- Date 17th Dec 2015

- Price range: Rs. 245-250 and Period: 17-21st Dec 2015

- MidCap Rs 5100 cr Mkt Cap

- Industry – Hospital Services

- Advice: Avoid

Summary

- Narayana Hrudayalaya Ltd was founded by eminent cardiac surgeon Dr Devi Prasad Shetty in 2000. It operates a national network of hospitals, clinics and primary care facilities.

- NHL’s revenue and EBITDA have grown 30% and 23.8% CAGR over the last 4 years. But the firm slipped into losses in FY15 on account of 3-4 acquisitions.

- NHL delivers high quality and affordable healthcare services by leveraging economies of scale, skilled doctors, process improvements and an efficient business model.

- However margins are low. In terms of valuations, NHL has an asking PE of over 200 times FY16 (P) which is very expensive. Thus from an investment perspective, NHL is not attractive at current IPO price points. It may however look attractive for development oriented or philanthropic investors.

- Opinion: Investors can avoid this IPO.

IPO highlights

- IPO is open from 17-21st Dec 2015 with Issue Price band: Rs. 245-250 per share.

- Shares offered to public: 2.45 cr roughly of Face Value: Rs.10 per share. Market Lot: 60 shares and in multiples of 60 shares thereof. Shares offered as portion of equity post issue: 12%

- Amount proposed to be raised: Rs. 613 cr via OFS route (there is no fresh issue of shares).

- This IPO is a liquidity event. The shareholders exiting partially are:

Introduction to Narayana Hrudayalaya

- NHL is a Bangalore based operator of a national network of hospitals, clinics and primary care facilities.

- NHL had revenues, Ebitda and profits of Rs 1371.6 cr., 136.6 cr. and (-10.9) cr. resp. for FY15.

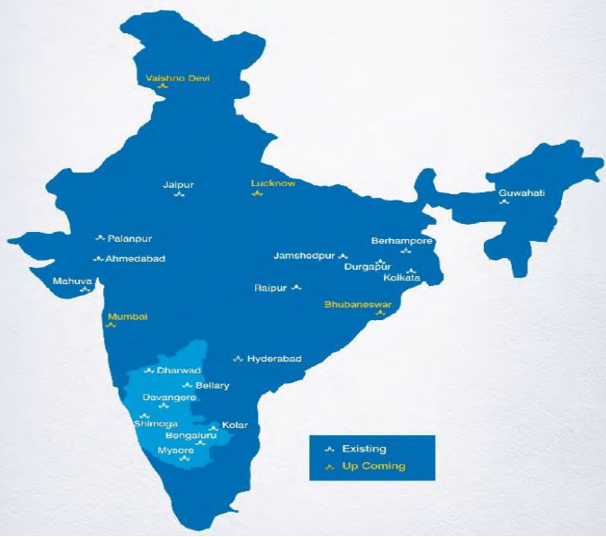

- NHL has a network of 23 hospitals (multi-specialty or super-specialty healthcare facilities which provide tertiary care), 8 heart centers and 24 primary care facilities including clinics and information centers, across 31 locations in India. Hospitals generated 90.7% of revenue, heart centers 7.3% and all others 2%.

- In FY15, NHL provided care to 19.7 lakh patients in 56 facilities with 5,442 operational beds

- NHL’s centers provide medical care in 30 specialties, including cardiology and cardiac surgery, cancer care, neurology and neurosurgery, orthopaedics, nephrology and urology, and gastroenterology.

- NHL has 11,163 employees, including 344 doctors, 5,587 nurses, 1,996 paramedical staff and 3,236 admin. personnel. They also have 1,750 consulting doctors engaged to their network.

- Leadership includes Dr Devi Shetty, Chairman & ED and Dr Ashutosh Raghuvanshi, MD-CEO.

- 3 of their hospitals are accredited by the JCI, USA for meeting international healthcare quality standards for patient care and organization management, and 6 of their hospitals are accredited by the National Accreditation Board for Hospitals and Healthcare Providers, India.

