_______________________________________________________________________

- Date 10th March 2015

- Price range: Rs. 221-230 with Retail discount

- Period: 10-12th Mar 2015

- Small Cap – Rs 1800 cr Mkt Cap; Industry – Amusement Parks

- Advice: High Risk, Avoid

Summary:

Summary:

- Adlabs Entertainment has two new amusement parks that are wonderful properties with unique attractions and located in an affluent customer catchment area.

- However Adlabs is loss making. It has a high cost structure. It is still stabilizing operation in its two parks. There are access and maintenance challenges. The amusement holiday concept has still to be proven in the Indian context.

- Current revenue levels are unsustainable. We feel that only if revenues ramp up sharply from here, will Adlabs be able to achieve profitability in 2 years.

- As an investment, the Adlabs IPO is rated a high risk, Venture Capital type offering.

- Investors can avoid this IPO.

Here is a note on the Adlabs Entertainment Ltd. IPO. (ADEL)

IPO Highlights

- IPO is open from 10-12th Mar 2015 with Issue Price band: Rs.221-230 per share

- There is a discount of Rs 12 for Retail category only

- Shares offered to public: 2.03 crores of Face Value: Rs.10 per share

- Shares offered as portion of equity post issue: 25.44%

- Amount proposed to be raised: Rs.450-468 crores.

- IPO proceeds: Rs. 330 cr. for partial repayment of Bank loans taken to set up amusement park near Mumbai. One of the Promoters will exit partially to the extent of Rs 46 cr. The rest of the amount will be utilized in general corporate purposes.

- ADEL is a loss making operation as of today, and is only EBITDA positive since FY14.

- News – ADEL raises Rs 60 cr. from anchor investors ahead of IPO, a positive for this IPO.

Introduction

- ADEL is an Indian amusement park firm based in Mumbai. It has two operational parks adjacent to each other, Imagica Theme Park (fully functional since Nov 1, 2013) and Aquamagica, the water park located adjacent (operational since Oct 1, 2014).

- The park is located in near Khopoli, and is 74 km from Mumbai, off the Mumbai-Pune Expressway.

- Next to the parks is planned a 3 star hotel with 287 rooms (116 rooms will be ready by Apr 2015).

- This addition will promote amusement vacations and provide synergy with Lonavala, Matheran and Khandala, tourist locations close by. ADEL also attracts customers from nearby Mumbai & Pune.

- Revenues in FY14 were Rs 107 cr and Losses Rs 52 cr. They have 1,248 employees.

- The promoters of ADEL are Mr Manmohan Shetty, and Thrill Park, a company with ownership again primarily with Manmohan Shetty. Mr Kapil Bagla is Exec. Director of ADEL.

- Imagica and Aquamagica have among the highest entry ticket rates for amusement parks in India, with Rs 1900 and 1150 (off season 1500 and 950). The business model is mostly an entry ticket which allows unlimited usage of rides. The additional revenue sources are specified in Fig 1.

- Future projects include new parks at Hyderabad and Gujarat, but these are at very early stage today.

Fig 1 – Revenue Segments at Adlabs Imagica

Financials of ADEL

- ADEL has not yet completed one full financial year with both parks operational. However the data from 4 quarters ending Dec 2014 indicates annual revenue run rate of Rs 210 cr.

- There are large loans on the books, a total of 1084 cr. as on Dec 2014. As a result, the Finance and Interest charges are high. Additionally, depreciation and amortization charges too are high.

- The firm has a Debt Equity D/E ratio of 4.9, which will reduce to 3.7 after IPO due to repayment from proceeds. This is very high indeed.

- Financials are captured in Fig 2.

Fig 2 – Adlabs Financials, Source Company documents, click image to expand

Business Profile

- The nature of the amusement park business is of a large initial capital investment in land, permissions, rides, hotel and branding. Then follow growing the footfalls and revenue.

- Capacity: the capacity of the theme park is 15,000 people hourly (as per Company Prospectus). The highest usage was in Q3FY15 with average footfalls 3,171 per day and the record for one day is 11,933. For the water park capacity peak is 5,450 and average footfalls inQ3FY15 were 819.

- Data from Wonderla parks indicates a capacity utilization of 23-27%. If we set ADEL utilization at the upper end of this range, the Theme park footfalls could go up 28% to 4050.

- The last 4 quarters saw footfalls of Imagica (9.12 lakh) and Aquamagic (3.01 lakh) totaling 12.13L. Management has commented on a need for annual footfalls of 14 lakh in order to become a cash positive company. Its only after this that ADEL starts repaying its loans.

