Good Growth but Expensive

- Date 01st Aug 2017

- IPO Open 31st Jul – 2nd Aug at Rs. 805-815

- Mid Cap: Rs. 6,000 cr. Mkt cap

- Industry – Security Services

- P/E: 66.5 times

- Advice: The IPO is rated as AVERAGE

Summary

- Overview: SIS is a provider of private security and facility management services in India and Australia. It is the largest company in security services in Australia and the #2 in security services and cash management in India. SIS’s revenues, EBITDA and PAT have grown at 14.5%, 13.7% and 12.4% CAGR from FY13 to FY17. They have a network of 251 branches in 124 cities and towns in India. Also they have an employee base of 154,432 employees across India and Australia.

- Key risk: Valuations look expensive in terms of P/E ratio at 66.5 times.

- Opinion: We rate the IPO as AVERAGE.

Here is our research report on Security and Intelligence Services Ltd. (SIS) IPO.

IPO highlights

- This IPO opens: 31st Jul – 2nd Aug 2017 with the Price band: Rs. 805 – 815 per share.

- SIS is a provider of security services, cash logistics services, electronic security and facility management services (FMS).

- The IPO issue size is Rs. 780 cr. at UMP. Shares offered to public number 0.95 cr. out of which 0.51 cr. are tendered under the OFS route. The FV of each is Rs. 10 and market Lot is 18. These shares are 13.07% of equity. The selling shareholders will receive Rs. 417 cr. at the UMP. See Exh. 1a.

- SIS benefits as the fresh issue of shares will generate Rs. 362.25 cr. to be utilized as in Exh. 1b:

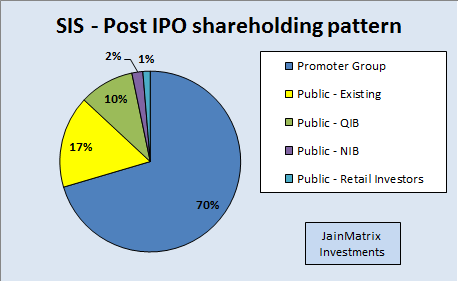

Exhibit 1a – Post IPO shareholding pattern

Exhibit 1b – Utilization of proceeds from fresh issue of shares

- The promoter and promoter group owns 76.9% in SIS which will fall to 70.4% (Post-IPO).

- The IPO share quotas for QIB, NIB and retail are in ratio of 75:15:10. Retail has low quotas.

- Theano (the investment vehicle of CX partners, which is a leading private equity group in the Indian mid-market) holds 15.19% stake in SIS (Pre-IPO). Theano is partially exiting through the IPO by tendering 32.6% of its current holding. The average cost of acquisition of equity shares for the Investor selling shareholders (Theano and AAJV) is Rs. 182.84/share. Ravindra Sinha (Chairman) and Rituraj Sinha (MD) have tendered 2.75% and 7.47% of their pre-IPO shares in the OFS.

Introduction to Security and Intelligence Services

- SIS is a provider of private security and facility management services in India and Australia. Started 32 years ago, it now has a #1 position in manned guarding in Australia and #2 in manned guarding and cash management in India. Revenues for FY17 were Rs. 4,577 cr. and profit Rs. 91 cr.

- They are a massive employer with an employee base of 154,432 personnel across India & Australia, of which 150,325 are billing employees. SIS categorizes employees as ‘billing’ who are deployed at customer premises and ‘non-billing’ who perform administration and support.

- SIS has a network of 251 branches in 124 cities and towns in India. Employees are not unionized, other than employees in their cash logistics business in Maharashtra; and some employees of a subsidiary. This is an advantage.

- In Australia, they provide paramedic and allied health, fire rescue services, mobile patrol, loss prevention and other related services. For Revenue segments, see Fig 2.

- SIS is the #2 cash logistics service provider in India. This includes transportation of bank notes and other valuables, doorstep banking and cash processing, ATM services include ATM replenishment, first line maintenance and safekeeping, and vault services for bullion and cash. The electronic security services include integrated and turnkey electronic security and surveillance solutions combining electronic security with trained manpower. They have recently entered into a JV in order to provide home alarm monitoring and response services. FMS in India include cleaning, janitorial services, disaster restoration and clean-up of damage, as well as facility operation and deployment of receptionists, lift operators, electricians and plumbers, and pest & termite control.

