- 22nd Feb 2017

- CMP: Rs 1,510

- Large Cap – Mkt Cap 33,700 crores

- Issue Period: 23rd Feb 2017, one day only

- OFS Floor Pricing: Rs 1,498/share. Retail gets a 5% discount

- Advice: Investors can BUY with a 2 year perspective

Summary

- Overview: BEL is a PSU Navaratna engaged in design, mfg. and supply of electronics products/systems for the defense requirements, as well as for non-defense markets.

- The EPS growth has been excellent recently and the price has risen faster than EPS growth leading to re-rating of the PE ratio/valuation of the company. The current government has a big thrust on defense which is evident from the quantum of fresh orders acquired for FY16.

- Investors have got a 5 year CAGR return of 25.7% and 12.1% CAGR in the last 2 years.

- BEL has conservatively preserved cash and is poised to grow financially as the Indian defence sector starts to grow domestically.

- Overall Opinion: We feel BEL is a value BUY for investors in this OFS.

OFS Offer details

- CMP is Rs 1,510. The OFS floor price is Rs 1,498; there is a 5% discount for Retail investors. 20% of the OFS offer is reserved for Retail. At floor price this is Rs 1,423.

- Cut off is the lowest price at which OFS shares will be sold, and will be equal or above the floor price. Cut off depend on the bids. Applicants may apply for OFS at floor price, or above, or at Cut Off.

- OFS Application date is only one day – Feb 23rd, 2017 between 9.15 am to 3.30 pm.

- The GoI will sell 1.11 cr. equity shares (5.0%) of stake in BEL through the OFS route. The govt. is selling this to meet its FY17 divestment targets. The shareholding is currently 74.4% which will come down to 69.4% after the OFS. It could fetch GoI about Rs 1,672 cr., based on the pricing declared.

- P/E as on 21st Feb, 2017 closing price is 21.8 times, which appears high.

Here is a note on the Bharat Electronics Ltd (BEL) Offer for Sale (OFS).

Introduction

- BEL is a Bangalore based PSU engaged in design, mfg and supply of electronics products/systems for mostly defense, and some non-defense applications.

- It has been accorded Navratna status by the GoI. BEL owns 9 factories.

- Turnover and profits were Rs 7,459 cr. and Rs 1,357 cr. in FY16. BEL has 9,848 employees (FY16) and a market Cap of Rs. 33,734 cr. Exports make up 7% of turnover.

- Shareholding in % is – GoI 74.4, DIIs 15.8, QFIs 4.3, Individuals 2.8, Others 2.74%.

- Its key products are weapon systems, radar and fire control systems, and communication. Its defense products include defence communication; radars; naval systems; computers, intelligence systems; weapon systems; telecom and broadcast systems; electronic warfare; electro optics, and solar photovoltaic systems. Its nondefense products include turnkey system solutions; civilian radars; e-governance systems, and homeland security. It also offers electronic mfg. services in areas of PCB assembly and testing; precision machining and fabrication; opto electronics components and assemblies, and offsets, among others.

Stock Evaluation, Performance and Returns

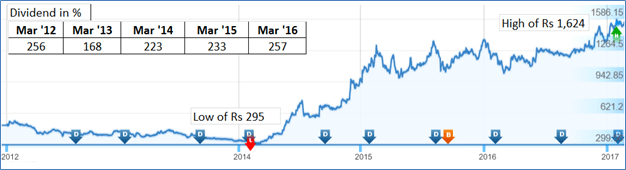

Fig 1 – Price History

- Revenues, EBITDA and Profits have grown at 7.1%, 6.2% and 7.7% over 7 years.

- There’s been a recent acceleration – the EPS TTM has grown from Rs 28.3/share in Dec 2012 to Rs 69.4/share in Dec 2016, a 25.2% CAGR growth in EPS in 4 years.

- The share price, grew at 25.7% CAGR over 5 years, see Fig 1 – Price History.

