- Date 24th July; IPO Opens 25-27th July at Rs. 1095-1100

- Valuations: P/E 32.3 times TTM, P/B 10.7 times (Post IPO)

- Mid Cap: Rs. 23,300 cr. Mkt cap

- Industry – Asset Management

- SUBSCRIBE for the IPO

Summary

- Overview: HDFC AMC is the #2 player among AMCs by AUM and #1 by profits. HDFC operates as a JV between HDFC and Standard Life Investments. HDFC is one of India’s leading finance companies. Revenues and profit for FY18 were Rs. 1,867 cr. and Rs. 722 cr. HDFC revenues, EBITDA and PAT grew at 19.9%, 19.2% and 19.1% CAGR in 5 years. The Indian mutual fund industry is expected to grow at a CAGR of 20% between FY18 and FY22, due to buoyant capital markets, and a shift from physical to financial assets. Valuations in terms of P/E are 32.3 times, P/B at 10.7 times and market cap/AUM at 8% are high. However we have seen that in emerging sectors/ industries the excelling high quality players can command very high valuations. So a good track record, robust financial performance, sectoral tailwinds, reputed management team and good promoter identity makes this IPO attractive.

- Risks: 1) High Valuations 2) Regulatory risks 3) Competition can impact margins 4) Macro concerns

- Opinion: Investors can SUBSCRIBE to this IPO with a 3 year perspective.

Here is a note on HDFC Asset Management Company (HDFC) IPO.

IPO highlights

- The IPO opens: 25-27th July 2018 with the Price band: Rs. 1095-1100 per share.

- Shares offered to public number 2.54 crore. The FV of each is Rs. 5 and market Lot is 13.

- The IPO is of Rs. 2,800 cr. for 12% equity by current promoters HDFC Ltd. and Standard Life Investments UK, with no dilution. HDFC Ltd. and Standard Life are selling 4.05% and 7.96% of shares.

- The Promoter group (HDFC and Standard Life) own 95% in HDFC which will fall to 83% post-IPO, ie. 53% and 30% in resp. HDFC is a well-known Indian NBFC and is the holding company into financing the purchase or construction of houses, commercial real estate, etc. in India.

- The IPO share quotas for QIB, NIB and retail are in ratio of 50:15:35.

- The unofficial/ grey market premium for this IPO is Rs. 370-380/share. This is a positive.

Introduction to HDFC AMC

- HDFC AMC is a leading Indian asset management firm into Mutual Funds and PMS Advisory. It is a JV between HDFC Ltd and Standard Life Investments. HDFC Ltd. is a leading Indian housing finance firm.

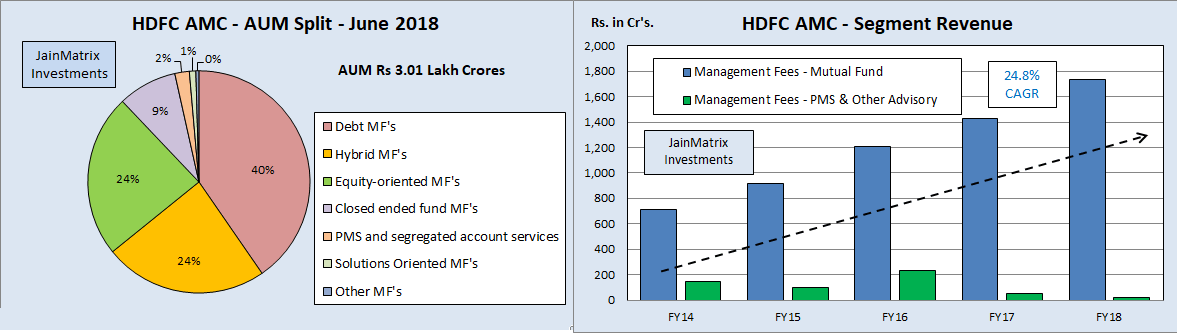

- Revenues and profit were Rs. 1,867 cr. and Rs. 722 cr. for FY18. It has 1,010 employees out of which 58% are in sales and 29% are in client services. It had an AUM of Rs. 2,92,000 cr. in FY18. It is the most profitable AMC in India. It is the largest AMC in India in terms of equity-oriented assets and has consistently been among the top 2 AMCs in India in terms of total average AUM since Aug 2008.

- The equity-oriented and non-equity-oriented assets are Rs. 1,50,000 cr. and Rs. 1,42,273 cr. resp. of total AUM. HDFC AUM has grown at 25.5% CAGR over FY13-18. Their proportion of equity-oriented AUM to total AUM is 51.3%, higher than the industry average of 43.2%. As equity schemes have a higher fee structure compared to non-equity schemes, the product mix helps achieve higher profits.

