Dear Readers,

The IPO season is hot now, hotter than the summer outside. In this note we recap recent events and try to look ahead too:

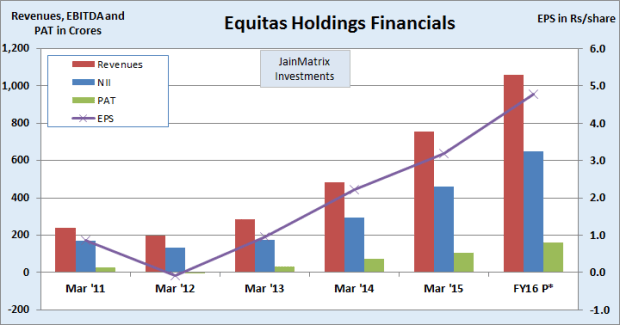

EQUITAS HOLDINGS IPO

- Our investment report was Equitas IPO – A Leader in Small Finance Banks

- It is available on link Equitas Holdings IPO Note

- JainMatrix Investments had recommended a BUY

- The IPO was open from 5-7thApr 2016 and Issue Price band was 109-110 per share

- There was a healthy subscription for the offer:

- The issue price was Rs 110 and the shares got listed on April 21, 2016.

- As of today the share price is trading at Rs 147.80 and is up by 34.5%.

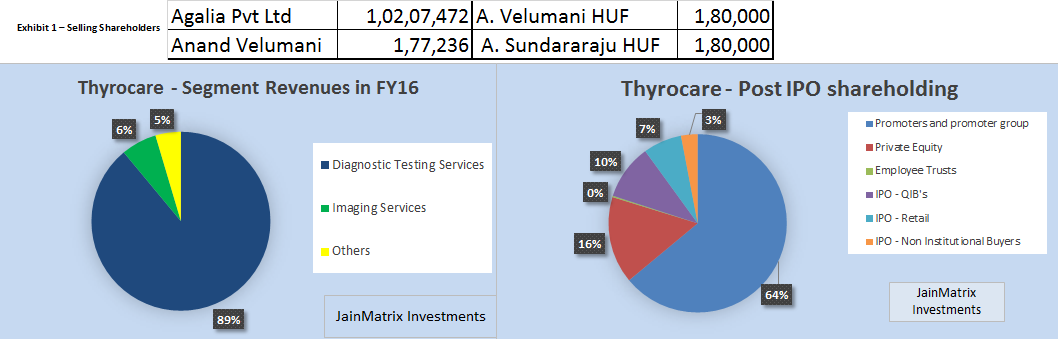

THYROCARE IPO

- Our report was Thyrocare IPO – Wellness for your Wealth

- The link is Thyrocare Technologies IPO Note

- JainMatrix Investments had recommended a BUY on Thyrocare.

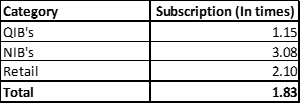

- IPO was open from 27-29thApr 2016, and the Issue Price band was 420-446 per share.

- There was a tremendous demand for the IPO and the category wise subscription was:

- The issue price was Rs 446 and the shares got listed on May 9, 2016.

- As of today the share price is trading at Rs 625.5 and is up by 40.3% in absolute terms.

PARAG MILK FOODS IPO

- Our report was Parag Milk Foods IPO – Let This Drink Go

- The link is Parag Milk Foods IPO Note

- JainMatrix Investments had recommended an Avoid on this offer.

- IPO was open from 4-6th May 2016 and the Issue Price band was Rs. 220-227 per share. There was a retail Discount of Rs 12 /share.

- Response was not good, so the company had to cut the issue price and extend the closing by three days as it could not garner the full QIB participation.

- It finally closed on 11th The category wise subscription was as follows:

- As per the grey market rumors, Parag Milk Foods is likely to list at a discount.

- Let’s see how this listing turns out.

We’re happy to note that we are able to predict even complex IPO offerings with some success using our fundamental research techniques.

Sign up with us to get solid professional support through your multi year investing cycle.

Annual subscription for the Investment Service is available for Rs 11,999/- (India located) or US$ 210 (located outside India), for individual / Retail investors.

Investment firms, wealth professionals and Institutions may contact us for a quote for Investment Services.

MAKE PAYMENT NOW

Happy investing,

Punit Jain

JAINMATRIX KNOWLEDGE BASE

See other useful reports

- JainMatrix Track Record May 3rd, 2016

- Thyrocare IPO – Wellness for your Wealth

- New Banks: Big Changes in Small Change

- Equitas IPO – Leader in SF Banks

- JainMatrix Investments Announcements

- A Superior Investing Process – Do a DIP SIP

- JainMatrix Investments presents the Investment Outlook for 2016

- Alkem Labs IPO

- Goods And Services Tax (GST): Integration And Efficiency

- Café Coffee Day IPO – Very Hot Coffee

- Syngene IPO: Good Pharma R&D spinoff from Biocon.

- JainMatrix IPO Reports deliver 60.5% returns

Search for companies/ sectors of your interest in Search box in the right panel.

Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

DO YOU FIND THIS SITE USEFUL?

Visit the Investment Service page to find how you can get more. Or Click LINK

Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

DISCLAIMER

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no known financial interests in Parag Milk Foods/ Thyrocare/ Equitas Holdings or any related group. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst (SEBI Registration No. INH200002747) under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.