- Industry – Railway Transportation PSU in PMC space

- Mid Cap of Rs. 4,000 crore

- IPO Opens 29th Mar – 03rd Apr 2019; Price range Rs. 17-19/share

- Valuations: P/E 6.9 times TTM; with a discount for Retail investors

- Advice: SUBSCRIBE for listing gains

![]()

Summary

- Transportation Infrastructure is a crying need in India. With Airlines, Roads and Ports sectors making good progress, the final frontier is the Indian Railways. The sleeping giant of IR appears to be getting up in the last few years.

- IPO Overview: RVNL is a Delhi based PSU into PMC of Railway projects like track laying, electrification, bridges etc. Its FY18 revenue, EBITDA and PAT were Rs. 7,822 cr., Rs. 614 cr. and Rs. 570 cr. resp. Revenue has grown at an impressive 33.7% and PAT at 19.2% over the last 3 years. Valuations are attractively low with a FY18 PE of 6.9x for the IPO. It has an asset light model. A good kicker should come from Q4FY19 results and listing gains in a positive market. Governance appears good and transparent within the PSU limitations.

- Key Risks: 1) Change in Central Govt. 2) De-emphasis on infra and railways by govt. 3) Issue of a contingent liability 4) Weak infra funding environment.

- Opinion: Investors can SUBSCRIBE to this IPO with a listing gains and a 2 year perspective.

Here is a note on RVNL IPO.

IPO highlights

- The IPO opens: 29th Mar-03rd Apr 2019 with the Price band: Rs. 17-19 per share. A discount of ₹0.50 per share on the offer price has been offered to retail and employee bidders.

- Shares offered to public number 25.34 crore of FV Rs. 10 and each market lot is 780 shares.

- The IPO will raise Rs. 482 cr. for 12% equity by current promoter i.e. Govt. of India with no dilution. The IPO share quotas for QIB, NIB and retail are in ratio of 50:15:35.

- The unofficial/ grey market premium for this IPO is Rs. 1-1.5/share. This is a positive.

Introduction

- RVNL – Rail Vikas Nigam Ltd – is a Delhi based PSU into PMC of Railway projects like track laying, electrification, bridges etc.

- Its FY18 revenue, EBITDA and PAT were Rs. 7,822 cr., Rs. 614 cr. and Rs. 570 cr. resp. Revenue has grown at an impressive 33.7% and PAT at 19.2% over the last 3 years.

- RVNL is a Miniratna (Category – I) firm incorporated by the Ministry of Railways (MoR) in 2003, as a project executing agency for MoR to undertake rail project development, mobilization of financial resources and implementation of rail projects for golden quadrilateral, port connectivity and project execution. RVNL mobilizes finances and forms project specific SPVs with private participation.

- The railway projects include new lines, doubling, gauge conversion, railway electrification, metro projects, workshops, major bridges, cable stayed bridges, institution buildings etc.

- Since 2003, RVNL has got 179 projects of which 174 are sanctioned for execution. Out of these, 72 have been fully completed for ₹20,567 cr. outlay and the balance are ongoing. They have an order book of ₹77,504 cr. as on Dec 2018 for 102 ongoing projects.

- During FY18, they completed 885 RKm (Route kilometre) of project length which included 315 RKm of track doubling and 425 RKm of rail electrification.

- RVNL earnings are from a management fee on the annual expenditure incurred for the execution of projects, of 9.25% for metro projects, 8.5% for other plan heads and 10% for national projects.

- Their activities under the various plan heads can be classified as under:

- New lines: is augmenting the rail network by laying new lines to achieving seamless multi-modal transportation network across the country and connecting remote areas.

- Doubling: Doubling involves the provision of additional lines by way of doubling the existing routes to enable the Indian Railways to ease out traffic constraints of single line or construction of 3rd/4th line to increase the capacity. RVNL is a significant contributor to the doubling projects and has been contributing to a third of the total doubling being completed / commissioned on Indian Railways for the last three years. (Source: CARE)

- Gauge conversion: includes conversion of meter gauge lines to broad gauge railway lines.

- Railway electrification: This includes electrification of current un-electrified rail network and electrification on the new rail network, generally from diesel run trains.

- Metro projects: This includes setting up of metro lines and suburban network in larger cities.

- Workshops: This includes mfg. facilities, and workshops for repairing and mfg. rolling stock.

