————————————————————————————————————————–

- Date: May 7th, 2014

- Large Cap with Market Cap Rs 10,920 crores

- CMP: Rs 146

- Advice: Buy

JainMatrix Investments has published a report on Petronet LNG for its Subscribers. A partial report is available below. Removed sections include Bench-marking, Financial Projections, Risk factors, and 2 year target prices for the share. The JainMatrix Investment service is available for a subscription fee.

This is an update of the June 2012 report called Petronet LNG – A Solid Gas Company LINK

Executive Summary

Overview: Petronet LNG dominates the import of Natural Gas in India, and has a unique private sector status. It has a great record of creation and operation of LNG import facilities. Revenues have grown at a CAGR of 34%, EBITDA 9%, Profits 7% & Cash Flow 23% over 6 years.

Why Buy Now: 1) The Kochi plant utilization will improve with the addition of linkage gas pipelines in the next 1 year. 2) The Dahej facility will add 50% capacity in the next 2 years, which is already connected to consumers. 3) We anticipate the fall of LNG prices in the spot market, which will grow gas demand. 4) The PLNG share is today at 22% below the 185 high of Aug 2011. Thus the current market price offers an attractive entry point with a low downside probability.

Petronet LNG – Description and Profile

- Petronet LNG (PLNG) imports, regassifies & sells gas in India, and is a JV of GAIL, ONGC, Indian Oil and BPCL.

- Turnover in FY14 was Rs.37,747 cr. and PAT 711 cr. PLNG owns and operates two LNG terminals, at Dahej, Gujarat (capacity 10 million metric ton per annum – mmtpa) and Kochi (5 mmtpa).

- Long-term contracts are in place for LNG supply from RasGas-Qatar (7.5 mmtpa), Exxon Mobil-Australia (1.44 mmtpa) and Gaz De France (0.6 mmtpa). These are at lower prices than spot prices.

- PLNG also takes spot cargoes to meet demand and utilize available capacity. Spot price of LNG has been rising from 3-4 $/mmbtu a few years ago to 17-18 $/mmbtu today.

- Sales of the long-term contracted gas are through GAIL, IOCL & BPCL, where PLNG keeps a regasification margin. With spot cargoes PLNG earns both marketing and regassification margins.

- Imported LNG is regassified and supplied in pipelines or Cryogenic road Vehicles. The customers include power plants, household & commercial piped gas, fertilizer plants, Industrial boiler fuel, etc.

- India Ratings has upgraded PLNG long-term issuer rating to ‘IND AA+’ from ‘IND AA’ while its Short-Term Issuer rating has been affirmed at ‘IND A1+’. The Outlook on the Long-term rating is Positive.

- Shareholdings pattern is: Promoters 50%, MFs/ DII 4.8%; FIIs 18.9%, Individuals retail /HNI 13.4%, Bodies Corporate & others 12.9%.

- PLNG has a private company status (PSU holdings <51%) that gives it operational flexibility.

- Key Executives: Dr. AK Balyan (MD/CEO), Rajender Singh (Dir. Technical) and R K Garg (Dir. Finance).

Current Projects

- PLNG has signed agreements to supply LNG to bulk consumers in Power, Refineries & Fertilizers.

- Its joint venture with Adani Port for bulk Solid Cargo, Adani Petronet Port at Dahej, has commissioned its second jetty expanding its capacity to 20 MT/ year at an investment of 750 cr.

- PLNG also directly markets LNG through trucks to LNG hubs and Satellite Stations to customer premises in regions not serviced by pipelines under the Brand name of Tarai Gas.

- The recently commissioned Kochi terminal is being utilized to the extent of only 8%. PLNG set up the plant successfully, but its connectivity to demand centers through pipelines has been delayed inordinately. See Fig 1.

Fig 1 – Demand Centers for PLNG Kochi, JainMatrix Investments

(Click on any image in this report to enlarge)

- GAIL is tasked with the creation of the Kochi/ Mangalore/Bangalore pipeline. This ran into local and political opposition, which delayed it. It is anticipated that this crucial infrastructure will be created in the next 12 months.

Future Plans

- PLNG is exploring supply of LNG to coastal area consumers with LNG Vessels.

- PLNG has signed the term sheet for a LNG Terminal at Gangavaram Port, AP, of 5 mmtpa capacity. It will be commissioned by 2016, at an investment of 4,500 cr. It received the MoEF clearance for 10 mmtpa LNG facilities.

- PLNG board has approved setting up of a wind power generation plant of 40 MW at a cost of 250 cr. Commissioning is expected in next one year.

News

- Oman may buy stake in PLNG’s planned unit at Gangavaram Port, of about 10-15% in this project, the Gulf nation’s oil minister Mohammed bin Hamad Al Rumhy said.

- PLNG will lease out almost half of the capacity at its Dahej liquefied natural gas (LNG) terminal from 2017 as prices for the high-cost fuel have cut demand. PLNG has signed 20-year deals to lease 6 mmtpa of the terminal’s capacity to GAIL, IOC, BPCL and the GSPC in Gujarat.

- PLNG is bullish on the domestic demand for LNG. The company will continue importing LNG in future and expects LNG prices to drop to $15/mmbtu in near-term from $17-18/mmbtu currently.

- PLNG wants IOC to drop Ennore LNG terminal project. With Indian Oil Corp (IOC) planning to set up two LNG terminals on the east coast, PLNG has raised the issue of duplicate infrastructure and has offered to meet all of its gas needs through the Gangavaram facility.

- PLNG plans to lease out one of the two storage tanks at its newly commissioned Kochi terminal to make the under-utilized facility commercially viable.

