- Date 24th Oct

- IPO Opens 25-27th Oct with Application Price range is Rs. 247-252

- Valuations: P/E 38.2 times TTM, P/B 6.1 times (Post IPO)

- Mid Cap: Rs. 15,400 cr. Mkt cap and Industry – Asset Management

- Advice: SUBSCRIBE

![]()

- Overview: RNAMC is one of the largest asset management companies in India, managing total AUM of Rs. 3,62,000 crores. They offer products like mutual funds, portfolio management services, alternative investment funds, pension funds; and offshore funds and advisory mandates.

- Revenues and profit for FY17 were Rs. 1,436 cr. and Rs. 403 cr. RNAMC’s revenues, EBITDA and PAT grew at 18.2%, 18.7% and 14.9% CAGR in 5 years.

- The Indian mutual fund industry is expected to grow at a CAGR of 20% between FY18 and FY22, due to buoyant capital markets, and a shift from physical to financial assets.

- At a P/E of 38.2 times, the valuations of the IPO appear high. But good track record, robust financial performance, sectoral tailwinds and a good management team makes this IPO attractive.

- Risks: Promoter related image, senior level exits and regulatory uncertainties are the key risks.

- Opinion: Investors can SUBSCRIBE to this IPO with a 2 year perspective.

Here is a note on Reliance Nippon Asset Management Company (RNAMC) IPO.

IPO highlights

- The IPO opens: 25-27th Oct 2017 with the Price band: Rs. 247-252 per share.

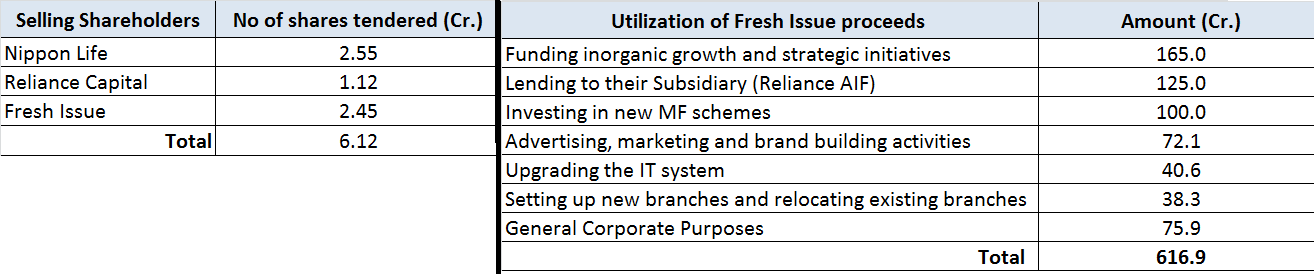

- Shares offered to public number 6.12 crore. The FV of each is Rs. 10 and market Lot is 59.

- The IPO will raise Rs. 1,542 cr. while selling 10% of equity. The offer includes a fresh issue of shares of Rs. 617 cr. and an OFS of Rs. 925 cr. (UMP).

- The selling shareholders are Nippon Life (selling 4.10%) and Reliance Capital (8.85%) of the current holding. Post IPO both promoters will hold 42.8% in RNAMC.

- The net proceeds from fresh issue of shares will be utilized as follows:

Exhibit 1(a) – Selling IPO Shareholders and Exhibit 1(b) – Utilization of Proceeds

- The Promoter group (Reliance Capital and Nippon Life Insurance) owns 95.5% in RNAMC which will fall to 85.7% post-IPO.

- Reliance Capital is an NBFC that is engaged in corporate lending and investment activities. It is an Anil Ambani – Reliance group firm. Nippon Life Insurance Company underwrites and sells life insurance and is the largest Japanese life insurance company by revenue.

- The IPO share quotas for QIB, NIB and retail are in ratio of 50:15:35.

- The unofficial/ grey market premium for this IPO is Rs. 65-70/share. This is a positive.

