- Date 28th Sept; IPO Opens 29-01st Oct at ₹ 552-554

- Valuations: P/E 25.4 times TTM

- Mid Cap: ₹ 7,024 cr. Mkt cap

- Industry – Asset Management

- Advice: AVOID

![]()

Summary

- Key Strengths: UTI AMC is the second largest AMC in India in terms of Total AUM and the eighth largest in terms of mutual fund AUM. UTI has a strong brand due to its presence in India for 55 years. Valuations are low in terms of P/E. This allows some upside potential to investors. With a GoI institutional ownership, the firm is perceived as safe and stable. Post IPO, T Rowe Price will continue to be the largest shareholder.

- Risks: 1) The financials of UTI have been weakening over the last 3 years. 2) The share of equity MFs has reduced in percentage, as the debt, liquid, hybrid, PMS and pension products grew faster. 3) Competition from the top 5 MFs is intense. With digital sales and distribution networks growing in importance for sales, UTI may have to invest more in sales and marketing. 4) AMCs are closely regulated by SEBI and are subject to changes or tightening of norms.

- Opinion: UTI is a fair business available at a low valuation. AVOID this IPO.

Here is a note on UTI Asset Management Company (UTI) IPO.

IPO highlights

- The IPO opens: 29/Sept – 01/Oct 2020 with Price band: ₹ 552-554 /share. Listing is 12/Oct.

- Shares offered number 3.89 crore. The FV of each is ₹ 10 and market Lot is 27 nos.

- The IPO is of ₹ 2,160 cr. for 30.75% equity by institutions SBI, LIC, and BoB who are selling 1.05 cr. shares each, and T Rowe Price and Punjab National Bank are selling 38 lakhs each.

- UTI AMC is a institutionally owned firm with T Rowe Price (26%), and PNB, SBI, LIC, and BoB holding 18.2% each being the major shareholders.

- The IPO share quotas for QIB, NIB and retail are in ratio of 50:15:35.

- Grey market premium has dropped from ₹ 75 to ₹ 45 in the past few days of market volatility.

Introduction to UTI AMC

- UTI AMC is the second largest AMC in India in terms of Total AUM and the eighth largest in terms of mutual fund AUM (June 30, 2020, by CRISIL). UTI AMC and its predecessor (Unit Trust of India) have been active in asset management for more than 55 years, having established the first MF in India.

- Revenues and profit were ₹ 855 cr. and ₹ 276 cr. resp. for FY20. See Fig 1a. It has 1,386 employees with 658 in sales, 47 in investment, 278 in Support/other and 403 non-officers.

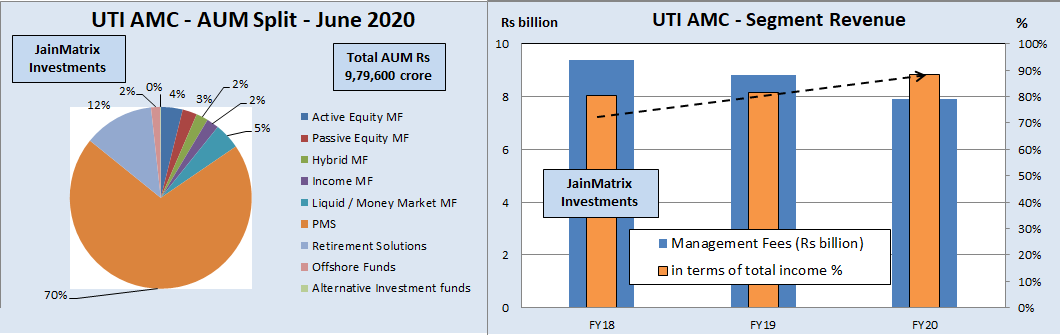

- It has an AUM of ₹ 9,79,600 cr. in FY20 split between MFs (1,51,500 cr.) and Others (8,28,100 cr.).

- We can see that Revenues, EBITDA and PAT have been falling for the last 3 years. See Fig 1a.

- FY21-E is a projection based on Q1FY21 results and can be lower also.

