- Date 23rd Feb

- IPO Opens 26-28th Feb with price range Rs. 263-270

- Small Cap: Rs. 1,760 cr. Mkt cap

- Industry – Roads Construction

- Valuations: P/E 32.9 times TTM, P/B 3.7 times (Post IPO)

- Advice: SUBSCRIBE

Summary

- Overview: HGI is a Jaipur based infrastructure construction, development and management firm with a focus on road projects, including highways, bridges and flyovers.

- Revenues and profit for FY17 were Rs. 1,059 cr. and Rs. 53 cr. HGI’s revenues, EBITDA and PAT grew at 34.3%, 27.5% and 37.0% CAGR in 5 years.

- HGI has a good 5 years performance where it has emerged as a rising star. The healthy order book, roster of completed roads projects and fair financial controls are impressive.

- At a P/E of 32.9 times (adjusted post IPO), the valuations of the IPO appear to be high. However earnings growth is likely to be at a faster pace due to reduced interest costs, better efficiencies and sectoral traction. Good track record, robust financial performance, sectoral tailwinds and an experienced management team makes this IPO attractive.

- Key Risks: 1) Project execution delays 2) Labor unavailability 3) Intense competition.

- Opinion: Investors can SUBSCRIBE to this IPO with a 3 year perspective.

Here is a 5 minute video on HG. Infra Engineering IPO.

Here is a note on H.G. Infra Engineering (HGI) IPO.

IPO highlights

- The IPO opens: 26-28th Feb 2018 with the Price band: Rs. 263-270 per share.

- Shares offered to public number 1.71 cr. The FV of each is Rs. 10 and market lot is 55.

- The IPO will raise Rs. 462 cr. by selling 26.26% of post IPO equity. The offer will be completed via an Offer for Sale (OFS) of Rs. 162 cr. and also by issuing fresh shares of Rs. 300 cr.

- The promoter group owns 100% (no private equity ownership) which will fall to 73.7% post-IPO.

- The selling shareholders are Hodal Singh, Harendra Singh, Vijendra Singh and Girish Singh of the Promoter family. They are selling 8.85% of their pre-IPO stake in HGI and are only part exiting.

- The net proceeds from fresh issue of shares will be utilized as follows:

Exhibit 1 – IPO proceeds

- The IPO share quotas for QIB, Non Institutional Buyer (NIB) and Retail are in ratio of 50:15:35.

- The unofficial/ grey market premium for this IPO is Rs. 20-25/share. This is a positive.

Introduction

- HGI is a Jaipur based infrastructure construction and development firm with a focus on road projects like highways, bridges and flyovers. Their main segments are (i) providing engineering, procurement and construction (EPC) services on a fixed-sum turnkey basis and (ii) EPC work for components of projects, primarily in the roads and highway sector.

- HGI’s FY17 revenue, EBITDA and PAT were Rs. 1,059 cr., Rs. 124 cr. and Rs. 53 cr. resp.

- HGI has also currently undertaking 2 water supply projects in Rajasthan on turnkey basis which includes the designing, construction, operation and maintenance of the project.

- HGI is active across various states like Rajasthan, UP, Haryana, Uttarakhand, Maharashtra and AP. During the last 5 years, HGI has completed 13 projects above the contract value of Rs. 40 cr. in the roads and highways sector aggregating to a total contract value of Rs. 1,675 cr., which included construction, improving, widening, strengthening of 2 and 4 lane highways, construction of high level bridge and of earthen embankment, culverts and cart track underpasses.

- As on Nov 30, 2017, HGI had 21 ongoing projects in roads & highways which includes construction, improving, widening, strengthening, upgradation and rehabilitation of 2, 4 and 6 lane highways, construction of high level bridge and construction of road network. This order book was Rs. 3,585 cr.

- HGI is pre-qualified to bid independently on an annual basis for bids by NHAI (National Highways Authority of India) and MoRTH (Ministry of Road Transport and Highways) for contract values of up to Rs. 806 cr. based on HGI’s technical and financial capacity as on FY17.

- HGI’s public sector clients include NHAI, PWD, MES and Jaipur Development Authority. They have also executed road construction contracts as a sub-contractor for private sector clients such as Tata Projects and IRB-Modern Road Makers.

- HGI’s equipment base comprised of 1,064 construction equipment. Also HGI has employed 2,447 employees which includes 2,130 skilled workers like engineers and managers.

- As of Nov 30, 2017, HGI had a total order book of Rs. 3,709 cr., consisting of 21 projects in the roads and highways sector, 4 civil construction projects and 2 water supply projects. See Fig 2.

Fig 2 – HGI’s order book by state and client type

- Leadership is Harendra Singh (CMD), Vijendra Singh (Whole Time Director) and Rajeev Mishra (CFO).