Industry Data and Personal Notes

- The amusement park industry in India is estimated at worth Rs 7,000 cr and has grown at 15-20% CAGR.

- ADEL thus appears to have only a 3% market share of this industry.

- Other players include Wonderla Holidays, Ocean Park Hyderabad, Essel World/ Water Kingdom Mumbai, FunNFood Village Gurgaon, Adventure Island Delhi, Nicco Park Kolkata, Entertainment City Noida, MGM Dizzee World Chennai and Ramoji Film City, Hyderabad.

- Globally it’s a very massive industry with the likes of Disneyland and Universal Studios of USA dominating. Like many others, this sector could also see the entry of MNCs and foreign investments in future. Any such event will raise the valuations for ADEL.

- Demand drivers: India’s per capita income has grown at a five-year CAGR of 16%. Also, the share of discretionary spending in overall expenses has increased rapidly from 19% in FY1981 to 45% in FY12. This has led to higher spending on leisure and entertainment activities such as visits to multiplexes, malls, vacations, restaurants and amusement parks.

- Personal Notes – A visit to Adlabs Imagica in Dec’14 provides the following insights on the business:

- Connectivity with Mumbai while good on the Expressway, is poor on the last 4-5 km stretch.

- Some of the larger rides were out of operation, for maintenance.

- However all the functioning rides were well conceptualized and uniquely Indian rides, celebrating and packaging India’s cultural, natural and historical diversity.

- A visit here is a whole day picnic, and there’s ample potential for F&B and allied services.

- There’s a massive demand from affluent city visitors for this unique experience. The focus has to be on schoolchildren, young parents and under 30 thrill seekers.

- The likely sequence of business events in future for ADEL, post IPO are:

- Commissioning of 3 star hotel adjacent to parks by Apr 2015.

- Marketing of parks as a holiday destination in Mumbai, Pune and other Metros in India.

- Improved operations and utilization of current park facilities, so cash flow is better.

- Repayment of loans by ADEL from internal cash flow, reducing finance and interest costs.

- Expected operational cash positive performance of ADEL in FY15 and 16.

Positives for the IPO / ADEL business

- Demand and Demographic Advantages. India is one of the youngest countries in the world with the median age of 26.5 years, compared to 37.1 years in US, 45.4 years in Japan and 35.9 years in China (Source: CIA, The World Factbook and CARE Research). This will drive demand for ADEL.

- Rising Income Levels. In the last decade, Indian economy has progressed rapidly. With the progress of the economy, India’s per capita GDP (constant price) has gone up from Rs. 32,037 in 2005-06 to Rs. 46,555 in 2011-12, fuelling a consumption boom in the country. (Source: CARE Report)

- Increased Spending on Tourism and Leisure Activities. In the last 6-7 years, there had been a steady growth in domestic spend on tourism, growing at a CAGR of 13.7% to USD 73.4 billion in 2011. Holidaying, leisure and recreation related tourism constitutes major part of the domestic tourism.

- ADEL has conceptualized and created a massive 132 acres amusement park on the lines of the large and successful parks like Disneyworld abroad. At the same time, the themes, concepts and execution of rides is uniquely Indian, combining entertainment with education and culture. This is very visionary thinking. In addition a strong brand has been built in a fairly short period.

- The promoters are media and entertainment savvy professionals and entrepreneurs.

- The key assets with good capacities are in place and operational. ADEL now needs to steadily build the brand, demand, utilization, maintenance and improvements of these.

- In the Mumbai – Pune catchment area, there are few comparable competitive entertainment destinations. Only Essel World and Water Kingdom come close. They are older properties, but are better located close to Mumbai city. ADEL parks are refreshingly different and offer an attractive option to customers.

Internal Risks

- High costs structure: The large bank debt and VC funds taken for the project are reflected in the high finance and interest costs. Operational costs too are high. The IPO can only rest a part of the loan. Already a repayment due Dec 2014 has been mutually deferred to March 2015 post IPO. The fear here is that ADEL may not be able to ramp up revenues fast enough to stay ahead of the repayment cycle demanded by lenders.

- The Promoters have also pledged part of their shares to raise loans for the ADEL operations. This is a high risk situation as any subsequent fall in share price after listing will trigger a share sale.

