- Date 14th Mar; IPO Opens 15-19th Mar at Rs. 370-375

- Large Cap: Rs. 44,780 cr. Mkt cap

- Industry – Commercial Bank

- Valuations: P/E 40.2 times TTM, P/B 4.9 times (Post IPO)

- Advice: SUBSCRIBE

- Overview: Bandhan is a commercial bank focused on serving underbanked and underpenetrated markets in India. Bandhan Bank has the largest microfinance loan portfolio, with Rs. 21,380 crores as of FY17. Bandhan bank has a great brand recall, strong financial performance, good asset quality and an experienced management. It is the new MFI loans leader. Presence in underbanked East and NE regions and universal bank structure are key strengths. At a P/B of 4.93 times (post IPO), the valuation look expensive. However Bandhan has a focus and a leadership position. It also operates in niche geographies.

- Risks: 1) Economically and politically sensitive sector 2) Significant exposure to unsecured loans.

- Opinion: Investors can SUBSCRIBE to this IPO with a 2 year perspective.

Related Reports:

- SKS MICROFINANCE – A MAGICAL MIX (Now Bharat Financial Inclusion)

- NEW BANKS: BIG CHANGES IN SMALL CHANGE

- EQUITAS IPO – LEADER IN SF BANKS

- BAJAJ FINANCE – A FIRM YOU CAN BANK ON

Here is a note on Bandhan Bank (Bandhan) IPO.

IPO highlights

- The IPO opens: 15-19th Mar 2018 with the Price band: Rs. 370-375 per share.

- Shares offered to public number 11.92 cr. The FV of each is Rs. 10 and market Lot is 40.

- The IPO in total will collect Rs 4,473 cr. while selling 10% of equity.

- The promoter & promoter group owns 89.6% in Bandhan which will fall to 82.2% post-IPO.

- The offer will be both a sale by current shareholders (OFS) and also by issuing fresh shares. The OFS proceeds would be Rs. 810 cr. at UMP and fresh issue size is Rs. 3,662 cr.

- The selling shareholders are IFC and IFC Investment Co. They are partly exiting through this IPO. The IPO is being launched as Bandhan needs to comply with the RBI’s direction of listing publicly and reducing promoter holding to 40% within the first 3 years of operations.

Exhibit 1 – IPO Selling Shareholders

- The IPO share quotas for QIB, NIB and retail are in ratio of 50:15:35.

- The unofficial/ grey market premium for this IPO is Rs. 30-35/share. This is a positive.

Introduction

- Bandhan is a commercial bank focused on serving underbanked and underpenetrated markets in India. They have a universal banking license that permits them to provide banking services pan-India across customer segments. They currently offer a variety of asset and liability services designed for microfinance (MFI) and general banking, as well as services to generate non-interest income.

- Revenues, NII and profit for FY17 were Rs. 4,320 cr., Rs. 2,403 cr. and Rs. 1112 cr. resp. It has 27,176 employees. 88% of their gross loans were micro loans (FY17). 96% of their loan book is unsecured.

Fig 2a – Loan products

Fig 2b Gross Loans and Fig 2c Loans Segments

Fig 3a Regions and Fig 3b Segments FY17

- Bandhan Konnagar was formed in 2001 as a NGO providing microfinance services to socially and economically disadvantaged women in rural West Bengal. It later became Bandhan Financial Services Ltd and subsequently got the conditional banking license in 2014.

- Bandhan operated across 33 States and UT’s through 887 branches, 2,633 doorstep service centres and 430 ATM’s. The gross loans of Bandhan are displayed in Fig 2b and 2c. 58% and 23% of the loans were from East and NE regions resp. for 9M FY18. Hence there is a geographic concentration risk.

- Bandhan generates 87% of revenues from retail banking business. See Fig 3(b).

- Total borrowings were Rs 1,330 cr. (9M FY18) and the cost of borrowings was 7.9% (FY17).

- Leadership is Chandra Shekhar Ghosh (MD & CEO), Sunil Samdani (CFO) and Biswajit Das (CRO).

News, Updates and Strategies of Bandhan

- IFC had invested in Bandhan Feb 2016 at Rs 42.93 so for their partial exit they will get 7.7X returns.

- The bank’s loan book grew at 51% CAGR over past 17 years, which slowed to a still strong 33% by 9M FY18. As per mgmt., in next 2-3 years a 33-35% growth in advances can be achieved.

- RBI’s guideline is to reduce the promoter’s stake to 40% within 3 years from the date of start of business as a bank. Bandhan received the nod in June 2015, so this timeline is quite close.