News, Business Model and Strategies of HGI

- Some impressive completed projects are 1) Yamuna Expressway in Noida, UP, 2) 4 laning of Jaipur-Tonk-Deoli project (Raj.) 3) Construction of Kuberpur to Fatehabad Road, Agra-Inner Ring Road (Phase-I) Agra, UP and ongoing 4) Rehabilitation and Up-gradation of Amravati-Nandgaon-Morshi-Warud-Pandhurna NH-53 (Mah.)

- HGI’s business strategies are:

- To focus on the EPC business in roads & highways sector and enhance execution efficiency.

- Selectively expanding its geographical footprint in states such as Gujarat, Punjab and MP, which have favorable geographic and climatic conditions, other than Rajasthan and Mah.

- Selectively explore hybrid annuity model (HAM) to grow its project portfolio.

- Business Model: HGI follows a evaluation process during pre-bidding stage, which involves technical surveys, feasibility studies and analysing the technical and design parameters and the cost involved in undertaking the project. This approach enables them to bid at competitive prices and successfully win projects. Once they win a bid, their focus is to ensure high quality of construction during execution, as a result of which, they are able reduce maintenance and repair costs and realize higher margins during the operation & maintenance stage.

Roads Infrastructure Industry Outlook in India

- India has the 2nd largest road network in the world, aggregating to 61 lakh kms. Roads are the most common mode of transportation and account for 86% of passenger traffic and 65% of freight traffic. In India, national highways with length of 1.04 lakh kms constitute a mere 1.7% of the road network, but carry about 40% of the total road traffic. On the other hand, state roads and major district roads at the next level carry another 60% of traffic and account for 98% of road length.

- In FY16, the road transport sector contributed 3.2% to the Indian GDP.

- Road transport is the most widely used mode of transport for freight and passengers. In Fiscal 2017, 64.5% of freight was carried by roads as compared to railways, from 56% in FY2010.

Key growth drivers for road sector are as follows:

- Rise in GoI investments, reforms and higher budgetary support. CRISIL Research expects investment in road projects to double to Rs. 10.7 tn. over the next 5 years. Investment in state roads is expected to grow steadily, and rise at a faster pace in case of rural roads, on account of higher budgetary allocation to Pradhan Mantri Gram Sadak Yojana (PMGSY) since FY16. The GoI has approved the Bharatmala programme under which 53,000 kms of national highways have been identified to bridge critical infrastructure gaps. Bharatmala will give the country 50 national corridors as opposed to 6 at present and Phase I will be implemented from 2017-18 to 2021-22.

- Policy changes to drive execution of national highway projects. Execution of national highway projects declined in the past two years on account of the private developers’ weak financials and unwillingness of lenders to provide further credit to infra companies. To clear this backlog, NHAI terminated projects and accordingly, work on 5,500 kilometers of length was stalled. To put execution back on track, the NHAI re-awarded almost 1,000 kilometers of the terminated projects.

- New region-specific initiatives to drive growth in road network. The GoI has taken new initiatives to build state roads. MoRTH has set up the National Highways and Infra Development Corp which will award national highway projects in border areas and in the north-east states. Apart from these projects, the Bharat Mala programme has also been proposed to build new roads along the border.

- Between FY18 and FY22, it is expected that an investment of Rs. 4.30 tn. would be made in the next 5 years for national highways, up 2.9 times compared with the past 5 years. Notably, the government will account for more than half of the investment.

Financials of HGI

- HGI’s revenues, EBITDA and PAT grew at 34.3%, 27.5% and 37% CAGR in 5 years, see Fig 3.

- The margins fell significantly in FY14-15 impacting profitability, because of rising commodity prices (for fixed-price contracts) and idling of capacities as execution could not begin on many new projects. The slowdown was common across the industry.

- Fig 3 – Financials

- HGI had a RoE of 30.3% in FY17 while the 3 year average RoE stood at 25.7% (FY15-17). The RoCE stands at 36.4%. These return ratios are high.

- HGI has been Operational Cash flow positive in all the last 5 financial years from FY13-FY17. This is a positive. Over FY13-15, HGI repaid its borrowings and funded CAPEX from internal accruals. However since FY16, CAPEX rose sharply and were funded by borrowings. See Fig 4.

- The current D/E ratio is 1.72:1 which is high which will fall to 0.70 post IPO.

- Fig 4 – HGI Cash Flow

- Because of high Capex, HGI has not declared any dividends in the last 5 years.

- Remuneration paid to the Key Management Personnel (KMP) +1 was Rs. 6.27 cr. for FY17, and 11.75% of PAT. Another Rs. 1.54 cr. was spent on insurance premiums for KMP. See Exhibit 5.

- Exhibit 5 – Renumeration

- HGI had an equity base of 5.4 cr. shares pre-IPO. Post the issue of fresh shares, the equity base will stand at 6.51 cr. (assuming fresh shares are issued at UMP of Rs. 270/share). This means the asking FY17 P/E is 27.4 (pre-IPO) and 32.9 (diluted post-IPO).