- NHL won the “Healthcare Excellence Award for Addressing Industry Issues” in 2012 from FICCI

- NHL won the “Arcelor Mittal Boldness in Business Award” in 2013

- NHL received the “Outstanding Achievement Award Healthcare – Social Cause” in 2015

NHL Business News and Insights

- NHL failed to start construction work for a proposed 1,000-bed cardiac hospital. So the state govt. issued a show cause notice to NHL initiated steps to reclaim the 6 acres of land allotted to NHL near Dumuduma (Bhubaneshwar) in Sept 2008.

- British govt owned development finance institution CDC invested Rs 300 cr in NHL for a minority share. NHL will use the funds to expand affordable treatment in Eastern, Central and Western regions.

- NHL raised Rs 183.9 cr. from anchor investors before the IPO opened, at the top end of pricing range.

- The cardiac hospital in Bangalore performs about 30 heart surgeries daily, the highest in the world, at a break-even cost of Rs 1.2 lakhs. This is significantly lower cost than most other hospitals in India.

- In line with social objectives, most patients are charged more, but the poorest are treated for free.

- M&A: NHL acquired Westbank Hospital for Rs. 150 cr. in Nov 2014, also Asia Healthcare Development (AHDL), Meridian Medical Research & Hospital (MMRHL), and Jubilant Kalpataru Hospital in 2014.

- NHL operates its business through a combination of the following models:

- hospitals – that they own and operate;

- hospitals/ heart centers – operate and pay revenue share

- hospitals, standalone clinics and primary care facilities – operate on a lease or license basis; and

- hospital management services provided to third parties for a fee – Managed Hospitals.

- Dr Devi Prasad Shetty is a famous heart surgeon, who founded NHL.

- He came to the conclusion that the health care industry needs more process innovation than product innovation. The industry “does not need a magic pill or the fastest scanner or a new procedure,” but instead requires improvements that lower the cost of medical attention and make it more widely available. Shetty’s premise of economies of scale is not radical; in fact, the doctor describes his way as “the Walmart approach.” What sets him apart, however, is that he has successfully adapted the method to a field as complex and costly as cardiac care. (knowledge@wharton).

- NHL provides free treatment or subsidized costs to certain categories of patients. This is part of NHL’s social strategy. In some cases, their agreements with partners or state governments may also specify such quotas/ subsidies. NHL then charges higher to other patients in order to recover these costs.

Industry Outlook

- According to WHO, India’s total expenditure on healthcare was 4% of India’s GDP in 2013. India trails developed (USA, UK) and also developing countries (Brazil, Russia, China and Thailand) on spending to GDP, due to the under penetration and price sensitivity

- India is the 10th largest economy (GDP of USD 1.9 trillion) with 20% of the people (1.2 billion).

- The Govt. accounted for 32.2% of healthcare expenditure in India (2013) a small increase in 10 yrs.

- A key concern India faces is the affordability of healthcare by a vast majority of its population. According to the WHO, while 58% of the total healthcare expenditure in India is borne by consumers directly (without insurance coverage or reimbursements), this proportion rises to 86% in case of private healthcare services. This has however reduced over the last decade.

- As per CRISIL estimates the size of the Indian healthcare delivery industry is at 3,400 million treatments in volume terms and Rs 3,80,000 cr. in value terms in 2014-15. The healthcare delivery market would grow at a CAGR of 12% till 2020.

- Cardiac care has the highest average realization per patient (CRISIL).

- A key cost factor in a hospital is the initial capital outlay required, particularly for land, building development and equipment. The capital cost to build a hospital is typically Rs 70-80 lakhs per bed (for a typical 200 bed multispecialty hospital, excluding land costs).

- The drivers of growth in the healthcare delivery market in India are:

- Potential in bed capacity – India’s bed density is 7/10,000 people (global median – 27 beds).