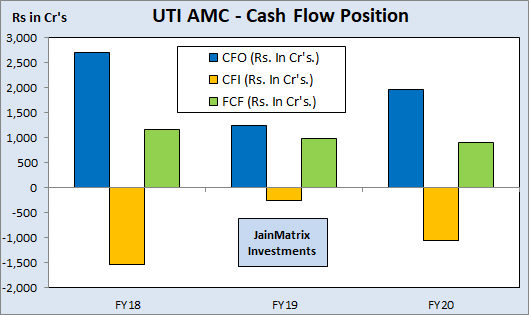

Fig 1a – Financials and Fig 1b – Free Cash Flow

Fig 1a – Financials and Fig 1b – Free Cash Flow

- Free Cash Flow has been positive but is also falling, See Fig 1b.

- Mutual Funds are further split as equity oriented and others. See Fig 2a. UTI manages 153 domestic MF schemes, comprising equity, hybrid, income, liquid and money market funds as of June 30, 2020.

- The market share of MF AUM is 5.6% among AMCs see Fig 2c.

- Its distribution network includes 163 UTI Financial Centers, 257 Business Development Associates and Chief Agents and 43 other Official Points of Acceptance, most of which are in each case located in B30 cities. Its Independent Financial Advisors (IFAs) channel includes 53,000 IFAs.

- UTI AMC has four sponsors SBI, LIC, PNB and BOB, each of which has GoI as a majority shareholder. It also has a global asset management company T. Rowe Price International Ltd as one of its major stakeholders with a 26% stake in the Company.

- Post IPO, T Rowe Price will continue to be the largest shareholder. T Rowe Price is a USD 1 trillion (75 lakh crores INR) global asset manager based in USA.

- UTI AMC has 11 million live folios making up 12.8% of client base of the Indian MF industry.

- Leadership is Dinesh Mehrotra (Non-Exec Chairman Dir.), Imtaiyazur Rahman (Dir.- CEO), Amandeep Chopra (Gr. President, Head Fixed Income) and Vetri Subramaniam (Gr. President, Head Equity).

Fig 2(a) – UTI AUM split – June 2020, 2(b) UTI Segment revenues and 2(c) Market share

Fig 2(a) – UTI AUM split – June 2020, 2(b) UTI Segment revenues and 2(c) Market share  Fig 3 – Shareholding Pre and Post IPO

Fig 3 – Shareholding Pre and Post IPO

MF Industry Outlook and Trends

- The economy has seen financial events such as demonetization, RERA implementation, GST and a crackdown on black money and shell companies. All these have rekindled interest in financial assets as compared to real estate and gold which were the most popular earlier.

- The Indian MF industry as a percentage of GDP increased from 4.7% in FY05 to 10.9% in FY20. This is much below the global average of 55%. There should be a steady growth in MF industry size.

- The regulations and disclosures around MFs have ensured good traceability and audit trails. SEBI has promoted MFs as good entry level equity and debt products, and MF asset growth has been good.

- The growth in the AUM has been supported by a favorable macro environment, the rising of capital markets, foreign fund inflows as well as growing investor awareness and trust in the MF products.

- There are 44 AMCs registered in India. But the top 10 AMCs having 83% of the industry AUM, see Fig 1c. SBI, HDFC, ICICI Prudential AMC, Aditya Birla and Nippon are the 5 largest MFs.

- Average MF AUM grew at 13% CAGR of from ₹7.6 trillion in Mar 2010 to ₹27 trillion as of Mar 2020.

- Global asset management firms have struggled in India as independent MF firms. Many sold out and exited. They have had a better success rate on partnering with Indian firms as the MF JV promoter.

- The regulator prescribes maximum Total Expense Ratios (“TERs”) for schemes, which are calculated by dividing the total costs of the fund by its total average assets. Aggregate scheme expenses, including all fees, commissions, costs, charges, and expenses, must not exceed the applicable TER for a scheme. TER is higher for equity MFs and lower for debt.