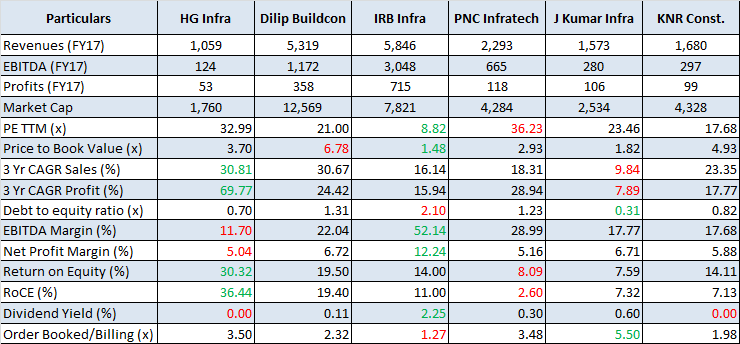

Benchmarking

We benchmark HGI against other listed infrastructure construction companies. See Exhibit 6.

- Exhibit 6 – Benchmarking

- The PE post IPO is high, so pricing appears aggressive, as seen with IPOs, a negative.

- The sales growth is excellent, comparable to sector leader, Dilip Buildcon. Profit growth is good also, partly due to a recovery from a slowdown in 2014.

- The post IPO D/E looks reasonable and is much better than a few of its other peer members. The IPO being partly fresh issue will help to reduce debt burden.

- The RoE at 30.3% and RoCE at 36.4% is excellent, high in the industry. This is a positive.

- HGI had the lowest EBITDA margin in the industry. However in H1 FY18, EBITDA margin is improving, due to better scale and efficiency in operations.

- PAT margins may improve due to lower interest costs going forward.

- Orders booked to Billings looks healthy and indicates over 3 years of revenue visibility.

- Putting it together HGI looks like a firm at the start of a high growth phase that can be accelerated by this IPO.

- Dilip Buildcon has done very well in last 2 years since IPO, and so is the sector leader. IRB looks undervalued and profitable. See our recent IRB report – In INVIT We Trust

- Also see our Roads Sector Note – THE ROADS SECTOR – IS IT A REVIVAL?

Positives for HGI and the IPO

- HGI has strong project management and execution capabilities. It also owns its construction equipment needed for ongoing projects. This helps control costs, and improves reliability.

- We can see a healthy order book; also HGI is pre-qualified to bid independently for project tenders by NHAI and MoRTH. This provides enough head room for faster growth.

- HGI’s management team is qualified and experienced in the construction industry. The Promoters Girish Pal Singh, Vijendra Singh and Harendra Singh have 20 years of infra sector experience.

- HGI has evolved from a sub-contractor to independent EPC firm, and subcontracting work has reduced to about 30% of revenues. Thus HGI is successfully moving up the value chain.

Risks and Negatives for HGI and the IPO

- The valuations appear on the higher side among peers as P/E is 32.9 times (adjusted post IPO).

- As HGI takes up projects on HAM in future compared to EPC, its working capital may increase.

- With no private equity ownership, HGI will transition from a family owned firm suddenly to a public listed firm. This change will have to be handled carefully, including disclosures.

- All firms in the sector face business risks like high working capital requirement, long project gestation periods, govt. clearances, local public opposition and PIL/ litigation issues.

- Delays in the completion of construction of current and future projects is a risk. A significant part of business is with GoI and any change in govt. policies or delays in payment are a risk.

- The firm has a business concentration in Raj. and Mah. with 96% of orders from there. But HGI is quite capable of growing a pan India footprint given good opportunities and projects.

- Competition is intense in road projects, particularly in EPC projects rather than BOT.

- HGI’s business is manpower intensive and any nonavailability of employees or labor issues can have an adverse impact on operations.

Overall Opinion and Recommendation

- The GoI has over the last few years and in Budget 2018 emphasized the roads and infra push in terms of budgets and ministry focus. This long suffering Roads sector has seen a revival in last 2-3 years is now expected to be a significant beneficiary of govt. spending.

- HGI has a good 5 years performance where it has emerged as a rising star. The healthy order book, roster of completed roads projects and fair financial controls are impressive.

- At a P/E of 32.9 times (adjusted post IPO), the valuations of the IPO appear to be high. However earnings growth is likely to be at a faster pace due to reduced interest costs, better efficiencies and sectoral traction. Good track record, robust financial performance, sectoral tailwinds and an experienced management team makes this IPO attractive.

- Key risks are 1) Project execution delays 2) Labor challenges 3) Intense competition.

- Opinion: Investors can SUBSCRIBE to this IPO with a 3 year perspective.

JainMatrix Knowledge Base:

See other useful reports on the right side panel and See Reports sections of the Menu.

- Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

- Check back on the website jainmatrix.com for updates.

Do you find this site useful?

- Visit the Investment Service page to find how you can get more. Or Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake, ownership or known financial interests in HGI or any group company. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.