- Others: This includes but is not limited to construction of traffic facilities, railway safety works (building of sub-ways in lieu of crossings), other electrification works, training works, surveys, construction of bridges including rail over bridges, etc.

- As a PMC (Project Management Consultant) firm, its services comprise of: (i) project development and execution of works related to creation of rail infrastructure; (ii) creating project-specific SPVs for encouraging private participation in the funding of railway projects; (iii) undertaking execution of railway projects under specific financial arrangement for the MoR and other Govt. departments; (iv) and other ancillary services like bankability studies for projects and preparation of detailed project reports.

- It has an asset light model where the contractor identified for project execution brings in all the people resources and machinery required.

- RVNL has a lean organization with only 541 employees of which 150 are regular and 391 are on deputation and may return to their home employer over time.

- Leadership in RVNL is Pradeep Gaur (53) is CMD, Ajay Kumar (56) is Director (Personnel), Vijay Anand (59) is Director (Projects) and Arun Kumar (59) is Director (Operations). They are all professionals with experience in Indian Railways and Metro corporations.

Financials and Segments

- We can see a solid growth of financials. FY19 so far does not look good, but we typically see H2 and Q4 as better than H1. See 4 year financials of RVNL in Fig 1.

- The emphasis in RVNL is on new lines, lines doubling and Metro projects. See business segments as reflected by the Order Book as on 31st Dec 2018 in Fig 2.

Fig 1- RVNL FY18 Financials

Fig 2 – RVNL Order Book Segments

Industry thoughts:

- Over the last few decades, the Indian Railways (IR) has not developed as fast as Roads, Ports and Airline sectors. It has struggled with its public service role as the dominant transporter of passengers. Most of the passenger services are priced at a discount and profits are from the goods services.

- However capacity constraints like tracks have forced IR to de-emphasize goods services.

- Productivity improvements have suffered in IR due to large and ageing workforce, legacy organization issues, weak governance in the past and slow decision making. Corruption has been an issue in IR in recruitment, private contracts and public services.

- Computerization has helped improve the Reservation system in IR. However there is still a long way to go in passenger capacity utilization, flexible pricing and ease of access.

- In recent times we have seen a dramatic improvement on many of these parameters in IR.

- In 2016, IR announced a capex plan of Rs 8,60,000 cr. over 5 years i.e. 2016-20. The capex plan is 90% more than the capital outlay in the previous 15 years.

- IR may be a critical element of India’s future growth story if it improves productivity, technology upgrades, goods transportation focus, financial sensitivity and improves services.

- RVNL is a key growth arm of IR and may have a good role to play in the transformation of IR in terms of capacity increase, new tech initiatives, metro projects, high speed train lines, etc.

- RVNL is also one of the second generation PSU firms that are lean in terms of employees, have a sharp business focus and outsource routine tasks to firms and have high productivity.

- MoR has under it group firms Indian Railways, Concor, RITES Ltd., IRCON, IRFC and RVNL.

- IR is the monopoly operator of rail based passenger and goods transportation services.

- Concor is a listed container focused transport firm running multi modal services.

- IRCON is a multi national consultancy firm active in transportation and infra, listed recently.

- RITES is a turnkey construction firm active in Rail and non-rail infra areas, listed recently.

- Indian Railway Finance Corporation (IRFC) is the dedicated financing arm of the Indian Railways for mobilizing funds from domestic as well as overseas Capital Markets.

- In this comparison it is clear that RVNL has a focus on India based Railways related work as a PMC consultant. There is little overlap with group firms.

Benchmarking

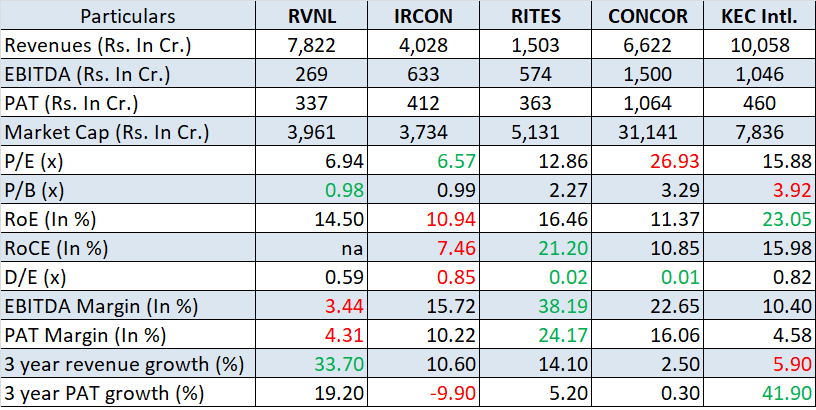

We benchmark RVNL against other comparable Indian Railway firms, and also KEC which is a private sector infra EPC firm. See Exhibit 3.

