consultants (contractual).

- DLP has built a national, “hub and spoke” network. Specimens are collected across multiple locations in a region for delivery to a designated clinical laboratory for centralized diagnostic It provides them with greater economies of scale and is the platform for good growth.

- DLP provides has over 3,495 diagnostic and related healthcare tests and services including – Routine clinical lab tests (blood chemistry analyses and blood cell count), Specialized testing (histopathology, genetic marker, viral and bacterial cultures and infectious disease); and Preventive testing services (screenings for hypertension, heart disease and diabetes).

- DLP was started by late Dr. Major S.K. Lal in 1949, by providing pathology services and maintaining a blood bank. The current leadership is Brig. Dr. Arvind Lal (CMD), Dr. Vandana Lal (Dir.), Dr. Om Prakash Manchanda (Dir & CEO) and Mr. Dilip Bidani (CFO).

- The Pre IPO shareholding of private investor/ shareholders was 32.2% which would get reduced to 23.2% post IPO. Private equity/ VC investors like Wagner Ltd., WestBridge Crossover Fund, LLC and Sanjeevini Investment Holdings are associated with DLP.

- The key strategy of DLP is to continue to expand their presence in the markets in which they operate and also into other markets in India through strategic acquisitions and partnerships.

- For FY15, 72% of the revenues were from the Northern region. Currently the focus of the company is to strengthen and expand their presence in Central and Eastern India. A new large, regional reference laboratory is under construction in Kolkata.

Business News and Updates

- DLP had announced its plan to expand operations in Bengaluru through new centers and labs to reach a total number of 50 centers (from current 20) by Dec 2015.

- BD India and DLP inaugurated a Centre of Excellence in Phlebotomy (blood collection, sampling) in June 2015. This center was launched to provide certified phlebotomy courses to healthcare professionals, and improving best practices for accurate and reliable diagnosis.

- DLP had acquired Ashish Pathology Labs, a lab in Ahmedabad as part of its acquisition strategy to expand inorganically last year. It has been growing mainly through organic expansion. In northern, eastern and central India it has been adding 20-25 labs year on year.

- As per DLP, “each lab costs around Rs 1 crore and there are additional investments in facilities like IT among others. Overall, we invest Rs 40-50 crore for our expansion every year”.

- DLP has sample collection centers in 9 countries and plans to start in Africa with Nigeria.

- Per latest data, DLP on day 2 of IPO is 2.65 times subscribed a sign of good success.

Industry Outlook

- According to the World Health Organization (WHO), India’s total expenditure on healthcare was 4% of the GDP as of 2013. India trails both developed countries (USA, UK) and also developing countries (Brazil, Russia, China and Thailand) in healthcare spending % of GDP. This is due to the under penetration of healthcare services as well as partial govt. ownership.

- As per CRISIL Research, the Indian diagnostics industry is at Rs 37,700 cr. in FY15. It will continue to grow by 16-17% CAGR over the next three years to over 60,000 cr. by FY18.

- Demand drivers for the Indian diagnostic industry include:

- Increase in evidence-based treatments; Changing disease profiles; big demand-supply gap;

- Increase in health insurance coverage; Need for greater health coverage as population and life expectancy increase; Rising income levels make quality healthcare services affordable

- Growing demand for lifestyle diseases-related healthcare services

- Urban areas account for a higher proportion of revenues in diagnostics industry, as the urban population (28% of population) contributes 67% of revenues (CRISIL Research).

- DLP trails only Fortis Healthcare controlled SRL in the diagnostics business. SRL had acquired Piramal Diagnostics to become the top player in the industry four years ago.

- The Govt. accounted for 32.2% of healthcare spends in India (2013), a small increase in 10 yrs.

Financials of DLP

- DLP’s Revenue, EBITDA and EPS have grown at 29.2%, 29% and 33.9% CAGR over 4 years.

- This is excellent as it indicates that the business is in high growth mode. Even with increasing competition and declining margins, the performance looks good. See Fig 3.

- However H1FY16 results were disappointing and the projected EPS for FY16 is Rs 10.1, whereas it was Rs 11.5 for FY15. This is a negative sign. Note FY16P data is a simple doubling of H1 data, also accounting for one time/ exceptional charges related to IPO.

- Currently DLP has zero outstanding borrowings as well as term loans. This is a big plus from the financial perspective. DLP has the option to raise funds in future if required.