Fig 2 – SIS Segment Revenues FY17 / Fig 3 – SIS Revenue Geographies

- SIS has strategic relationships with several MNCs in India. For the cash logistics and alarm monitoring and response businesses, they have a JV with Prosegur, a global player. They also have a JV with Terminix, a MNC provider of termite and pest control services. SIS has licensed the ‘ServiceMaster Clean’ brand, and associated processes, operating materials and knowhow for their FMS in India from ServiceMaster group, a top service provider.

- Revenues grew faster in India at 33% compared to Australia – 5% CAGR over 5 years. See Fig 3.

- It has deep geographical reach for manpower sourcing & training; operates 18 training academies (India) and 4 in Australia. Security personnel undergo extensive 28 day residential program in various aspects of security. They also pay for this course so this is a revenue center.

- Leadership is Ravindra Sinha (Ch’man), Rituraj Sinha (MD), Uday Singh (CEO) and Arvind Prasad (CFO).

News, Updates and Strategies of SIS

- Promoter Background: Ravindra Sinha is the founder. He currently holds 41.57% stake. He is a member of Partiament. He started his career as a journalist, then became an investigative reporter and served as a war correspondent during the Indo-Pak war 1971. He has served as an advisor to the MoHRD. Per reports he declared personal assets of Rs. 850 cr. in 2014.

- In July’17 SIS, through a subsidiary SIS Australia, acquired an addl. 41% of the voting rights in SXP, formerly an associate, to now make it a subsidiary. In Aug’16, SIS acquired 78.7% of the equity of Dusters Total Solutions Services at a cost of Rs. 116.9 cr. Dusters is the 4th largest FMS provider in India, in terms of revenues, as of FY16.

- SIS’s revenue share from Australia has fallen from 74.5% in FY13 to 52.45% in FY17, due to faster revenue growth in the Indian market. The trend is likely to intensify.

- The strategy at SIS is to 1) Grow their businesses across customer segments including govt. and private sectors 2) Upgradation of technology to improve productivity. In Aug’16 they deployed ‘iOps’, a mobile security services operations platform; and deployed ‘SalesMaxx’ in Mar’17, a portable tablet sales kit, to enhance sales productivity and reduce time overheads 3) Leverage existing branches to achieve operational synergies 4) Inorganic growth through acquisitions 5) Australia business has good cash flows while the growth has been coming from the India businesses.

- The unofficial/ grey market premium for this IPO is in the range of Rs. 105-107. This is a positive.

Industry Reviews:

- In India: The security services market in India is witnessing high growth due to an improved economic environment, concerns about crime, terrorism, public safety measures and urbanization.

- The market for security services in India grew at 18.2% CAGR from FY10-15 to reach Rs. 39,000 cr. by FY15. It may grow at the rate of 20% between FY15-20 to reach Rs. 97,000 cr. by 2021.

- The industry works on a credit period of 60-90 days from completion of services. Many smaller operators pay wages only when they receive payments from customers while larger players pay wages on a monthly basis. In addition, security services is a low margin, high volume business. This makes the security services industry a working capital intensive business. This operating model is not expected to undergo much change in the next few years.

- The industry faces high attrition (57% for SIS), but that does not mean the guards are exiting the industry. When a large contract is lost or expired, the guards already employed in that location may be absorbed on the payrolls of the firm that wins or takes over the contract. This is a common business practice in the Indian security services market.

- The security services market is fragmented but has good growth. National operators currently have 20% share and regional /local operators have 80%. However, with the rollout of GST and stricter enforcement of PSARA (Private Security Agency Regulation Act 2005), the share of national operators is going to improve and local operators may get hit by cost of compliance. By FY20, national and regional operators are likely to have 90% of the market in India.

- The demand drivers of the Indian security services are 1) Increasing economic activity and GDP growth leading to need for improved security 2) Growth in Wages 3) Increased threat from anti-social elements and terrorist outfits 4) Societal perception on threats and awareness on security.

