- Date 30th Nov; IPO Opens 30-2nd Dec, at ₹ 870-900/share

- Large Cap: ₹51,800 cr. Mkt cap; Sector – Insurance, Health

- Advice: SUBSCRIBE

- Why Buy Now: The waves of Covid have pushed SHI into losses but 1) we do not anticipate more severe waves in future, and 2) SHI should be able to recover through faster business growth and adjustment of prices for the covid pandemic. By having an IPO at this time, investors have an opportunity to buy SHI at low valuations We expect profitability in SHI by 2022, even as it grows rapidly in revenues and network. Once this happens, this IPO entry price will look reasonable.

- Risks: 1) Loss making entity, so this is a risky investment opportunity 2) Uncertain covid outlook 3) high competition 4) New infectious diseases 5) regulatory uncertainty.

- Opinion: Investors with a risk appetite can SUBSCRIBE to this IPO with a 2 year perspective.

Here is a note on Star Health and Allied Insurance IPO (SHI).

IPO Highlights

- Star Health IPO will open from Nov 30 – Dec 2 with a price band of ₹ 870 – ₹ 900.

- The firm will raise ₹ 7,249 crores, including fresh issue ₹ 2,000 cr. and offer for sale 5.83 cr. shares by promoters & shareholders, for max. ₹ 5,249 cr., together 14% of post IPO shareholding.

- Star Health is looking for a market cap of ₹ 51,796 cr.

- Promoters currently hold 66.22% stake and post-IPO this will come down to 58.3%. Public holding will increase from the current 33.78% to 41.70%. The quotas are QIB 75%, NII 15%, and Retail 10%.

- Promoters of Star Health are Safecrop Investments India LLP, WestBridge AIF I and Rakesh Jhunjhunwala. The shareholders selling shares in the IPO include promoter Safecrop Investments India LLP, and many other (public) shareholders.

- The grey market premium (GMP) of SHI has declined sharply to below ₹ 10 per share, according to people who deal in unlisted stocks; it has fallen from ₹ 90 per share last week.

- Objects – with the funds raised from fresh offering, SHI plans to augment the company’s capital base and maintain solvency levels.

- One lot size is 16 shares and Face Value is ₹ 10. Retail investors can bid for one or more lots, and a minimum of ₹ 14,400 or multiples of this, upto a maximum of ₹ 1,87,200 for 13 lots and 208 shares.

Introduction to Star Health and Allied Insurance

- Star Health and Allied Insurance is the largest private health insurer in India with a 15.8% share in FY21 (CRISIL Research). Started in 2006, it is #1 based on health GWP over 3 years.

- It had retail health GWP of ₹ 9,349 cr. in Fiscal 2021. SHI made a loss for the first time in 3 years in FY21 even as revenue rose, due to Covid.

- Its health insurance product suite insured 2.05 cr. lives in retail and group health, which accounted for 89.3% and 10.7%, resp, of total health GWP (Gross Written Premium) in FY21.

- It has a distribution network of 779 health insurance branches spread across 25 states and 5 UTs. Its agency distribution channel also includes corporate agent banks and other corporate agents, which accounted for ₹ 220.9 cr. and ₹ 19.1 cr., resp., of its GWP in FY21.

- Promoter of SHI are Safecrop Investments India LLP, WestBridge AIF I and Rakesh Jhunjhunwala.

- The proposed IPO will make SHI the fourth private sector insurance provider to list on Indian stock exchanges, following HDFC Life, ICICI Prudential Life and ICICI Lombard General.

- Star Health’s total number of individual agents grew at a CAGR of 27.3% from 2.9 lakh (Mar’19), to 4.6 lakh (Mar’21) and 5.1 lakh (Sept’21). Under the IRDA (Appointment of Insurance Agents) Regulations, 2016, insurance agents are only permitted to sell the policies of three insurers: one life insurance company, one non-life insurer and one health insurer.

- SHI has enabled online purchase of policies in as less as 5 minutes on website Starhealth.

- SHI has already allocated ₹ 3,217 cr. to 62 anchor investors today.

- Key leaders: V Jagannathan, Chairman & CEO, Dr. S. Prakash, MD (since ‘19), Anand Roy MD (‘19)

Fig 1a) Revenue Segments in FY21 and b) Industry Market Shares

Insurance 101, and Health Insurance in India

- Insurance is a very useful product. There are several types – Life, Health, Automobile, Property, Farm/crop, and all kinds of asset insurance products. Products are for retail or business consumers.

- Health insurance is a long term product. Having a health problem is not highly predictable, so it is bought so that in case a hospitalization happens, you are protected to the extent of Sum Assured.