- Rider Safety: The safety of amusement park visitors is important, and it is an ongoing challenge to keep up high maintenance and well-marked safety regulations for visitors, to prevent mishaps. ADEL has had 1-2 accidents so far, but has an overall good record. This must sustain.

- The hotel project needs to be commissioned on time, and launched successfully promoting the amusement + holiday synergy. Any delay could adversely affect the business performance.

- Changes in consumer preferences could adversely affect the business. Typically a repeat visitor may like to see new rides and innovation in amusement rides, this is an ongoing challenge for ADEL.

- There is no clarity on Hyderabad and Gujarat projects, so we cannot assume any revenues there.

External Risks

- Litigations: There are several suits pending in courts against Promoters, ADEL, directors and group companies. We cannot be sure if the future business will be affected.

- A slowdown in economic growth in India could cause the business at ADEL to suffer.

- Competition from existing and new players. A slew of new projects are in the pipeline.

Benchmarking

Since ADEL is loss making and just recently launched, a benchmarking exercise against other firms is inappropriate. However, a simple revenue to market cap comparison with closest competitor Wonderla Holidays reveals:

Fig 3 – Comparison of ADEL and Wonderla

This simple comparison indicates that ADEL may be only 14% overpriced compared to WHL. However in reality ADEL has a massive cost disadvantage due to the recent construction. And WHL has mostly older operating assets and is investing in a new amusement park. WHL is identified as a safer investment.

Overall Opinion

- There is no doubt that the new parks of ADEL are wonderful properties with unique attractions and located in an affluent customer catchment area.

- However ADEL has a high cost structure. It is still stabilizing operations in its two theme parks. There are access and maintenance challenges. The vacation amusement concept still has to be proven in the Indian context.

- Current revenue levels are unsustainable. We feel that only if revenues ramp up sharply from current levels will ADEL be able to achieve profitability in 2 years.

- As an investment, the ADEL IPO is rated a high risk, Venture Capital type offering.

- Investors can avoid this IPO.

JainMatrix Knowledge Base:

See other useful reports.

- Page Industries – The Jockey Rides Too Fast

- The Case for the JainMatrix Direct Equity Service

- Snowman Logistics IPO

- Wonderla Holidays IPO

- CPSE NFO

- Godrej Properties – A Towering Success

- Yes Bank

- Balkrishna Industries

- Mindtree Ltd.

- Adani Port and SEZ

- BHEL

Disclaimer

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. JM has no known financial interests in Adlabs Entertainment Ltd or any related firm. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Either JM or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com

Fig 1 – Products by Revenue

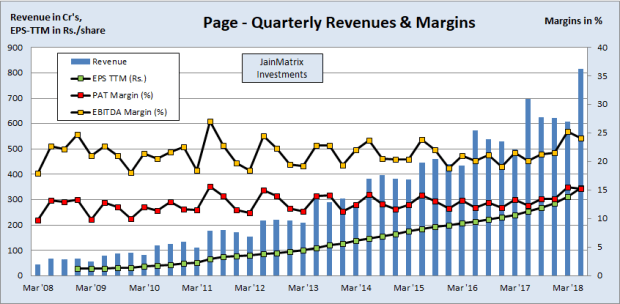

Fig 1 – Products by Revenue Fig 2 – Page Financials and Fig 3 Cash Flow, Dividend

Fig 2 – Page Financials and Fig 3 Cash Flow, Dividend

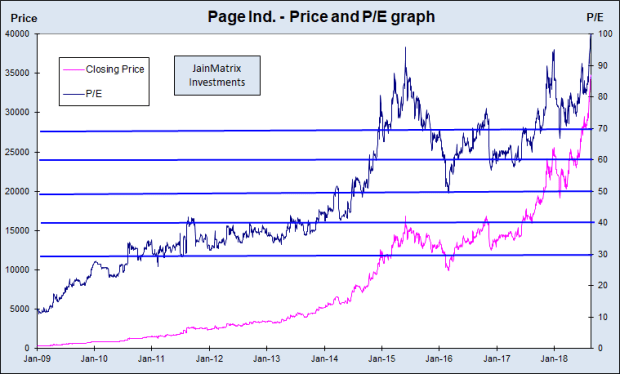

Fig 4 – Price and PE Chart, and Fig 5 – Price and EPS Chart

Fig 4 – Price and PE Chart, and Fig 5 – Price and EPS Chart Fig 6 – Finance Metrics

Fig 6 – Finance Metrics Table 7 – Benchmarking and Table 8 Projections

Table 7 – Benchmarking and Table 8 Projections