Benchmarking

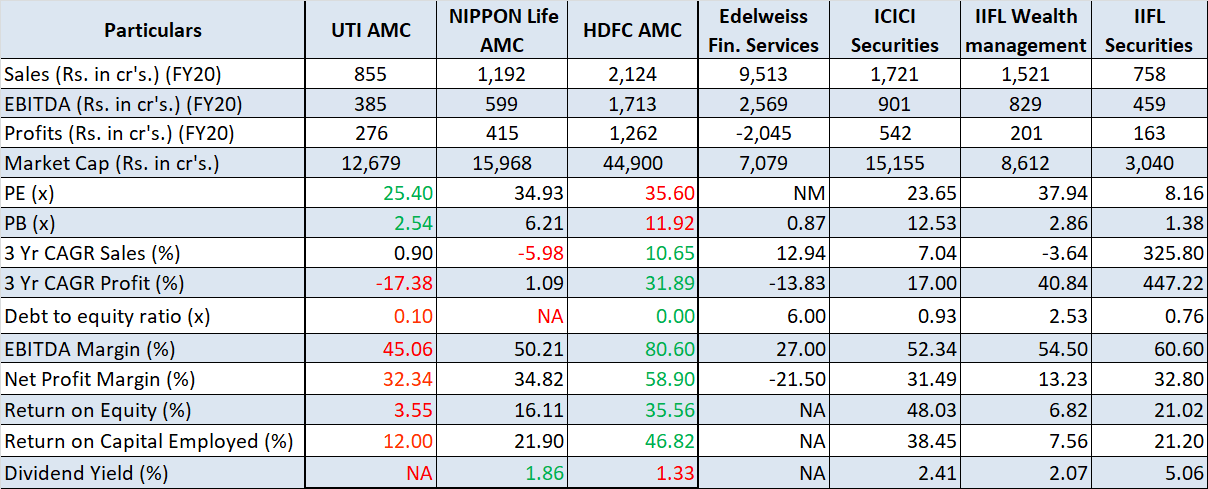

We benchmark UTI AMC against 2 AMC firms, and 4 brokerages and wealth managers. See Exhibit 4.

Exhibit 4 – Benchmarking

Exhibit 4 – Benchmarking

- We can see that of the 3 AMCs, HDFC comes out leading on most parameters except valuations and dividend yield. UTI leads only in valuations.

- Our conclusion is that UTI is a ‘fair business available at a good price’.

Positives for UTI AMC and the IPO

- UTI has a strong brand due to its presence in India for 55 years.

- Valuations are low in terms of P/E and P/B. This allows some upside potential to investors.

- It is a large firm and has quasi government brand. Operations are all India.

- The AUM by UTI is large, and particularly in Retirement it is a leader.

- It is in the top 10 firms by MF AUM.

- With a GoI institutional ownership, the firm is perceived as safe and stable.

- Post IPO, GoI institutional ownership will fall to 49%, and may allow it to function like a private firm.

- With financialization of savings growing, UTI should be able to grow AUM.

- UTI has an experienced and stable management & investment teams.

- T Rowe Price may take an active role in UTI, buy out shares from the market and take over UTI (it will trigger an open offer requirement) in future.

Risks and Negatives for UTI and the IPO

- The key financials of UTI have been weakening over the last 3 years.

- Partly this was because in 2019, SEBI reduced the TERs allowed for all MFs, impacting revenues and profits. AMCs are closely regulated by SEBI and is subject to changes or tightening of norms.

- The equity part of UTI MFs reduced in percentage, as debt, liquid and hybrid products grew faster.

- Competition from the top 5 MFs is intense. With digital sales and distribution networks growing in importance for sales, UTI may have to invest more in sales and marketing.

- In July 2014, the holding period for long-term capital gains tax on debt MFs was increased from 12 to 36 months. It is possible that such regulatory changes can affect their business in future.

- The tax on LTCG from equity was introduced in budget 2018 in Feb at 10%, from zero earlier. This caused a correction in markets, particularly the mid and small cap stocks, and MFs.

- Competition to the MF industry is from alternatives like the PMS industry, AIF/ Hedge Funds, Private equity markets and direct equity advisory. Many of these are the next steps for MF investors after they have started their investment journey with MFs.

Overall Opinion and Recommendation

- Mutual Funds industry in India has benefited from the financialization of assets, the growth of the digital economy and the entry of a wave of new investors in recent years.

- However growth may be concentrated among the top 5-6 firms which already command 57% share.

- UTI has a strong brand due to its presence in India for 55 years. Valuations are low in terms of P/E. But we can see that in last 2-3 years financials have weakened. While AUM has increased, UTI is big in low margin areas like retirement, pension and GoI PMS. We perceive UTI as a fair business available at a low valuation in IPO.

- Risks: 1) The financials of UTI have been weakening over the last 3 years. 2) The equity share of MFs has reduced in percentage, as the debt, liquid, hybrid, PMS and pension products grew in share. 3) Competition from the top 5 MFs is intense. With digital sales and distribution networks growing in importance for sales, UTI may have to invest more in sales and marketing. 4) AMCs are closely regulated by SEBI and are subject to changes or tightening of norms.

- Opinion: Investors can AVOID this IPO.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake ownership or known financial interests in UTI AMC. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

Leave a comment