- Date: 18th Sept, 2020

- Price: ₹ 374

- Small Cap: ₹ 5,200 cr. Mkt cap

- Industry – Roads Construction

- Advice: Buy with a target of ₹ 810 in 2 years

![]()

Summary

- Overview: Dilip Buildcon is an EPC firm undertaking projects in India in the roads, bridges, tunnels, etc. DBL’s revenue in FY20 was ₹ 9,725 crore and profits ₹ 358 cr. DBL’s revenues, EBITDA and PAT have grown at 41.2%, 41.1 and 27.9% CAGR from FY11-FY20. It’s a small cap but a sector leader.

- Why Invest Now? Good growth in order book in Q1FY21. The Booked to Bill ratio rose to 2.84. Also DBL has diversified from primarily roads into attractive adjacent sectors like tunnels, mining, metros, airports and irrigation. It is also executing 2 large infra asset sale deals which will free up capital, improve returns, reduce debt and allow reinvestment in growth. The share is also sharply off 2018 highs and is available at a P/E of 18 times TTM. The macro is good with GoI investing heavily in infrastructure. Interest rates are falling and loans are easier to get.

- Key Risks: 1) high debt and large working capital requirement 2) pledged shares 3) high competition 4) covid and weather disruptions 5) Roads Sector perception

- Outlook: Investors can BUY the share a 2 year target price of ₹ 810.

Our other Roads related reports:

- H.G. Infra IPO – An Exciting Road Ahead – Feb 2018

- Here’s A Great Construction Achievement – July 2018

- Dilip Buildcon IPO – This Is A Rough Road – Aug 2016 (we have changed our opinion)

Here is our research report on Dilip Buildcon Ltd. (DBL).

Dilip Buildcon – Description and Profile

- Dilip Buildcon (DBL) is an Engineering, Procurement and Construction (EPC) firm undertaking projects in India in the roads, bridges, tunnels, mining, metros, airports and irrigation sectors.

- DBL’s revenue in FY20 was ₹ 9,725 crore and profits ₹ 358 cr. DBL’s revenues, EBITDA and PAT have grown at 41.2%, 41.1% and 27.9% CAGR from FY11-FY20.

- DBL owns 12,901 vehicles and construction equipments, and employs 33,700 people.

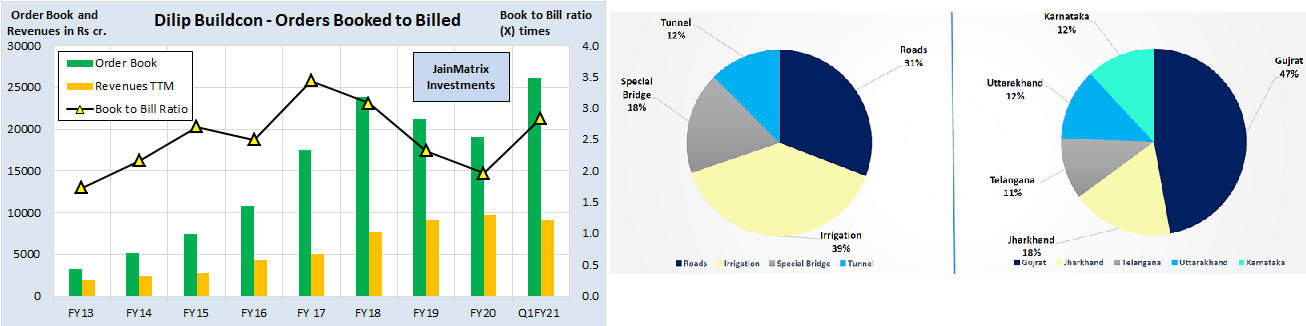

- DBL segment revenues for FY21 Q1 are: (a) Construction of roads and bridges – 88% (b) Mining – 1% (c) Irrigation projects – 1%. (d) Urban development – 10%

- DBL is MP based but in Fig 1b we can see that projects are from all over the country.

- As of Q1FY21, DBL had an order book of ₹ 26,115 cr. The Orders Booked to Billings ratio was at 1.96 times in Mar 20 has risen to 2.84 in Q1 giving good revenue visibility. Out of this 68% are central government projects and 32% state government projects.

- Dilip Suryavanshi is CMD. He has 34 years’ experience in construction, and is President of the MP Builders Association. Devendra Jain is the CEO-ED and has 19 years’ experience in construction.

- Shareholding of DBL is: Promoters -75%, MF – 9.5%, FII – 8.7%, Public – 6.7%.