- Facility Management Industry in India: FMS refers to the outsourcing of services and functions which are considered non-core activities. The total FMS market has grown at a CAGR of 16% from FY10-15. The total FMS market in India is estimated to grow with a CAGR of 20.3% between FY16-20.

- Demand for FMS is consistently growing with increasing awareness among end-users. End-users include offices, hotels, hospitals, malls, residential spaces, the auto industry, the pharma industry, electronics, food and infra development, mostly the commercial sector.

Financials of SIS

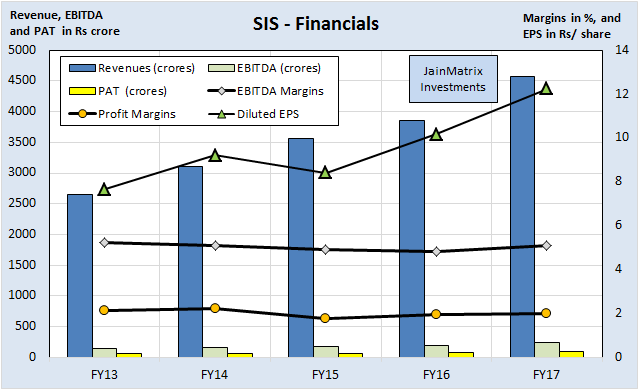

Fig 4 – SIS Financials

- SIS’s Revenue, EBITDA and PAT grew at 14.5%, 13.7% and 12.4% CAGR from FY13-17, see Fig 4.

- The EPS grew moderately in the last 5 years. There was a fall in FY15 as the bonus was increased from Rs. 10,000 to Rs. 21,000 with retrospective effect from Apr 1, 2014 per a Dec 2015 amendment in Payment of Bonus Act. As a result SIS incurred additional expenses of Rs. 8.75 cr. in FY15. Also a change in depreciation calculations as per new regulations impacted the bottom-line for FY15.

- SIS has an ROE of 16.8% and a RoCE of 22.4% for FY17 which is good. The return ratios are high. Dividend declared grew at a CAGR of 30.7% from FY13-16. But in FY17 there was no dividend. SIS has low and flat margins over the years which is due to the nature of the business and industry. Thus high sales growth is essential for attractive PAT growth.

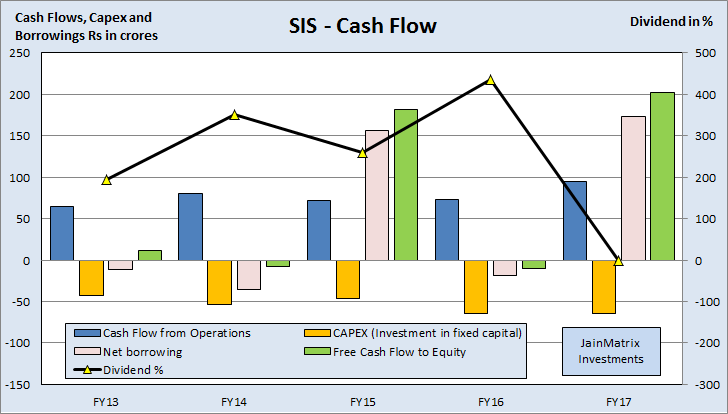

- SIS had negative FCFE in only 1 out of the last 5 financial years, see Fig 5.

- The attrition rate of employees in the security services business in India for FY15, FY16 and FY17 was 65.7, 57.7% and 55.7% resp. The attrition rate of employees in Australia, for FY15, FY16 and FY17 was 24.2%, 21.4% and 20.6%, resp. The industry faces high attrition.

- But borrowings have been high recently on account of acquisitions. The current D/E ratio is 1.37 (FY17). This may improve after Rs. 200 cr. debt is paid off post IPO from a total debt Rs. 762.5 cr.

Fig 5 – SIS Cash Flow

Benchmarking

We benchmark SIS against Quess Corp and TeamLease Services. The business segments for these firms are different as compared to SIS. Majority of Quess revenues are derived from recruitment (RPO), general staffing, training and skill development etc. whereas TeamLease is into multiple HR services ranging from temp staffing (general & IT), permanent recruitment, payroll processing etc. However they are close comparables. We also view but not rate Redington and NIIT. See Exhibit 6.