- Govt spending on healthcare will remain low, allowing private sector to increase presence

- Increasing population as well as life expectancy to require greater health coverage

- Rising income levels to make quality healthcare services more affordable

- Growth in medical tourism, cosmetic medical services to aid demand growth

- Anecdotal evidence points to falling medical standards in large hospitals:

- Cesarean births are rising alarmingly as a ratio to natural deliveries in many regions.

- Many large urban hospitals target affluent patients with a battery of unnecessary tests and procedures, effectively milking the patient under the guise of a doctor’s line of treatment.

- Medical services are only as good as the person serving you. Stories abound of medical negligence like silly errors during operations, nurses and staff missing pre or post operation, etc.

- Inflated medical bills for patients with insurance

- There appears to be a shortage of medical nursing staff. This is attributed to a lack of professional growth in India (and ample opportunities abroad). Nurses in India are not allowed to carry out simple medical tasks, which are reserved for doctors, thus limiting their professional growth.

- Medical Colleges and higher education are constrained by limited seats and high costs.

- Many such issues fall under the purview of the Medical Council of India.

Financials of NHL

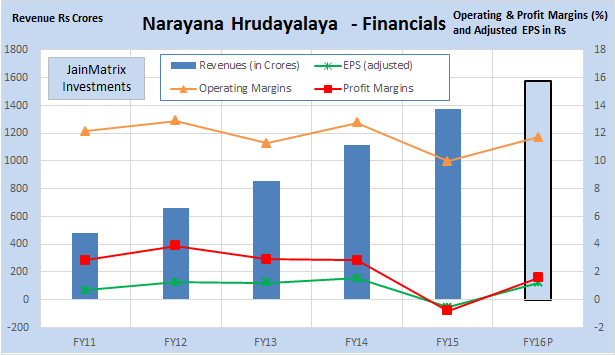

- The EPS of NHL has grown 32.5% CAGR from the year 2011-2014 which is a positive sign of high growth potential. However in FY15 NHL posted a loss of Rs 10.9 cr. Also again it has turned PAT positive for HI FY16. Note FY16P data is a simple doubling of H1 data.

- NHL’s revenue and EBITDA has grown 30% and 23.8% CAGR over the last 4 years. This is excellent.

- Margins have become thinner for NHL in the last 4 years. See Fig 4.

- NHL has been operating cash positive over 5 years, but the free cash flows are negative. Fig 5.

Positives for the IPO

- NHL has a social commitment to provide subsidized/free services to some patients.

- Dr Devi Shetty has through NHL created a ‘Walmart’ type business model for high end services like heart surgeries, and has lowered costs while delivering high quality. This is widely recognized in the industry and NHL/ Dr Shetty have been awarded many times for these achievements.

- NHL has a strong brand ‘Narayana Health’ with good presence in Karnataka & East India. Its has a reputation for clinical excellence and affordable healthcare.

- NHL is setting up in the NorthEast and Vaishno Devi (where hospital facilities are scarce), Lucknow (multi-specialty hospital), Mumbai (pediatric hospital) and Bhubaneshwar (tertiary care).

- NHL is strong in many segments, but particularly in cardiology and cardiac surgery.

- Capital efficiency – NHL’s capital cost is Rs 25.5 lakhs/bed in FY2015 (industry avg 70-80 lakhs/ bed).

- Ability to attract high quality doctors and medical support staff.

- Experienced management team with a strong execution track record.

- Anecdotal evidence suggests that the NHL chain appears to have a better reputation in terms of patient care, good medical advice and trustworthy services than other large hospital chains.

Internal Risks

- Dr Devi Shetty has built NHL to this scale, but there may be a need to broad base the firm’s leadership so that it can become an institution, rather than be dependent on a few leaders.

- Just three large hospitals contribute 58% of total revenues currently. Thus any disruption to any of these 3 will affect their business.

- A majority of NHL doctors are not employees but medical consultants. There is no assurance that they would continue to provide services to NHL on an ongoing basis. This can affect business.

- NHL has in the past ceased operations and decommissioned beds at some facilities. NHL may not be able to successfully implement all their growth strategies, particularly in Tier II and Tier III cities.