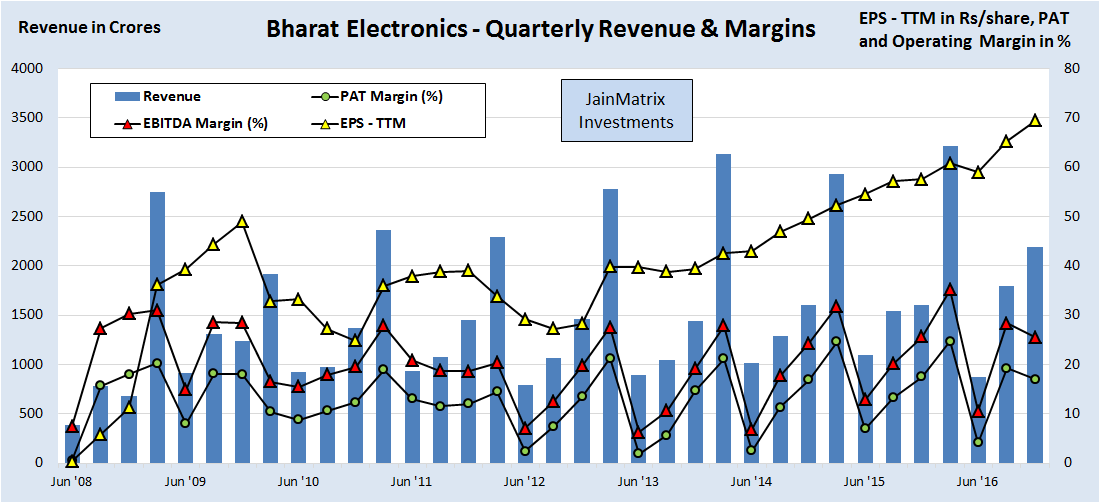

- The margins are good. The EBITDA and PAT margin for FY16 stood at 35.2% and 24.7%, see Fig 2.

Fig 2 – Quarterly Financial

- We can see that the Q4 – March quarter is the largest by far due to Govt. customers.

- ROCE and RONW are currently at 20.2% and 16.2% resp. Both these ratios have been high and fairly stable over the last 5 years.

- The dividend at 257% on a FV of Rs 10, provides a dividend yield of 1.13%. This is good.

- Cash from operations and Free Cash Flow are positive for 7 of the last 9 years. This is a positive. Fig 3.

- As a result BEL has good cash reserves and zero debt. The cash on hand is Rs.7,553 cr (FY16), which is Rs 315 per share. In theory, the operations of BEL are available today for Rs 1510-315= Rs 1,195.

- This cash on the balance sheet may be used for expansions, M&A or dividends.