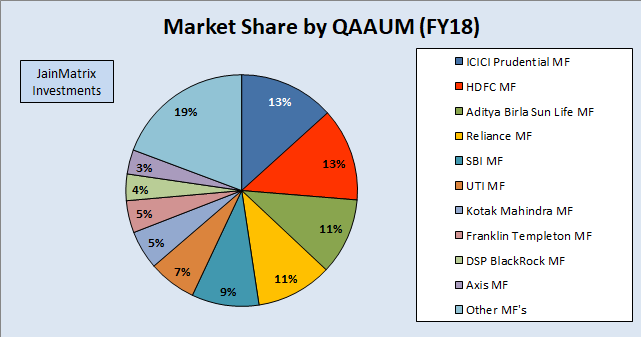

- The market share of AUM is 13.7% and of active equity AUM is16.8% among AMCs see Fig 1c.

- HDFC offers a large suite of savings and investment products across asset classes, which provide income and wealth creation opportunities to customers. In FY18, they offered 133 schemes classified as 27 equity-oriented schemes, 98 debt schemes (including 72 fixed maturity plans FMP), three liquid schemes, and 5 other schemes (including ETF schemes and funds of fund schemes).

- This diversified product mix provides them with the flexibility to operate successfully across various market cycles, cater to a wide range of customers from individuals to institutions, address market fluctuations, reduce concentration risk in a particular asset class and work with diverse sets of distribution partners which helps them expand their reach.

Fig 1(a) – HDFC AUM split -June 2018 (b) HDFC Segment revenues c) Market share /Note – QAAUM is Quarterly Average AUM /Click to enlarge image view.

Fig 1(a) – HDFC AUM split -June 2018 (b) HDFC Segment revenues c) Market share /Note – QAAUM is Quarterly Average AUM /Click to enlarge image view.

- HDFC also provides portfolio management and segregated account services, including discretionary, non-discretionary and advisory services, to high networth individuals (HNIs), family offices, domestic corporates, trusts, provident funds and domestic and global institutions. As of FY18, they managed AUM of Rs. 6,474 cr. as part of their PMS and segregated accounts services’ business.

- HDFC had a total of Live Accounts of 81 lakh as of FY18, and their Monthly Average AUM from individuals was 62.2% of their total MAAUM, compared to the industry average of 51.4%.

- A key element of their strategy is to promote a customer-centric culture that spans across all aspects of their business. As of FY18, they served customers in over 200 cities through their pan-India network of 209 branches (and a Dubai office) and service centers of their registrar and transfer agent, which is supported by a network of 65,000 empaneled distribution partners across India, consisting of independent financial advisors, national distributors and banks.

- Leadership is Deepak Parekh (Chairman), Keki Mistry (Non-Exec Director), Milind Barve (MD), Prashant Jain (CIO) and Piyush Surana (CFO).

Promoter – HDFC Ltd and Group – Snapshot and Financials

- The HDFC group is a known financial conglomerate in India, with presence in housing finance, banking, life and non-life insurance, asset management, real estate funds and education finance. Listed companies of the group include HDFC Ltd., HDFC Bank, HDFC Standard Life Insurance Co. and GRUH Finance. HDFC Ltd is the holding company and is also engaged in financing the purchase or construction of residential houses and commercial real estate.

- Income and PAT has grown at 14.1% and 19.5% CAGR resp. over 5 years.

Fig 2 – HDFC Financials

Fig 2 – HDFC Financials

- HDFC Ltd. share price gained 19.5% CAGR over the last 5 years and CMP is Rs 1,970.

- HDFC Ltd. has visible signs of pick-up in demand for mortgage loan led by improving affordability, attractive incentive from PMAY scheme and introduction of RERA which augurs well for sustained growth in loan book for HDFC over the next 3-5 years. Further, the performance of its various financial business subsidiaries/associates has improved substantially over the last few quarters.

- The key risks are 1) Aggressive competition among the HFCs 2) Unstable interest rate environment.

- HDFC has a market cap of Rs 3,33,106 cr. to be ranked #6 in India.

- HDFC is a prestigious group with good ethics. It has rewarded shareholders and performed well over decades. The listed subsidiaries of HDFC Ltd. have generally retained these qualities.

News, Updates and Strategies of HDFC AMC

- The average cost of acquisition of equity shares for HDFC ltd. has been Rs 19.53 over 2000-18 and for Standard Life Investments it is Rs 15.01 over same period.