- Bandhan’s business strategy is as follows:

- To maintain focus on micro lending while expanding further into other retail and SME lending.

- To strengthen their liability franchise in order to provide a stable, low-cost source of funding.

- To enhance their digital platform to improve customer acquisition and retention and reduce costs.

Micro Finance and Banking Industry Outlook in India

- Financing needs in India have risen along with economic growth over the past decade. By complementing banks and other financial institutions, NBFCs help meet this need.

- MFI is a volatile sector that can be badly affected by economic and political events. The Bank structure is better to house MFI activities, as can be seen by Bharat Financial merger with IndusInd Bank, and SFB license to several players by RBI. Bandhan has a good advantage here.

- Bandhan has the largest overall gross micro-banking asset portfolio, with Rs. 21,380 cr. as of FY17. Amongst the banks (private as well as public), the micro loans given by Bandhan are more than 3 times the next player, SBI.

- It has an estimated 15-20% share in MFI.

- Penetration of Microfinance is low in NorthEast India, which can be to Bandhan’s benefit. See Fig 4.

Fig 4 – Micro Finance Penetration (Source: The Bharat Microfinance Report 2017)

- The gross loan portfolio (GLP) of MFIs grew at 51% CAGR from FY13 to FY17. This growth was fuelled largely by the growth in GLP of some large players, such as Janalakshmi Micro-finance, Bharat Financial Inclusion, Ujjivan Financial Services and Satin Creditcare Network.

- Banking credit growth slumped in the previous 2 fiscal years owing to asset quality and capital adequacy issues. However, as per CRISIL Research bank credit will rise owing to improvements in working capital demand, marginal pick-up in private investment, increased govt. spending on the infra, improvements in commodity prices, and expectations of a good monsoon season.

- Though demonetisation affected the retail sector’s credit performance in FY17, which dropped 300 bps from FY16, growth remained higher than industrial and agricultural credit growth in FY17. The retail segment represents more than one-fifth (23% as of FY17) of overall banking credit, and in turn, derives a major share from housing finance, which accounts for 53% of retail credit by banks as of FY17. So the retail segment was negatively impacted by the demonetisation-driven slump in the real estate sector. Retail credit grew 16% YoY, while industrial credit contracted YoY by 2%.

Financials of Bandhan Bank

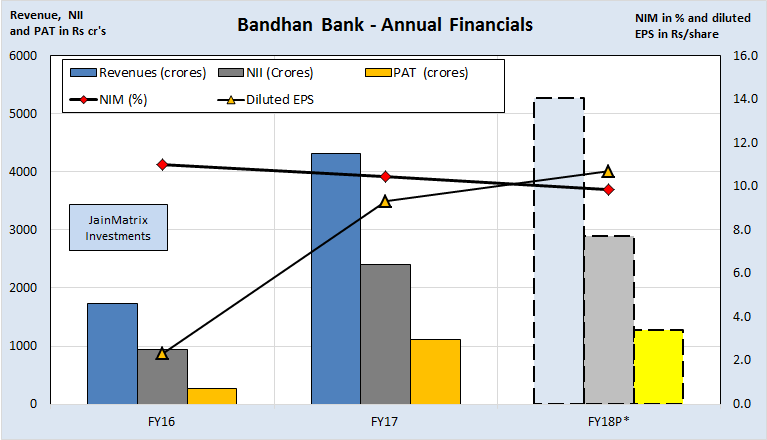

- Bandhan’s revenues, NII and PAT over the years are in Fig 5.

- Previous data is not shared as its business model changed from an NGO to NBFC to a bank.

- Bandhan had a RoE of 25.01% and RoA of 4.5% in FY17. This is excellent as the return ratios are high and amongst the best in the industry. It has not declared any dividends in the last 5 years.

Fig 5 – Financials (FY18 is projected by extrapolating 9M results)

- NIM’s for Bandhan have declined in the last few years, however the NIM’s were high at over 11% in FY16 which has gradually declined to 9.86% in 9M FY18. Currently, it earns a high yield on loans, however as the bank expands its loan portfolio to other segments and into general banking there could be significant drop in the NIM.

- The gross loan and disbursement growth slowed in FY17 due to demonetization related issues.

- Bandhan has a robust asset quality. The GNPA as on 9M FY18 stood at 1.67% whereas the NNPA’s stood at 0.8%. The NNPA’s for FY17 were as low as 0.4%. Priority Sector Loans constitute 31.6% of the total advances as of 9M FY18. 97.6% of the GNPA’s are from the PSL loans for Bandhan Bank.