- Salaried employees may get Group health insurance from their employer. They should check if their families are also covered – this may be an add-on. Non salaried need to buy on their own.

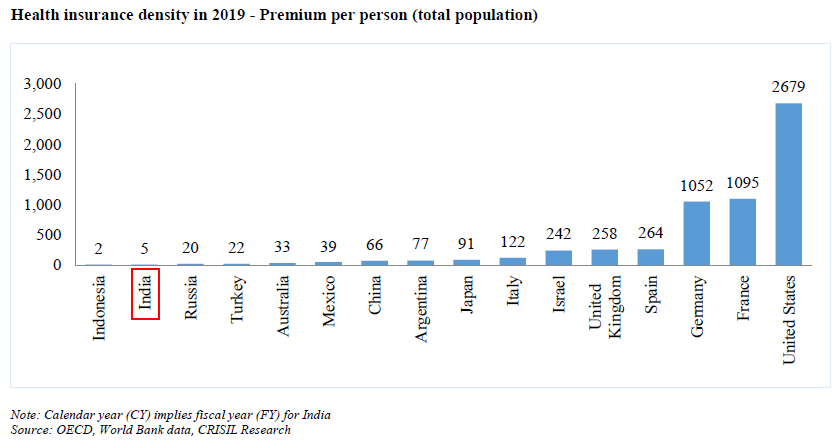

- The health insurance penetration in India is low at just 0.36% of GDP whereas the global average comes around 2% of GDP. Countries like the UK, China, Argentina and the United States have higher penetration level of 0.61%, 0.65%, 0.78% and 4.1%, respectively.

- The players are regulated by IRDAI (Insurance Regulatory and Development Authority of India) and is subject to regulatory uncertainty and compliance requirements.

Fig 2a) Penetration

Fig 2b) Premium per person

Fig 2c) Industry segments

- The average premium paid per person in India at $5 / ₹ 375 per year on average for the population.

- Health in India is a split sector – the govt. of India does offer public hospitals and facilities that are free, but there are insufficient facilities in most places to cover the population. Wherever govt. facilities are insufficient or inadequate, people have to pay and use private medical services.

- The Covid crisis of FY21 & FY22 has shown the importance of Health insurance. At the same time we can see India has low penetration of health cover, high out-of-pocket expenses, and only 10% of the population has insurance policies outside of government plans, according to CRISIL Research.

- The total expenditure spent on healthcare by the centre and states for FY20 was 1.6% of GDP, including establishment expenditure of salaries, gross budgetary support to various institutions and hospitals and fund transfers to states under centrally sponsored schemes such as Ayushman Bharat.

- Health insurance industry data shows the types of companies and product segments.

- Personal experience: As a customer of the Family Floater product from SHI, I had it for several years with no claims. About 3 years ago, I suddenly had to use the insurance for a hospitalization and operation. It was a relief that these were covered. The process was easy and a doctor came to verify the patient, operation and hospital. SHI finally reimbursed about 90% of my claim.

Financials of SHI

- Revenues have grown steadily, but PAT fell in FY21 & H1FY22 due to Covid.

- The cash flow for SHI is shown in Fig 3b. It’s clear that FY20 and FY21 have been negative for FCF.

Fig 3a) Financials, and Fig 3b) Free Cash Flow

Benchmarking

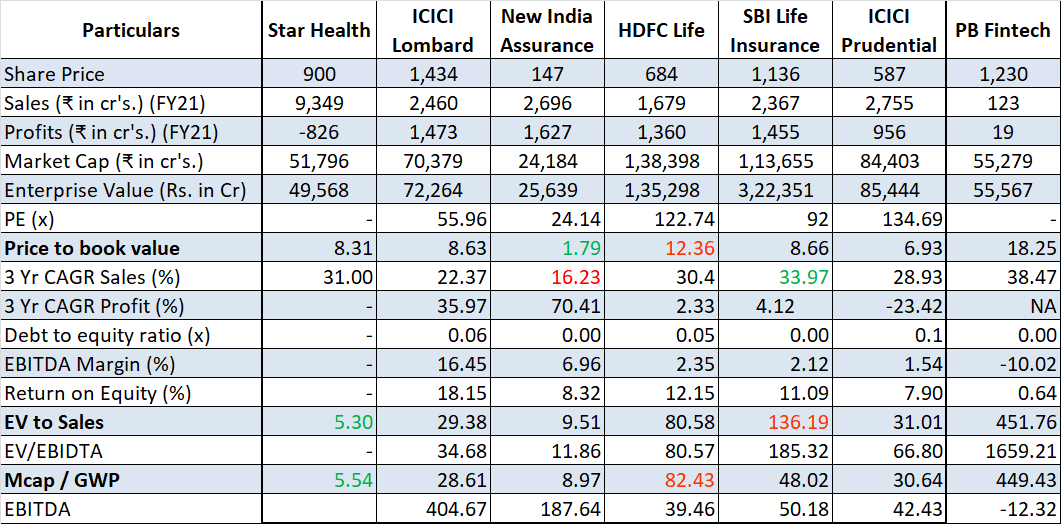

We benchmark SHI against listed insurance firms in India, and PolicyBazaar. See Fig 4.