- HDFC’s business strategy is as follows: 1) Maintain strong investment performance 2) Expand their reach and distribution channels 3) Enhancement of product portfolio. 4) Invest in digital platforms to establish leadership in the growing digital space.

- HDFC has grown by acquisition, taking over Morgan Stanley AMC (2014) and Zurich India MF (2003).

- HDFC AMC sold its shares worth almost Rs 150 cr. to distributors in April 2018 before the upcoming IPO. These shares were offered to 190 distributors and advisers at Rs. 1,050/share. But SEBI in July 2018 directed HDFC to scrap this placement and to return the money it had collected with a 12% interest. These shares were then acquired by PE firm KKR paving the clearances for the IPO. Prior to the share allotment, HDFC had sought approval for a special quota for distributors in its IPO, but SEBI rejected the proposal then because it was against a separate quota for distributors.

MF Industry Outlook in India

- The economy has seen financial events such as demonetization, RERA implementation, GST and a crackdown on black money and shell companies. All these have rekindled interest in financial assets as compared to real estate and gold which were the most popular earlier.

- Penetration of equities remains low, with only 2% of population having a demat or equity /MF ownership. Gold & real estate hold a large proportion of savings but have generated weak returns.

- The regulations and disclosures around MFs have ensured good traceability and audit trails. SEBI has promoted MFs as good entry level equity and debt products, and MF asset growth has been good.

- The MF industry’s AUM grew at a CAGR of 24.9% from Rs. 7 lakh cr. in FY13 to Rs. 21.4 lakh cr. as of Mar 2018, supported by strong investor inflows of Rs. 9 lakh cr. FY17 & FY18 have been remarkable for the industry, attracting around 68% of the Rs. 9 lakh cr. net inflow, with equities leading the charge. Equity-oriented funds (including balanced and excluding ETFs) attracted 60% of the total net inflows in FY17 & FY18. Supported by these strong inflows, growing participation from individual investors and rising equities, the assets surged 42.3% in FY17 and 21.7% in FY18. During FY18, the fresh investments in MFs grew by 22.2% to Rs. 3.9 lakh cr. in the FY 2018.

- The growth in the AUM has been supported by a favorable macro environment, the rising of capital markets, foreign fund inflows as well as growing investor awareness.

- Today there are 41 AMCs operating comprising 7 promoted by PSB’s, 2 by financial institutions, 25 by private sector and 7 by foreign players (including JV’s). The Indian MF industry is concentrated with the 10 large AMCs having 80% of the industry AUM. ICICI Prudential AMC, HDFC, Reliance, Birla Sun Life and SBI Funds are the 5 largest with 57% of AUM.

- The MF industry is expected to grow at a CAGR of 20% between FY18-22, with the AUM expected to grow to Rs. 45 lakh cr. by Mar 2022. Growth rates are expected to be higher in FY19 due to buoyant capital markets and increase in retail participation, after which it may taper down. Stock broking firms too perform very well when markets are in a bullish phase.

- Global asset management firms have struggled in India as independent MF firms. Many sold out and exited. They have had a better success rate on partnering with Indian firms as the MF JV promoter.

- India’s MF penetration (AUM to GDP) at 12.8% is much lower than the world average of 62% and also lower than developed economies like US (101%), France (76%), Canada (65%) and UK (57%) and even emerging economies like Brazil (59%) and South Africa (49%). This is expected to grow fast.

Financials of HDFC

- HDFC revenues, EBITDA and PAT grew at 19.9%, 19.2% and 19.1% CAGR in 5 years, see Fig 3.

- Margins for 5 years are flat but high double digits due to good exposure to equity assets. Given the high revenue growth, flat margin is a good achievement. Absolute profits have grown fast.

- HDFC had a RoE of 33.4% in FY18 and RoCE of 49.1%. The return ratios are high and excellent.

- HDFC paid dividends of Rs. 405 cr. in FY18 (including DDT). The dividend payout ratio is high at 56%.

- HDFC has been Free Cash Flow positive in the last 5 years. This is good CF management, see Fig 4.

- 76% of the pre IPO equity shares have been pledged by a non-promoter shareholder. None of the shares held by the promoter or promoter group have been pledged.

- The issue has been priced at Rs. 1,100 share which translates to a P/E of 32.3 times. The market cap/AUM is 8%. This is aggressive and makes the issue expensive.

Fig 3 – Financials, Fig 4 – HDFC Cash Flow

Fig 3 – Financials, Fig 4 – HDFC Cash Flow

Benchmarking

We benchmark HDFC against other Indian and global AMCs. See Exhibit 5. Only Reliance Nippon is a pure AMC, other Indian firms have NBFC and broking businesses. US firms are for comparison.