Introduction

- RNAMC is one of the largest AMC companies in India, managing total Assets Under Management (AUM) of Rs. 3,62,550 cr. as of June 2017. They are involved in managing (i) mutual funds (MFs including ETFs); (ii) managed accounts, including portfolio management services (PMS), alternative investment funds (“AIFs”) and pension funds; and (iii) offshore funds and advisory mandates.

- RNAMC was ranked the 3rd largest AMC, in terms of MF quarterly average AUM with a market share of 11.4%, as of June 2017. For FY16, they were the 2nd most profitable AMC in India.

- Revenues and profit for FY17 were Rs. 1,436 cr. and Rs. 403 cr. It has 971 employees out of which 563 are in sales & distribution and 179 are in operations and customer service.

- RNAMC manages 55 open-ended MF schemes including 16 ETFs, and 174 closed ended schemes under Reliance MF as of June 2017. The pan-India network is of 171 branches and 58,000 distributors like banks, financial institutions, DSAs and independent financial advisors (IFA).

- 59% of the AUM is in MFs, 40% are managed accounts and 1% is offshore funds.

- In managed accounts business, they provide PMS to HNIs and institutional investors including the Employees Provident Fund Organization (EPFO) and Coal Mines Provident Fund Organization (CMPFO).

- A subsidiary, Reliance AIF manages 2 Alternative Investment Funds registered with SEBI. RNAMC manages offshore funds through its subsidiaries in Singapore and Mauritius and have an office in Dubai, which caters to investors across Asia, Middle East, UK, US, and Europe. They also advise on India focused equity and fixed income funds in Japan and South Korea. See Fig 2.

Exhibit 2(a) – AUM by product offering and 2(b) Managed Accounts segments

Fig 2 (c) – RNAMC AUM trend from FY13-17

- Within the MFs 64% of the AUM is debt, 30% is equity and 6% are gold & ETFs. Within managed accounts 84% of the AUM is EPFO, 14% CMPFO and 2% PMS & AIF AUM.

- Their monthly inflow from Systematic Investment Plan (SIP) into MFs increased to Rs. 509 cr. in June 2017 from Rs. 274 cr. in April 2015. The number of SIP accounts stood at 18.6 lakh accounts, an addition of 5.6 lakh. The average ticket size of SIPs rose to Rs. 3,915 in June 2017 from Rs. 2,822.

- Leadership is Vijayendra Kaul (NonExec Chairman), Sandeep Sikka CEO and Prateek Jain CFO.

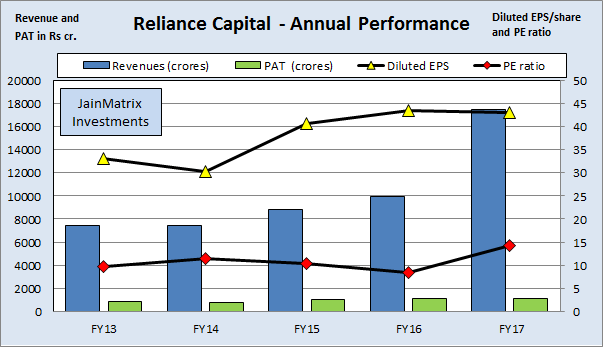

Promoter – Reliance Capital – Snapshot and Financials

- Reliance Cap is an NBFC engaged in corporate lending and investments; AMC services through RNAMC; General and Life Insurance, Commercial Finance and other fin. services.

- Income and PAT has grown at 23.7% and 7.5% CAGR resp. over 5 years.

Fig 3 – Reliance Cap Financials

- Reliance Capital’s share price gained 11.2% CAGR over the last 5 years and CMP is Rs 566.2.

- The life insurance segment of Reliance Capital is weak, however consolidation is over. The general insurance and commercial finance business have witnessed strong performance in Q4 FY17. The AMC arm is the strongest amongst other business segments and the outlook for the same is bullish. It is expected to post better profits in FY18.

- Reliance Capital has a market cap of Rs 14,500 crores.

News, Updates and Strategies of RNAMC

- RNAMC’s business strategy is as follows:

- To expand investor base and focus on retail. According to ICRA, in India, the retail investors MA-AUM grew by 163% from Mar 2014 to Jun 2017 from 1,63,000 cr. to 4,28,000 cr.