Exhibit 3 – Benchmarking

- The PE post IPO is low. This provides a safety net for IPO investors.

- Return ratios are good among the PSU pack.

- Debt is high but this is expected from an infra projects firm. Also it is a pass through debt, with IR making the payments as per schedule.

- 3 year growth of revenues and PAT is excellent.

Positives for RVNL and the IPO

- We have seen a flurry of new initiatives in IR and a slew of new projects and technology initiatives. The GoI is serious about change. So RVNL may see acceleration in business.

- Many private sector suppliers to IR have reported good growth in orders booked and revenues, across parts supply, and projects related to track laying and electrification. Many of these initiatives may be run by RVNL. Also it is notable that GoI is procuring from reputed private sector firms and taking their help to ramp up its operations.

- RVNL is a lean and productive firm, and with this listing, may be allowed to chart an Indian Railways independent part to growth and impact. Infra development is a high potential sector.

- It has attractive valuations with low PE and PB, moderate return ratios and a high 3 year revenue and PAT growth. The over 4%+ dividend yield is good.

- An order book of Rs. 77,500 cr. gives business visibility of 10 years.

- BV of Rs. 4,062 cr., and BVPS of Rs. 19.4/share is close to IPO price.

Risks and Negatives for RVNL and the IPO

- Typically infra projects have issues like land acquisition and govt. clearances which delay execution. This is true for railway projects too with suburban and metro projects.

- Funding of infra projects is underdeveloped in India. Long term funds from insurance and pension firms do not flow smoothly to infra, so projects become riskier with shorter term and more expensive funding. It is also exposed to financial variations like the current NBFC liquidity issue.

- On many parameters IR is weak when compared internationally, such as speed of trains, passenger services in trains and at stations, etc. Conversely many improvements are possible.

- The MoR and IR have been slow to grow in the Metro segment in India. As a specialized suburban train, the Metro is seen as an essential urban solution in Tier 1, 2 and 3 towns.

- As a MoR firm, with IR as the key group firm, RVNL may be constrained by their slow approvals and permissions. There are worries around political compulsions in MoR.

- Also RVNL has got projects by default from IR in the past due to relationship and structure. However in future and after RVNL listing, the flow of new projects is not assured.

- There is a contingent liability of Rs. 3774 cr. This is due to a demand from a contractor. However RVNL feels that the demand is not as per agreement, also if the charge is enforced, it will add to the project cost and be reimbursed by respective clients.

- H1 FY19 performance indicates no growth over FY18, however financials for PSU could be skewed towards H2 and Q4 which is usually the best quarter for infra/ GoI firms.

- Of the 10 IPOs made by PSUs in the last 2 years, only 2 have generated positive returns. Balance 8 are down 30% on average. IRCON is down 16% since listing.

- Political risk: With elections due in 1-2 months, we note that RVNL has accelerated performance in the current term of GoI. A change in leadership or party in power at MoR may affect future growth.

Overall Opinion and Recommendation

- Infrastructure is a crying need in India. With Airlines, Roads and Ports sectors making good progress, the final frontier is the Indian Railways. The sleeping giant of IR appears to be getting up in the last few years.

- RVNL represents the new initiatives, new technologies and expansion projects for IR. The current path is of acceleration, ambitious growth and standardization across India. The challenge is to get IR to grow in double digits, improve productivity, cover the country better and lower costs.

- Valuations are attractively low with a FY18 PE of 6.9x for the IPO. A good kicker should come from Q4FY19 results and listing gains in a positive market.

- Governance appears good and transparent within the PSU limitations.

- Key risks are 1) Change in Central Govt. 2) De-emphasis on infra and railways by govt. 3) Issue of contingent liability 4) Weak infra funding environment.

- Opinion: Investors can SUBSCRIBE to this IPO with a listing gains and 2 year perspective.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake, ownership or known financial interests in RVNL or any group company. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

Leave a comment