Exhibit 6 – Benchmarking

- PE for SIS is moderate at 66.52 times as compared to its peers. Quess Corp enjoys PE valuations at 117 times largely due to high expectations from investors due to high recent sales and PAT growth.

- The valuation is moderate in terms of P/B ratio (adjusted post IPO at 6.67 times).

- SIS has witnessed poor sales growth compared to its peers in the last few years. The 3 year sales growth below 13.8% and the 3 year PAT growth at 9.9% is moderate. However the India business has grown much faster than the Australia business and is now over 50% of revenues.

- The D/E ratio at 1.37 is highest but is expected to improve post IPO.

- The margins are moderate. The return ratios are good with RoE at 16.8% and RoCE at 22.44%.

- The dividend yield is the highest, however the yield is low on a standalone basis.

- Note: The dividend yield has been calculated basis FY16 and the UMP of the IPO at Rs. 815/share.

Positives for SIS and the IPO

- Leader: SIS is #1 in security services in India & Australia, and #2 cash logistics provider in India.

- SIS has a diverse customer base, so is de-risked from economic cycles and customers dependence.

- SIS has a scalable business model. Also security services are becoming essential over the years and this makes the business shock-proof to any kind of demand fluctuations.

- New initiatives like GST are positive for organized players like SIS.

Risks and Negatives for SIS and the IPO

- The valuations look expensive in terms of P/E ratio. SIS has the high D/E, low margins and low growth rates for the asking PE ratio which stands at 66.5 times FY17 which is expensive.

- Rising labour costs are worrisome for SIS and will impact profitability.

- SIS has a large workforce deployed across workplaces and customer premises, in high risk/ crime affected roles. They may be exposed to service claims and losses or employee disruptions that could have an adverse effect on the business.

- SIS is exposed to 18 criminal proceedings and 27 taxation related matters currently. Any adverse outcome in any of these proceedings may negatively affect the business.

- SIS’s businesses involve carrying and handling of firearms by employees. Any misuse or contravention of laws or policies relating to firearms by personnel may affect their reputation.

Overall Opinion and Recommendation

- Employment generation is a challenge in today’s environment. SIS with its large workforce and structure is well placed to create jobs and build strong brands around services of security, cash management and FMS.

- With deep relationships in govt. and private sectors, and a good niche, SIS may continue to get good growth in the Indian market.

- The Indian securities business of SIS grew 33% YoY in FY17 and grew 50% faster than the industry. The management is focused on the Indian market for the years to come.

- The valuations are expensive at a P/E of 66.5 times of FY17 earnings, so we rate the IPO as AVERAGE.

JAINMATRIX KNOWLEDGE BASE

See other useful reports:

- IRB Infra Developers – In INVIT We Trust – 25 JULY

- Stock Market Awareness Presentation by JainMatrix – July

- Equity Investment Made Easy by JainMatrix – Updates July 2017

- A Rural focused Stock Pick – premium – 08 July

- Eris Life IPO – and Pre listing note – premium – 28 June

- AU Small Finance Bank IPO – 26 June

- The JainMatrix Investments Outlook – 22 June

- MSC Portfolio Review – 10.8% CAGR Alpha – premium – 21 June

- JainMatrix – Track Record – 31 May

- IndiGo Airways – Flying High, Wide and Handsome – 30 May

- Eicher Motors – It’s Firing on Both Engines – 16 May

- Hudco IPO – Sector Uncertainties, AVOID – 09 May

- S Chand IPO: An Educational Content Powerhouse – 27 Apr

- Vikas Ecotech – Get ‘Vikas’ for your Investments – 24 Apr

- Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

- Check back on the website jainmatrix.com for updates.

DO YOU FIND THIS SITE USEFUL?

- Visit the Investment Service page to find how you can get more. Or Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Punit Jain intends to apply for this IPO in the Retail category. Other than this, JM has no known financial interests in SIS or any group company. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.