- To focus on developing their AIF business.

- To grow inorganically through strategic acquisitions. In Nov 2016, in order to strengthen their ETF offerings, they acquired the AMC business of 12 schemes by the Goldman Sachs MF. RNAMC intends to leverage the experience gained through the previous acquisition.

- The average cost of acquisition of equity shares for selling shareholders is as follows:

Exhibit 4 – Acquisition Costs

- According to merchant bankers, RNAMC is expected to see demand worth more than Rs. 15,000 cr. for the shares on offer for anchor investors. The portion allocated for anchor investors is worth Rs 462 cr. The anchor book subscription will be open on 24 Oct.

- They bought the CPSE ETF funds from Goldman Sachs in 2015, boosting govt. business and AUM.

- The day 1 IPO performance is that it got subscribed 4.63 times by 5 pm, so IPO success is assured.

MF Industry Outlook in India

- The economy has seen big financial events like demonetization, RERA, GST and a crackdown on black money and shell companies. All these have rekindled interest in financial assets as compared to real estate and gold which were popular earlier.

- The regulations and disclosures around MFs have ensured that traceability and audit trails are quite clear in this industry. At the same time, SEBI has done a remarkable job of promoting the MFs as good entry level equity and debt products, so AUM growth has been good.

- As of June 2017, there are 41 active AMCs in the market comprising 7 sponsored by PSBs, 2 by financial institutions, 25 by the private sector and other financial companies and 7 by foreign players (including JV’s).

- The Indian MF industry is concentrated with the 10 large firms having 80% of the industry AUM. ICICI Prudential AMC, HDFC, Reliance, Birla Sun Life and SBI Funds are the 5 largest.

- The MF industry witnessed a healthy growth in the past decade, with the AUM growing from Rs. 3,50,000 cr. (FY07), to Rs. 19,50,000 cr. (June 2017) growing at a CAGR of 18% over 10 years.

- The growth in AUM has been supported by a favorable macro environment, the rise of capital markets, foreign fund inflows and growing investor awareness. During FY17, the fresh investments (or new sales) in MFs grew by 28% to Rs. 1,76,000 cr. in the FY 2017.

- The Indian MF industry is expected to grow at a CAGR of 20% between FY18-22, with the AUM expected to grow to Rs. 45,00,000 cr. by Mar 2022. Growth rates are expected to be higher in FY18 and FY19 due to buoyant capital markets coupled with an increase in retail participation, after which the growth rate is expected to taper given the increase in scale. (Source RHP)

- The stock broking firms too perform very well when markets are in a bullish phase.

Financials of RNAMC

- RNAMC’s revenues, EBITDA and PAT grew at 18.2%, 18.7% and 14.9% CAGR in 5 years, Fig 5.

- RNAMC had a RoE of 21% in FY17 while the RoCE stands at 30.5%. The return ratios are high.

- RNAMC declared a high dividend in FY17 as compared to FY16 in spite of weak financials. The PAT growth was 1.6% in FY17, but the dividend growth was 72%. Declaring high dividends right before the IPO in a year with poor financial growth is a negative.

- RNAMC has been Free Cash Flow positive in 4 of the last 5 years. This is a positive.

- The margins fell in FY17 impacting profitability, on account of a rise in administrative expenses, higher depreciation and expenses growth for that year.

- RNAMC allotted equity shares to existing shareholders in a bonus issue on 11 Aug, 2017. It declared a bonus ratio of 50:1, and post the issue of bonus, the no. of shares stood at 58.75 cr. and post IPO it would jump to 61.20 cr. shares.

- This means the asking FY17 P/E is 36.8 (pre-IPO) and 38.3 (diluted post-IPO).

Fig 5 – RNAMC Financials / Fig 6 – RNAMC Cash Flow (below)

Positives for RNAMC and the IPO

- Reliance Mutual Fund is a top brand of 22 years vintage. RNAMC has a strong presence across India with subsidiaries in Singapore and Mauritius.