Fig 3 – Cash Flow and Dividend

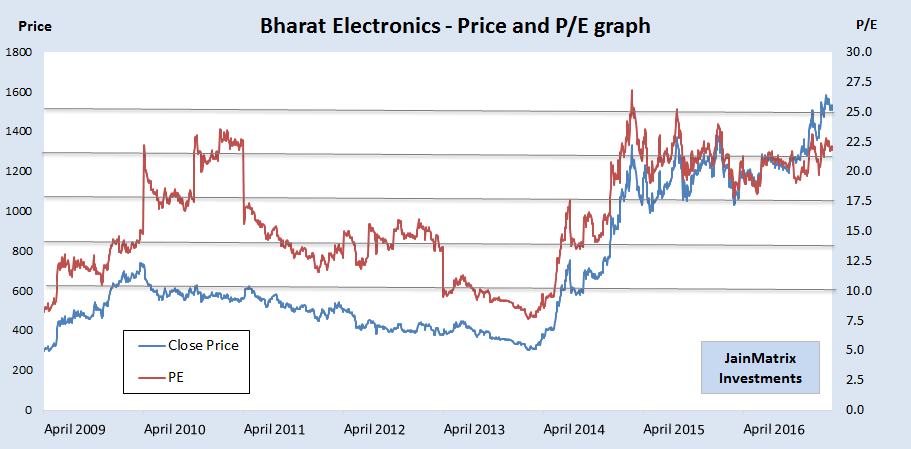

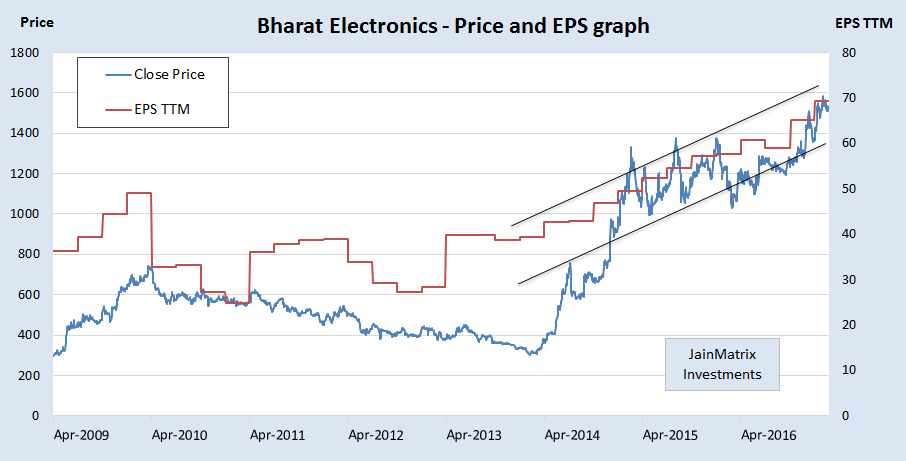

Fig 4 – Price and PE Chart/ Fig 5 – Price and EPS Chart

- The Price and P/E chart is Fig 4. The 8 year historical average PE is 17.5 times and range is 10 to 25 times in 4 quadrants. Current P/E at 21.75 times is in the high or overpriced quadrant per the chart.

- The Price and EPS chart Fig 5 shows a strong rise in EPS from 2014-16. However the BEL share price rose faster, so the PE too has risen in the last 4 years.

- We conclude that the BEL stock has got re-rated and the historical average has moved to a higher level in the last 2.5 years.

Fig 6 – Booked to Bill ratio / Fig 7 – New Orders

- A key ratio is Total Orders Booked to Revenues Billed, Fig 6. This is linked to annual new orders, Fig 7. The last 4 years view shows that the ratio is improving.

- It is because of GoI thrust on defense combines with the Make in India program where they are trying to develop domestic capabilities in both private and public sectors. This is evident from the quantum of fresh orders acquired for FY16.

Benchmarking

Exhibit 8 – Financial Benchmarking (click image to enlarge)

In the benchmarking exercise we compare BEL with some peers. See Exhibit 8.

- It’s difficult to find comparable firms to BEL due to its unique defence sector, electronics products, emerging industry and PSU status.

- The PE ratio appears moderate, however the P/B ratio appears to be high.

- It has a good position in terms of margins and dividend yield and return ratios.

- The double digit return ratios are good and stable over the years. This is a positive considering the nature of the business of BEL.

Overall Opinion

- India has the third largest armed defense force in the world. India’s requirements on defense are currently catered largely by imports. The GoI policy is now promoting self-reliance, indigenisation, technology upgradation, achieving economies of scale and development of capabilities in defense.

- BEL occupies an important space as it has a momentum of capabilities in electronics and is being entrusted with many new initiatives. Its growth has picked up massively in the recent years.

- We feel that opening up of the defence sector to the private players is the way to go in the long run. However the growth of private domestic defense firms may take time to translate to reality. Until then, PSU defense firms will dominate. They will also help in the transition to private sector.

- BEL like most PSUs has conservatively preserved cash and is poised to grow fast.

- We feel BEL is a value BUY for a 2 year holding period in this OFS and at current levels from markets.

Download the PDF to see entire note.

JainMatrix Investments_BEL_Feb2017

DO YOU FIND THIS SITE USEFUL

- Visit the Investment Service offering page to find how you can get more.

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

DISCLAIMERS

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Punit Jain discloses that he has no current holding in BEL, but he may apply in the OFS in the retail category. Other than this, JM has no known financial interests in BEL or any related firm. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any equity investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Punit Jain is a registered Research Analyst and compliant with SEBI (Research Analysts) Regulations, 2014. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com