- The asking PE and P/B is high. HDFC has moderate 3 year sales and PAT growth. The NBFC business segments of Indian firms has allowed faster growth.

- The Debt is low, but again for non AMC business, the debt is necessary so it not comparable.

- The margins are at the higher end amongst most peers from the industry. This is a positive.

- The return ratios historically also have been very high and robust among comparable peers.

- Note – The USA companies data is for CY2017, Exchange rate is Rs/$ of Rs 68.

Exhibit 5 – Benchmarking

Exhibit 5 – Benchmarking

Positives for HDFC and the IPO

- HDFC has a market leadership in the Indian MF industry of #2 on AUM and #1 on equity AUM. Their market share of total AUM was 13.7% and of actively managed equity-oriented AUM was 16.8%.

- HDFC has a trusted brand and strong parentage of HDFC group. The holding company and the 3 other listed group firms have done well on the stock markets. HDFC Standard Life Insurance Co was the most recent to list in Nov 2017. It has also done well post listing, up 65% on IPO price.

- HDFC MFs have performed well with a solid approach, philosophy and risk management.

- HDFC has a superior and diversified product mix distributed through a multi-channel distribution network. Their product mix enables them to operate through various market cycles, cater to specific customer requirements and reduce concentration risk. Strong distribution relationships also ensure the commitment of the channels for new launches and investor support and confidence.

- HDFC has consistently had assets and profit growth.

- HDFC has an experienced and stable management & investment teams.

Risks and Negatives for HDFC and the IPO

- The valuations are high in terms of P/E, P/B and market cap/AUM.

- HDFC had overextended its distributor benefits pre-IPO, and was ordered by SEBI to avoid a conflict of interest and revoke the distributor allotment of shares. HDFC realizes the importance of distributors, but needs to take care to not cross the legal or market accepted limits.

- The global macros are looking cloudy. Trade war tensions between USA – China can escalate. A diplomatic conflict with Iran is playing out. Oil prices are trending higher. Brexit threatens the UK economy. Europe and the Euro are looking weak with poor economic outcomes for the region. In this situation a sharp deterioration on any of these parameters can affect Indian investment climate.

- AMCs are closely regulated by SEBI and is subject to changes or tightening of norms. For example in July 2014, the holding period for long-term capital gains tax on debt MFs was increased from 12 to 36 months. It is possible that regulatory changes can affect their business in future.

- SEBI in Oct 2017 issued a circular to categorize and rationalize the MF schemes. MFs are classified into 5 groups, i.e., equity, debt, hybrid, solution oriented and other schemes. These 5 groups have 36 categories of schemes, and only 1 scheme per category is permitted by a MF. This has resulted in many MF schemes being merged, renamed and repurposed in the industry. HDFC has complied with the SEBI changes, but the rationalization may have a adverse impact on their brands and business.

- Competition from existing and new MFs could reduce their market share or put pressure the fees.

- The tax on Long term Capital Gains from equity was introduced in budget 2018 in Feb at 10%, from zero earlier. This caused a correction in markets, particularly the mid and small cap stocks.

- Competition to the MF industry is from alternatives like the PMS industry, AIF/ Hedge Funds, Private equity markets and direct equity advisory services. Many of these are the next steps for MF investors after they have started their investment journey with MFs.

- HDFC has defocused from PMS and other segments and appears to focus on Mutual Funds.

Overall Opinion and Recommendation

- In India there is a massive trend of financialization of assets, a move away from physical / guaranteed assets like real estate, gold and FDs, towards equity and debt.

- The MF industry is witnessing a massive growth with total AUM’s growing rapidly in the last 10 years. The number of new investors and their portfolios has grown significantly from retail investors. In fact the domestic driven MF industry has emerged as a foil to the FII investors in India.

- The #2 player by AUM, HDFC AMC is well managed financially, has a great brand, high margins and return ratios, low CAPEX and cost structure.

- Valuations look high in terms of PE 32.3 times, P/B 10.7 times and market cap/AUM at 8%. However we have seen that in emerging sectors/ industries the excelling high quality players can command very high valuations (think Avenue Supermarts in Retail and group firm GRUH Finance in rural home loans). HDFC certainly faces high competition, but can pull ahead and become #1 by AUM in the next few years. So a good track record, robust financial performance, sectoral tailwinds, reputed management team and strong promoter identity makes this IPO attractive.

- Opinion: Investors can SUBSCRIBE to this IPO.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake ownership or known financial interests in HDFC AMC. He has a stake in HDFC Bank. Punit Jain may apply for this IPO in the Retail category. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

Leave a comment