JAINMATRIX INVESTMENTS – PRICING AND PAYMENT OPTIONS

Liked this report? Get such reports privately in your mailbox with a subscription.

Business Model, News and Updates for DBL

- DBL’s strategy going forward is to (a) focus on road EPC for government clients (b) divest BOT assets freeing capital (c) geographical diversification (d) projects clustering (e) Target smaller project size to reduce overdependence on large projects (f) Deleverage balance sheet.

Fig 1(a) – DBL Segment Revenue in FY20 and Fig 1(b) – State wise Order Book (clickable)

Fig 1(a) – DBL Segment Revenue in FY20 and Fig 1(b) – State wise Order Book (clickable)

- It has a policy of no subcontracting and no equipment on rental. This has helped it build good human resource and execution capabilities. They do a faster execution of projects. DBL has completed 90% of their projects early, and has received bonuses of ₹ 565 cr. from 2012-20.

- DBL carefully selects projects and strives for geographical clustering of these outside MP. This helps in utilization of construction assets and reduce environmental and forest clearance risks. It also paves the way for regional strengths. DBL leverages its manpower, equipment and materials and saves transportation costs, thus achieving economies of scale.

- Drones and UAV are emerging technologies used to reduce project time, improve safety and control project costs. UAV is used to collect engineering data at a construction site.

- GPS technology is used to track machine life, fuel usage, and consumables. It provides mapping and replays vehicle location history with real time alerts and notifications. Using this tech, DBL is able to guide drivers and operators, enabling fuel savings of ~25%.

- DBL has received a LoA for construction and upgrading of NH 131A near Narenpur to four-lane and near Purnea to two-lane with paved shoulders in Bihar on HAM mode, of value ₹ 1,960 cr.

- DBL in Aug 2018 won a contract of Pachhwara Central Coal Mine for 55 years valued at ₹ 32,156 cr., located in Jharkhand. The Pachhwara Block is reserved for Power Sector end use and was allotted to Punjab State Power Corp by GoI. DBL will develop this in consortium with VPR Mining where DBL will hold 74% equity. It expects to generate annuities of ₹600 cr. and margins in line with the current road business.

- In June 2012 Income Tax dept. conducted raids on promoter Dilip Suryavanshi, teacher-turned local business tycoon Sudhir Sharma and associates at 10 locations, including Indore and Bhopal in MP. The officers found incriminating documents related to tax evasion. The ED later sought details from the IT dept. regarding an alleged ₹ 140 cr. FEMA violation from South Africa. (TOI news).

- As a part of Business Continuity Measures (BCM), DBL imposed the (WFH) policy and this was identified as major relaxation for working in the COVID-19 pandemic environment.

Industry Outlook

- India has the 2nd largest road network in the world, aggregating to 61 lakh kms. Roads are the most common mode of transportation and account for 86% of passenger and 65% of freight traffic. In India, National Highways with length of 1.04 L km are just 1.7% of the road network, but carry about 40% of the road traffic. On the other hand, state roads and major district roads at the next level carry another 60% of traffic and account for 98% of road length.

- There are 2 central Govt. bodies which award road projects, NHAI which is in charge of the National Highway Development Program (NHDP) and Ministry of Road Transport and Highways (MoRTH), which covers highways not under NHDP.

- From the Fig 2 below we can see the transition of projects awarded to new models recently.

Fig 2 – Road Project Models (click on images to enlarge)

Fig 2 – Road Project Models (click on images to enlarge)

- NHAI has set an aggressive timeline for highways, expressways and economic corridors, to be ready by Mar 2025. The combined length of these is 7,800 km and would require investment of approximately ₹ 3.3 Lakh cr. in the next five years.

- NHAI has constructed 3,979 km of NHs in FY19-20, the highest ever achieved in a financial year.

- GoI has envisaged a highway program Bharatmala Pariyojana for development of 65,000 km of NHs. Under Phase-I of the program, GoI has approved implementation of 34,800 km of NH projects with a stiff target of 5 years with an outlay of ₹ 5.35 L cr.

- Highway construction in India increased at 21.4% CAGR between FY16-19. In FY19, 10,855 km were constructed, and GoI has set a target for constructing 12,000 km of NH in FY20.

- The development of road infra in India is witnessing great momentum and construction of roads per day hit a new high of 27 kms/day for FY18, which is much higher than what was achieved earlier.