- The operating margins have declined to 24% from 25.5% in 2012. However the profit margins have improved from 12.4% in 2011 to 14.3%. But Profit margins fell in H1FY16 to 9.2%.

- DLP’s operations have been both operating and free cash flow positive since 5 years. This is positive. But there is a declining trend due to increasing investments in the business. Fig 4.

Positives for Dr Lal Pathlabs and IPO:

- DLP financials have shown strong growth in 4 years. DLP has been acquiring small medical labs to grow inorganically. Such growth is also sustainable.

- DLP has a strong footprint in the North. Expansion in South & East will give a further impetus.

- They have built a good brand in diagnostics which is likely to strengthen in the near future.

- DLP uses a ‘Hub and Spoke’ business model, which allows consistent service levels and rapid growth.

- Experienced leadership team includes professionals with strong industry expertise and track record.

Internal Risks

- The Dr Lal PathLabs brand is fundamental to their business, and any failure to maintain the quality of their diagnostic healthcare services provided could affect their business.

- Business interruptions at DLP’s National Reference Laboratory may also affect operations.

- DLP’s business depends on franchisees and business partners. Any non-performance by them may adversely affect DLP. Some of their lab operations are undertaken jointly with third parties, whose interests may differ from DLP’s, and such arrangements entail certain risks.

- DLP leases the majority of its laboratories and other business premises. They might not be able to renew any such leases on favorable terms, and costs will rise.

- DLP is subject to seasonal fluctuations in operating results and cash flows. Diagnostic healthcare testing volumes typically increase during the monsoon season and experiences slower business during Dec-Jan, when the temperature and humidity are lower.

- For DLP, the employee benefit expenses have risen sharply over the last 5 year reflecting shortages in medical / doctor staff. If this accelerates, it can impact profitability.

External Risks

- DLP operates in a competitive business environment which has low barriers to entry.

- Diagnostics business is still dominated by unorganized local centers rather than large chains.

- The business is subject to a variety of central and state govt taxes and surcharges, and any increase in tax rates — such as GST, could adversely affect their financials.

- Political instability or disruptions at locations where they operate can affect business.

Benchmarking

We compare DLP with hospital chains as well as retail focused service companies:

- DLP emerges quite strongly across parameters like margins, growth, and return ratios.

- It does not lead the pack on the valuation parameters.

- Based on this it appears that the valuations of DLP may fall somewhere between established hospital chains and the leading retail service business.

Overall Opinion

- India with its large and growing population is stretched in terms of available healthcare facilities. Expenditure in this sector will trend upwards. Govt’s (free) facilities cater to the low end of market.

- In this space, DLP’s diagnostic and healthcare services provide an essential, high demand service. Its not a discretionary service, more like an essential service.

- The business model is robust and scalable, and there are clear benefits of a national chain over small and local service providers.

- DLP has a good brand and solid service delivery in the North, where it is established. We believe that DLP will be able to grow and roll out a national (urban) footprint. The next target would be semi urban and rural areas. There is massive potential to grow over the next 10 years.

- In terms of valuations, DLP has an asking PE of 54.5 times FY16 (P) which looks expensive. However we feel that the business can be valued closer to a retail food service than a hospital. DLP’s model is scalable; its reach can be expanded rapidly.

- As an investment, the DLP IPO is rated a medium risk, high return type of offering.

- Retail Investors can BUY this IPO with a 2-3 year perspective.

READ AND DOWNLOAD THE ENTIRE REPORT

Here is a note on the Dr Lal Pathlabs IPO in PDF format.

JainMatrix Investments_Dr Lal PathLabs IPO_Dec 2015

Click the link above to open/ download the PDF document.

JAINMATRIX KNOWLEDGE BASE

See other useful reports

- Alkem Labs IPO

- Goods And Services Tax (GST): Integration And Efficiency

- Indigo IPO – Flying High, Wide And Handsome

- Café Coffee Day IPO – Very Hot Coffee

- Syngene IPO: Good Pharma R&D spinoff from Biocon.

- Navkar Corp IPO – Location Challenges – Avoid

- CPSE ETF – Unlocking Value, Slowly

- JainMatrix IPO Reports deliver 60.5% returns

Search for companies/ sectors of your interest in Search box in the right panel.

Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

Do you find this site useful?

- Visit the Investment Servicepage to find how you can get more. Or Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no known financial interests in Dr Lal Pathlabs Ltd. or any related firm. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com

Leave a comment