- As a first AMC firm in India to list, there will be a scarcity premium to this IPO offering.

- RNAMC has a strong focus on processes. They regularly monitor their current processes which have contributed significantly to their growth. RNAMC is certified on the International Quality Standard, ISO 9001:2008 and have implemented a robust Quality Management system. They have instituted well-documented operational processes, extensive trading systems and technology platforms.

- RNAMC has a large and experienced management and investment team comprising of 44 professionals that manage their funds and provide advisory services. The senior investment team has an average 19 years of experience and are the key resources of to RNAMC.

- In terms of financial performance, RNAMC has so far performed well. The margins and return ratios are high. The growth is above average and debt is low. Also RNAMC is in an industry likely to perform well over the next few years. These factors make investment in RNAMC attractive.

- There is a bubble in IPOs with massive over subscription and unreasonable valuations in the recent past. We feel this is on account of high inflow of investment funds, and poor choices of expensive primary markets over more reasonable secondary markets. This may help this IPO offering.

Risks and Negatives for RNAMC and the IPO

- The valuations are high side in terms of P/E at 38.3 and P/B at 6.15 times (adjusted post IPO).

- In the past RNAMC’s reputation was built up with high profile star investors like Madhu Kela and Sunil Singhania. However, both have left RNAMC in the last 6 months. Madhu is a part time adviser to Reliance Capital and Sunil is now global head of Reliance Cap’s equity business. In fact in last 12 months, 3 top executives left. RNAMC may struggle to maintain business momentum in future.

- Reliance Capital, the promoter of the RNAMC is part of the Anil Ambani Group. Other group companies are Reliance Power, Reliance Comm., Rel. Infra, Rel. Defense and Rel. Big Cinema. Many of these firms are not doing well financially and for shareholders. Reliance Power IPO in 2008 is still fresh in our minds. Reliance Comm. looks likely to shut down soon. Having said this, RNAMC is in the AMC business and has a fair reputation over the years.

- AMCs are closely regulated by SEBI. The investment product industry in India has benefitted from the regulations, however it is also subject to changes or tightening of norms. For example in July 2014, the holding period for long-term capital gains tax on debt MFs was increased from 12 to 36 months. Thus regulatory changes can affect business in future.

- SEBI has on 6 Oct 2017, issued a circular to categorize and rationalize the MF schemes so as to enable the investors to better evaluate the different options available and take informed investment decisions. Accordingly, the schemes are classified into 5 groups, i.e., equity schemes, debt, hybrid, solution oriented schemes and other schemes. These 5 groups collectively have 36 different categories of schemes under them. The circular states that, only 1 scheme per category is permitted to continue to exist/ be launched by a MF, with few exceptions. Since RNAMC runs 55 open-ended and 174 closed ended MF schemes, there may be a big consolidation required soon.

- Competition from existing and new market participants offering investment products could reduce their market share or put downward pressure on their fees.

Overall Opinion and Recommendation

- The MF industry is witnessing an unprecedented growth with AUM increasing 6 fold in 10 years. The number of new investors and their folios have grown by 66 lakh in the first 6 months of this year on account of strong participation from retail investors. The PMS sector is also doing well; and post Pension reforms, this sector is also coming under professional AMC purview.

- Further Gold and real estate are a large proportion of Indian savings which have not generated significant returns. India is witnessing falling interest rates and thus FD and savings rates have fallen sharply and other metals as a store of wealth have proven to be costly. There is thus a trend of shift from physical assets to financial and risk assets in the Indian economy.

- Reliance Nippon AMC is an established #3 market share player with a good 22 years of history.

- At a P/E of 38.2 times, the valuations of the IPO appear to be high.

- But a good track record, robust financial performance, sectoral tailwinds and a good management team makes this IPO attractive.

- Promoter related image, senior level exits and regulatory uncertainties pose the key risks.

- Opinion: Investors can SUBSCRIBE to this IPO with a 2 year perspective.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no stake ownership or known financial interests in RNAMC or any group company. Punit Jain may apply for this IPO in the Retail category. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.