Industry Notes

- Gas is a better fuel than Coal, Oil and Nuclear. It burns almost completely, so is the cleanest fuel.

- India is a major gas/LNG consumer (13th position globally) and importer (5th largest).

- The Indian economy is growing at a CAGR of 6-7% with similar growth in energy consumption.

- Oil regulator PNGRB has extended the last date of bidding for licenses to retail CNG and piped cooking gas in 14 cities, including Bengaluru and Pune, by three months to 12 May’14.

- Following the nuclear disaster in Japan in March 2011, there has been a big spurt in demand and also spot prices of LNG in Asia. See Fig 2.

Fig 2 – Natural Gas Spot Prices

- The huge demand/supply gap for gas is expected to continue for years to come. The demand: supply ratio in ‘13-14 was 2.42 and is expected to reach 2.57 in 2019-20 and 3.1 in 2029-30. Se Fig 3.

- Indian gas demand is expected to reach 713.5 mscmd by 2030, compared with a supply of 231.4 mscmd. Thus there is a pent-up demand for gas. Domestic supply of Natural gas from Reliance (Krishna Godavari), ONGC and Oil India wells has not scaled up to meet this demand.

Fig 3 – Gas Demand Supply Gap

- The share of natural gas in Indian energy basket should increase from 10% to 20% by 2050. Fig 4.

Fig 4 – Energy Consumption, JainMatrix Investments. (Click on any image to enlarge)

- Other LNG terminals are Hazira (Shell, 3.6 mmtpa), RGPPL, Maharashtra (GAIL – NTPC JV 5 mmtpa).

- Other proposed regasification terminals in the country are Pipavav LNG terminal, Mundra LNG terminal (JV of GSPC and Adani, 5mt/year), Ennore LNG terminal (JV of IOCL and TIDCO), Mangalore LNG terminal and Paradip LNG Terminal (GAIL, 4.8 mt/year)

Stock Evaluation, Performance and Returns

- PLNG had its IPO in Mar’04 priced at Rs 15, and was subscribed 4.2 times. The price rose to 120 in Jan’08, in the financial crisis fell to 30 in Nov’08; the all time high was 186 in Aug’11.

- PLNG at CMP of 146, has given IPO investors a 28% return CAGR in 11 years, Fig 5. The maiden dividend of Rs 1.3 was paid in 2007. Thereafter dividend has shown a steady increase.

Fig 5 – PLNG Stock Returns, JainMatrix Investments

- Revenues, EBITDA and Profits have grown at 34%, 9% and 7% CAGR over 6 years (Fig. 6).

- The Quarterly Operating and Profit Margins have fallen from early years even as volumes have ramped up rapidly. The Earnings per Share (EPS) grew till FY12 but has shown declines thereafter.

Fig 6 – Quarterly Revenues and Profits, JainMatrix Investments

- Cash flow and EPS have a robust growth rate Fig 7. The Cash flow from operations is up 23% CAGR, but annualized EPS is up only 7% CAGR over last 6 years.

- With good cash flow, PLNG has repaid some debt and D/E has fallen to 0.61, quite good.

Fig 7 – Cash Flow and EPS, JainMatrix Investments

- Price and PE chart (Fig 8) shows that the historical mean of PE is 14 times. PE today is 15.3 and so the stock is just above average valuations.

Fig 8 – Price and PE Chart, JainMatrix Investments

- Price and EPS quarterly graph, Fig 9, shows that EPS grew sharply in FY11-12, but recently it is in a declining trend.

- We can see in Fig 9 that the share price anticipates EPS performance by about 1 year, in both EPS peaks and troughs. The current share recovery too appears to be factoring in a 2015 EPS gain.

Fig 9 – Price and EPS chart, JainMatrix Investments

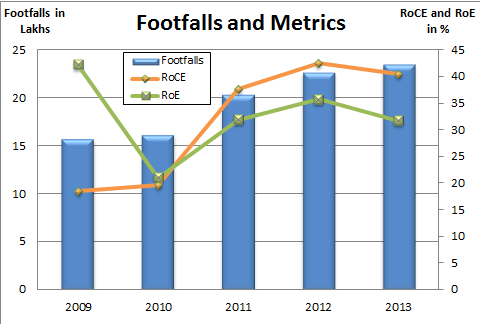

- The company has an interest coverage ratio of around 15.5 times which is good.

- ROCE and RONW are over 25% in FY14, which is excellent.

- Beta of the stock is 0.36 (Reuters) and this indicates much lower volatility to that of the Sensex.

- PEG is at 0.32 – indicates safety and great value.

Opinion, Outlook and Recommendation

- India continues to be fuel starved, with many projects suffering for lack of gas supply. Domestic gas findings have underperformed and there is a large demand supply gap.

- All PLNG capacities are fully utilized except Kochi where there is a temporary delay in pipeline infra.

- Our opinion is that Kochi capacity utilization will move to 30% (in 1 year) and 80% (2 years). The TN section pipeline – disputes should get resolved (6 months), and constructed (1 year thereafter).

- We are confident that in 2 years not only the current capacities, but also newer additions will be well utilized. Gas volumes supplied by PLNG will double by end 2016.

- The PLNG share is today at 22% below the 185 high of Aug 2011. The recent low was 102.5 in Jan 2014 from which it has recovered sharply. This fall is complete.

- The worst is over for the PLNG stock and the next 2 years will see a recovery – both of the 2013 financials high, and the past peak share prices.

- Invest now and systematically to gain from long-term out-performance.

JainMatrix Knowledge Base:

See other useful reports

Do you find this site useful?

- Visit the SUBSCRIBE page to find how you can get more. Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Either JM or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com

Click and Share this post :