- As a universal bank, Bandhan has a CASA ratio of 33.22%. This is fair, and should grow in future.

Benchmarking

We benchmark Bandhan against peers, See Exhibit 6.

Fig 6 – Benchmarking

- Majority of the peers have reported losses in 2 of last 4 quarters. Prices have however kept up well.

- PE of Bandhan is the lowest in the peer group. However it is low because the peer group companies have depressed earnings reported in the last 4 quarters.

- In terms of PB, the valuations are in the mid-range at 4.93 times post IPO. The valuation looks expensive considering that 96% of Bandhan’s loan book is unsecured and they would be entering new categories which have lower margins.

- The D/E ratio at 0.15 (diluted post IPO) is the best and lowest and hence gives Bandhan scope to aggressively lend. The CAR of Bandhan stood at 26.4% for FY17 as against RBI’s minimum requirement of 15%, which indicates that it is adequately capitalized.

- The RoE is the highest at 25.01% and Bandhan has the lowest GNPA’s (9M FY18) amongst its peers. This is a positive. Bandhan also has the lowest cost to income ratio of 36.3%.

Positives for Bandhan bank and the IPO

- As a universal bank, Bandhan has flexibility to operate across multiple product lines and with few restrictions. It is the leader in the MFI industry as other players are Small Finance Banks or NBFCs.

- World Bank arm International Finance Corporation (IFC) is an investor/ promoter of Bandhan.

- Bandhan has a strong presence in East & NE India, which are more agriculture and agro-commodity intensive regions. We feel it may have high scope to grow and penetrate deeper here.

- Bandhan’s growth has been achieved despite difficult conditions in India’s MFI and banking industry. Events like the crisis in the southern state of AP in 2010, demonetisation in late 2016 and farm loan waivers, were challenges for the banking industry. But Bandhan did well.

- In MFI, achieving volumes of loans is a powerful advantage as the costs of reach and distribution are shared across many loans. With a good marketshare and presence in East & NE, it has an advantage.

- Bandhan has a large low cost distribution network. They operate in 33 States and UTs in India, reaching 1.2 crore customers. Bandhan’s distribution network is relatively low cost because of its ‘hub and spoke’ model of using DSCs and associate bank branches, and focus on tech initiatives, which reflects in their operating cost-to-income ratio of 35.4% & 36.3% for 9M FY18 & FY17, resp.

- The asset quality of Bandhan is stable with NNPA’s at 0.80% for 9M FY18. Financially the firm is well managed with excellent return ratios, good margins and tight controls on costs. This is a positive.

- Bandhan has a good management team. The founder, MD & CEO, Mr. Chandra Shekhar Ghosh, has 37 years of experience in Indian MFI. Members of their senior management have a track record that combines professional and entrepreneurial skills in microfinance and banking, with average 23.9 years of experience in finserv. 8 of 12 directors on the board are Independent Directors.

Risks and Negatives for Bandhan and the IPO

- The valuations are on the higher side in terms of P/B at 4.93 times (adjusted post IPO).

- Bandhan has a limited financial history and a rapidly evolving business which makes it difficult to evaluate their business and future operating results.

- Bandhan’s micro finance loan portfolio is not supported by any collateral that could help ensure repayment of the loan, and in the event of non-payment by a borrower of one of these loans, they may be unable to collect the unpaid balance.

- Bandhan handles cash in a high volume of transactions occurring through a dispersed network of branches and DSCs; as a result, they are exposed to operational risks, including fraud, petty theft and embezzlement, which could harm financial position.

- Bandhan’s business relies significantly on their operations in the East and NE states, and any adverse changes in the conditions affecting these States can adversely impact their business. As of FY17, roughly 81% of Gross loans were located in such areas.

- The microfinance sector is sensitive to economic, political and weather events

Overall Opinion and Recommendation

- Microfinance sector carries out the critical role of financial services penetration into rural India. MFI’s have been operationally under stress since 2017 due to demonetization and GST rollout. The earnings were impacted due to a spike in defaults and business disruption. However the current signs are that this impact is over and the rural economy & demand is regaining strength.

- Bandhan bank has a great brand recall, strong financial performance, good asset quality and an experienced management. It is the new MFI loans leader.

- Presence in underbanked East and NE regions and universal bank structure are key strengths.

- At a P/B of 4.93 times (post IPO), the valuation look expensive. However Bandhan has a focus and a leadership position. It also operates in niche geographies.

- Opinion: Investors can SUBSCRIBE to this IPO with a 2 year perspective.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake ownership or known financial interests in Bandhan or any group company. Punit Jain intends to apply for this IPO in the Retail category. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.