Fig 3 – Construction, Outlay and Projects Awarded

Fig 3 – Construction, Outlay and Projects Awarded

- Under Union Budget 2020-21, GoI allocated ₹91,823 cr. to MoRTH, and plans to invest ₹ 15 lakh cr. in the next five years. CRISIL expects investment in roads to double to ₹10,70,000 cr. over 5 years.

- The GoI approved the Bharatmala program under which 53,000 kms of NHs have been identified to bridge critical infra gaps. It will give the country 50 national corridors as opposed to 6 at present. Phase I will be over FY18-22 with 24,800 kms of construction expected.

- Construction of roads generates employment and contribution to growth in GDP.

- In recent times, the InvIT structure has become popular for holding and listing of infra assets. This structure is tax efficient and allows infra firms to monetize their assets.

Stock evaluation, Performance and Returns

- DBL’s revenues, EBITDA and PAT have grown at 41.1%, 41% and 27.9% CAGR from FY11-20.

- DBL’s price history is detailed in Fig 4. The share price high was ₹ 1,247.5 in May 2018.

Fig 4 – Price History

Fig 4 – Price History

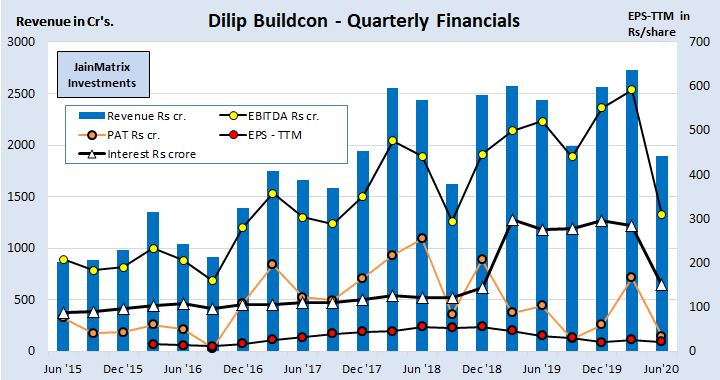

Fig 5a – DBL Financials (click on images to enlarge)

Fig 5a – DBL Financials (click on images to enlarge)

- DBL’s revenue was ₹ 1,892 cr. in Q1 FY21, a decrease of -17% YoY. PAT also fell by -70% YoY to ₹ 34 cr. in Q1 FY21 largely due to the impact of covid-19 and lockdown, see Fig 5a. We can also see that Sept quarter is typically weakest, mostly as the rains slow the construction for roads.

- They paid a dividend of ₹ 1/share (Rate of 1%) in FY20, a yield of 0.11% which is very small.

- DBL has not been able to generate Free Cash Flow in the last 6 years in-spite of good Cash from Operations due to the large CAPEX needs . This is common across the industry. See Fig 5b – Cash Flow. We can also see some of the key Financial metrics in Fig 5c.

Fig 5b – DBL Cash Flows and Fig 5c – Financial Metrics

Fig 5b – DBL Cash Flows and Fig 5c – Financial Metrics

- It had a Booked to Billed ratio of 1.96 (FY20) which rose to 2.84 in Q1FY21 on wins, see Fig 5d.

- DBL has a ROE of 11.21% in FY20.

- It secured record orders worth ₹ 10,703 cr. in Q1FY21 across 4 sectors and 5 states including 2 new states of Uttarakhand and Bihar, see Fig 5e.

- It is getting more diversified, and now has over 50% of Order Book from non – Road sector.

- The promotors hold 75% shares. However 21.5% of shares have been pledged by them.

- In Fig 6a, we see the PE chart for DBL has a historic average of 16.25 times and a range of 7.5-25 times in 4 quadrants. Today at 23.5 times, it is trading near its historic averages.

- In Fig 6b we can see that the EPS TTM had decreased in the last year due to nationwide lockdown.

Fig 5d – Order Book to Billed and Fig 5e – OB in Q1FY21

Fig 5d – Order Book to Billed and Fig 5e – OB in Q1FY21

Fig 6a – Price – PE graph

Fig 6a – Price – PE graph

Fig 6b – Price – EPS graph

Fig 6b – Price – EPS graph

Benchmarking and Financial Estimates

Fig 7a – Benchmarking

Fig 7a – Benchmarking

We benchmark DBL against peer road construction companies. See Fig 7a.

- DBL appears to be at slightly expensive valuations in terms of P/E and P/B.

- Sales and profits growth while impressive is not the highest.