Fig 4 – Benchmarking

- As a loss making firm, the PE is negative for SHI. As are the profits.

- On sales growth we can see that SHI is close to the leader, SBI Life. New India lags here.

- As a result, the key valuation parameters are P/B, EV/Sales and Mcap / GWP.

- The P/B of SHI is about average. New India is valued low partly as it’s a PSU. HDFC Life is expensive.

- On EV to sales, SHI is a value leader. Highest is SBI Life. On Market Cap to GWP, again SHI is the leader while HDFC Life is most expensive. On revenues, we can see that SHI is the leader. However, the loss making situation is marring the valuations of SHI on traditional parameters of PE and ROE.

- Putting this together, we sense that SHI is a valuable asset available at low valuations due to the covid related losses. It’s entirely possible that post covid, SHI may emerge quite profitable.

- Star Health stands out among other standalone health insurers (SAHI) in terms of size, strong growth rates (32% Gross Written Premium CAGR over FY18-21) and better operational performance which is reflected in pre-Covid numbers for the company (~93% combined ratio).

Positives for SHI and the IPO

- Largest private health insurance firm in India with leadership in the attractive retail health segment.

- There is low penetration of health insurance in India. Also Post covid, awareness of health insurance has risen. This category may continue to see high growth.

- The famous Indian investor Rakesh Jhunjhunwala has backed SHI as promoter. As he has a large following in India, this helps with publicity and investor confidence.

- India has an aggressive plan for vaccination and has covered a good proportion of population. The one dose number has crossed 100 cr. and two doses 37 cr. There is a plan for a booster dose too.

- SHI has a good brand, a national presence, and the largest network distribution in health industry.

- Diversified product suite with a focus on innovation and launch of new and specialized products.

- Strong risk management with superior claims ratio and quality customer services.

- Demonstrated track record of operating and financial performance.

- Low valuations as per benchmark analysis.

- The sector is divided 46-54% between PSU and private. There is ample opportunity to grow for SHI.

- The second wave was better handled by people & hospitals compared to the first. With this experience, any further waves should be handled better in terms of prevention and cure.

Risks and Negatives for SHI and the IPO

- In India we appear to be in a recovery from Covid, but we cannot accurately predict any 3rd/4th wave in India and the business impact of the same. Omicron is a new variant found recently also.

- The company has suffered a setback for the last 18 months due to covid, and has run into losses.

- In order to emerge from this crisis, SHI may have to raise the prices of its products.

- There are 29 active health insurance companies in India. It’s a competitive space and thus it may be difficult for any one company to dominate or win a 40%+ market share.

- Post covid, GoI may be forced to raise spending on healthcare, which is mostly free services.

- The Medical Council of India has been replaced by the National Medical Commission in FY20 for the purpose of medical education and medical professionals. The poorly regulated sector has seen shortages of doctors and nurses, and hopefully this will improve in future.

- Recent loss making firms that have IPO’ed had uneven results. Zomato and PolicyBazar have done well, but Paytm had a rough first week.

Overall Opinion and Recommendation

- Public sector healthcare is inadequate and of insufficient capacity. With rising medical services and medicine costs there is ample demand for health insurance.

- SHI has grown rapidly and is well focused on the health insurance sector.

- The waves of Covid have pushed SHI into losses but 1) we do not anticipate more severe waves in future, and 2) SHI should be able to recover through faster business growth and adjustment of prices for the covid pandemic.

- There is a massive growth opportunity for health insurance in India as affluence grows. This will also be driven by higher inflation in medical services.

- As the largest private player, SHI has an opportunity to grow the market and service the demand.

- We expect profitability in SHI by 2022, even as it grows rapidly in revenues and network. Once this happens, this IPO entry price will look reasonable.

- Risks: 1) Loss making entity, so this is a private equity type, risky investment opportunity 2) Uncertain covid outlook 3) high competition 4) New infectious diseases

- Opinion: Investors with a risk appetite can SUBSCRIBE to this IPO with a 2 year perspective.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake ownership or financial interests in Star Health or any group company. He has been a retail customer of SHI for 5+ years. Punit Jain intends to apply for this IPO. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from a RIA – Registered Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

Leave a comment