- Litigation related to medical services, from patients is a business risk.

- They recently acquired a third party hospital and two hospitals companies. These and any future acquisitions may present integration challenges or turn out to be unprofitable. Acquisitions carry the inherent risk of past non-compliance and undisclosed liabilities.

- NHL is exposed to business risks related to clinical trials undertaken and stem cells they preserve.

- The IPO is a liquidity event and an exit platform. Funds raised will not benefit NHL.

External Risks

- In general, a number of govt. and regulatory registrations, licenses and approvals have to be obtained. In particular, Narayana Hospitals and AHDL have not obtained occupancy rights over certain hospitals and clinics they operate out of, and not obtained ownership rights over certain lands forming part of NH Health City and certain superstructures constructed by them in RTIICS. They run the risk of being dispossessed of these properties. (RHP)

- The Central or State Governments may exercise rights of eminent domain in respect of the land on which NHL’s facilities are situated.

Benchmarking

In a benchmarking exercise, we compare NHL with some listed peers.

- Sales at NHL have shown an impressive growth.

- But valuations look expensive. Since there was a loss in FY15, the PE is not mentioned. But estimated PE for FY16 falls in the 200-205 range, a very high number.

- Even on EV/EBITDA and EV/ Sales, NHL falls at the higher end among its peers.

- Debt levels are reasonable, not high. But return ratios are quite low.

- The reason we can find for low margins and even losses in FY15 are – several acquisitions were made in this year, which are integral with NHL’s growth strategy. However these operations are yet to contribute to the returns for NHL.

Overall Opinion

- India with its large and growing population is badly stretched in terms of quality healthcare facilities. Expenditure in this sector will trend upwards. Govt’s (free) facilities cater to the low end of market.

- NHL has a good brand name and sustainable model for providing quality and affordable healthcare. It has lowered the costs of delivering complex procedures, while also meeting social objectives.

- The pricing for NHL IPO looks stretched from various angles. In FY 2015, NHL suffered a loss. At the projected FY16 profits, the PE looks like 200-205 times.

- Perhaps NHL has in an attempt to grow fast and acquire companies, compromised on profits for FY2015 and FY2016. Modern companies are making such trade-offs.

- Perhaps NHL has sacrificed profits for its social objectives. It can easily improve margins but takes on a number of free or subsidized procedures and ‘does good rather than just make money’.

- Can the trustworthiness and technical competence at NHL justify a big pricing premium to the peers in Exhibit 6?

- NHL does not have positive free cash flows since 5 years.

- NHL executives need to clearly articulate their profit or social objectives to potential investors and shareholders, especially since these clash with each other.

- We conclude from this that for investors, NHL is not attractive at current price points. But it may look attractive for development oriented or philanthropic investors.

- Investors should avoid this IPO and look to enter the counter at lower levels.

READ AND DOWNLOAD THE ENTIRE REPORT

Here is a note on the NHL IPO in PDF format.

JainMatrix Investments_Narayana Hrudalaya IPO_Dec 2015

Click the link above to open/ download the PDF document.

JAINMATRIX KNOWLEDGE BASE

See other useful reports

- Track Record – Dec 2015

- Dr Lal Pathlabs IPO

- Alkem Labs IPO

- Goods And Services Tax (GST): Integration And Efficiency

- Indigo IPO – Flying High, Wide And Handsome

- Café Coffee Day IPO – Very Hot Coffee

- Syngene IPO: Good Pharma R&D spinoff from Biocon.

- Navkar Corp IPO – Location Challenges – Avoid

- CPSE ETF – Unlocking Value, Slowly

- JainMatrix IPO Reports deliver 60.5% returns

Search for companies/ sectors of your interest in Search box in the right panel.

Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

Do you find this site useful?

- Visit the Investment Servicepage to find how you can get more. Or Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no known financial interests in Narayana Hrudalayala Ltd. or any related firm. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com

Leave a comment