- Debt equity ratio is high at 2.62, a problem in the sector but DBL is highest in this peer group. However Net Debt to Equity is 0.92. EBITDA and Profit margins are low. However, their strategy helps DBL grow its revenues faster. RoE, RoCE are fair.

- Financials of DBL are projected for 2 years in Fig 7b basis order book, corporate plans, management guidance and analyst judgement.

Fig 7b – Financial Projections

Fig 7b – Financial Projections

Strengths of DBL

- DBL is a sector leader in Indian roads EPC. It has a large order book and rising revenues.

- DBL has a good pan India presence. It operates in geographical clusters for projects which helps with efficiency and asset utilization. So DBL has an efficient business model. The execution through strong operations helped DBL receive early completion bonuses for many projects.

- DBL has seen a strong growth in financials and order book. In Q1FY21, it has improved order book and also diversified into new infra verticals like tunnels and irrigation projects, amid the lockdown challenge.

- Diversification by DBL from roads to a number of adjacent infra sectors is a sign of aggression and dynamism. There are business model synergies with these sectors and they are high potential sectors.

- The sale of road assets to Shrem and Cube Highways is helping reduce capital tied up and so debt is being reduced. DBL should be able to sharply reduce its interest payments by continuing to sell road assets as well as take advantage of the lower interest regime and reduce cost of loans.

- Key assets are large employee strength and construction assets. It also has a factory campus in Bhopal.

- Road projects used to be riskier earlier as NHAI etc. used to bid out projects while having acquired only a small portion of the land required for construction. Projects used to get delayed and the Construction firm used to suffer. This has now changed and most of the land is acquired before bidding it out.

- Promoters Dilip Suryavanshi, Devendra Jain and top management are highly experienced in infra space.

- Largest Caterpillar equipment fleet owning company in Asia.

Weaknesses and Risks of DBL

- All firms in the roads EPC sector face issues like high working capital requirement, long project gestation periods, govt. clearances, govt. customers and PIL/ litigation issues. DBL is no exception.

- D/E is high at 2.62 times and interest payments have been rising. However Net Debt to Equity is 0.92.

- The promoter Dilip Suryavanshi is alleged to have a close relationship with the CM of MP, Mr. Shivraj Singh Chauhan. However he became CM again only recently. Further their business has gone national.

- The 2012 IT Department case of tax evasion and FEMA is an issue. While the firm is attempting to settle this issue, there is no clarity on additional tax liabilities, or even more such cases against the firm.

- The 3 promoters are paid high salaries. This is not shareholder friendly. But it is in acceptable limits.

- The promoter has pledged 21.5% of shareholding, however this is only till award of certain projects. The pledges will be released as soon as they receive financial closure on the same from banks. But pledging of shares by promoters reduces the stability of the share in the market.

- Competition is intense in road projects, particularly in EPC projects rather than BOT.

- Sector perception: the roads construction sector is seen as a tough business with challenges like litigation, high working capital, opaque GoI clients and a difficult business model.

- The Land acquisition Act in India specifies the process and compensation. It has undergone several changes recently, and we expect more changes. The uncertainty affects the roads EPC industry.

- BOT projects are evaluated based on traffic projections. In this sector, BOT companies are facing financial pressures due to aggressive projections during evaluation and high competition during bidding.

- High interest payments compared to earnings.

- The covid infection affected operations in Q1, but by August, labour availability is 90% of normal.

Overall Opinion

- There is an urgent need to build infrastructure such as roads and highways. This is reflected in the Indian budget allocations. Project awarding and completion has never been so fast in roads sector.

- In this sector Dilip Buildcon has built a good momentum of business, and has a national presence, a fast growing order book that is diversifying from roads to attractive adjacent sectors like bridges, tunnels, mining, metros, airports and irrigation. It has a good strategy and business model.

- Road projects undertaken include work on BOT, HAM and EPC models. However two recent large deals of sale of infra assets is releasing tied up capital and helping focus on core EPC.

- Key Risks: 1) high debt an large working capital requirement 2) pledged shares 3) high competition 4) covid and weather disruptions 5) Sector perception

- Excellent financial management, galloping revenues and order book, sectoral tailwinds along with a low price entry point makes Dilip Buildcon an excellent BUY.

- Investors can BUY the share with a 2 year price target of ₹ 810.

Disclosure, Disclaimer and Assumptions

The target price has been arrived at using financial projections in Fig 7b and a target PE of 15 times. This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Punit Jain has an equity ownership (<1%) in DBL since Sept 2018. Other than this he has no financial interests in DBL or any group company. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

Leave a comment