SUMMARY

- Date: Dec 6th 2012

- Offering: Price Range Rs 210 – 240

- Issue Period: Dec 11 – 14

- Retail gets an additional discount

Description: Bharti Infratel runs the tower network for Airtel, and also partners for this with Vodaphone and Idea. The business is sticky in terms of customers and has stable cash flows. The telecom sector is at an early stage of growth in India. Risks: The business is capital intensive. There is regulatory and litigation uncertainty. BIL has only recently turned Free Cash Flow positive. Opinion: BIL has the leadership and first mover advantage. The aggressive pricing may be justified by high growth, good financials, and resurgent industry. Invest for the long term, at Cut Off price.

Bharti Infratel – Description and Profile

- Bharti Infratel (BIL) was started in 2006 as the tower subsidiary of Bharti Airtel. Revenues in FY12 were Rs 9597 crores with PAT 751 cr. Operating & profit margins are 38% & 7.8%.

- BIL owns 33,000 towers, and holds 42% stake in Indus Towers, which has 110,000 towers. BIL thus owns 80,656 towers, a 21% share of the tower industry (and a combined 143,300 and 38%).

- BIL, along with Indus, currently employ 2521 staff directly, and 5659 indirectly. Operations are spread across all 22 Telecom circles of India.

- Currently Airtel owns about 86.1% of BIL, and PE firms 13.9%, see Fig 1. But Airtel will not sell any shares in IPO. So after the issue, its stake would fall to 79.4% and the PE firms will fall to 10.5%.

Why Is BIL going for an IPO?

The objects of the issue are:

- Investments in Installation of 4,813 new towers – 1087 cr.

- Upgradation and replacement on existing towers – 1214 cr.

- Green initiatives at tower sites – 639 cr.

- General corporate purpose and partial exit by investors Temasek Holding, Goldman Sachs, Anadale and Nomura – Over 1060 cr.

Soft Benefits:

- In future Airtel can sell its shares and deleverage its stressed Balance Sheet.

- Overall valuation of Airtel will get a boost on successful listing of BIL, since it retains 79% ownership.

Telecom Industry

- The Indian telecom industry revenue reached Rs 1,36,100 cr. by Mar’12, and the mobile subscriber base is around 91.9 cr. Of that number, approximately 86.8 cr. are 2G subscribers and 5.1 cr. 3G.

- The industry has gone through phases. While the 1990-’99 phase was an introduction phase, the 2000-’10 period saw massive industry and subscriber growth. We are now in a phase of hyper competition /consolidation, where operators may reduce from 12-15 to 6-8. For details, see LINK.

- The business model is based on leasing of towers by service providers on 10-15 year contracts. There is customer stickiness and the revenue model is stable.

- The total number of towers today is 376,000, and the Tower tenancy average rate for the industry is 1.7. BIL enjoys a higher tenancy of 1.9. The 1.7 – 1.8 range is considered the break-even point. Tenancies for independent telcos are estimated at around 1.46 times.

- BIL is a pioneer in the industry as it initiated co-operation and alliances in the telecom towers industry. As a result, from being a competitive scenario, industry players were able to grow tower numbers rapidly and at the same time reduce costs of this critical infrastructure by sharing.

- Airtel along with partners Vodaphone and Idea together having 68% of the mobile market by Revenue Market Share. They are also incumbents growing fastest. Thus BIL is in the safest position in the industry in the form of market share, growth prospects and revenue stability.

- The key drivers for tower and tenancy growth will be: 1) Rural 2G expansion 2) new 3G capacity 3) Usage of higher frequencies 1800MHZ+ which is more tower intensive and 4) new 4G coverage.

- Operating Costs structure of industry indicates that 50% of Opex is Energy, of which again 60% is Diesel costs. This is a risk as there is a good chance Diesel prices may be raised as it is subsidized.

- Companies also face several barriers in the form of the complex and time-consuming approval process for the deployment of new towers, and public fear of radiation from current towers.

- Industry players include Indus towers (109k towers), Reliance Infratel (50k), Bharti Infratel (33k), Viom Networks (42k), GTL Infra (33k), ATC (10k), Tower Vision (8k) and Ascend Telecom.

- There are significant entry barriers for new players as the business is capital & technology intensive.

BIL financials:

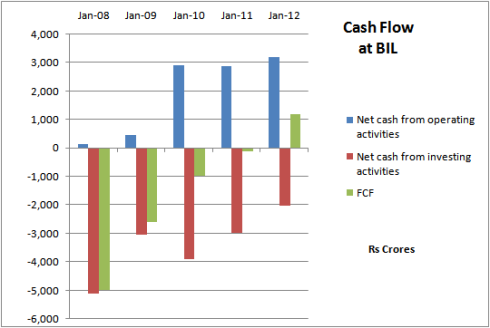

- We can see at a glance that financials are good. Revenues, EBITDA and PAT have increased at 23%, 31% and 57% CAGR over the last 3 years. Fig 3.

- The Free Cash flow of BIL has improved a lot from FY09, and turned positive in FY12. Fig 4.

- Low debt-equity ratio of 0.2 times.

Key Strengths of BIL

- Pioneering status in industry. Largest market share in a high growth industry.

- Sharp business focus on growth and maintenance of passive telecom infrastructure.

- Stable long term revenue visibility; High tower tenancy at 1.9 compared to industry average of 1.7

- Low debt-equity ratio of 0.2 times, and Positive Free Cash Flows of late

Key Weaknesses/ Issues/ Challenges of BIL

- It’s a capital intensive business. As of now, BIL’s RoE was low at 5.3% in FY12.

- Diesel is key input, and prices can be raised unexpectedly.

- Industry in a financially stressed condition, due to regulatory overhang, hyper completion and stabilizing of subscriber growth. There is an ongoing consolidation in the industry.

- While market pressures have resulted in consecutive quarter-on-quarter reduction in profits for several companies including Bharti Airtel, a recent SC order on telecom licenses has forced operators to go slow on rollouts, reducing business for tower providers.

- Regulatory uncertainty: BIL’s operations may be affected if certain proposed regulatory measures with respect to tower sharing among service providers, etc. are implemented.

Strategic Thoughts around this IPO

- Telecom is a key infrastructure for a country, and the availability drives individual and corporate productivity. The benefits of mobiles are massive, and have changed our way of doing things.

- Even today India is at an early phase of telecom usage. While raw penetration numbers indicate a saturation level, the fact is that (as per TRAI data of Mar ‘12) urban wireless penetration was 162.8% while rural wireless penetration was 38.3%, indicating:

- New connections growth will essentially happen in rural areas, with churn in urban areas.

- Market maturity will start with urban areas, where newer data intensive apps and smartphones will drive demand and consumption of telecom services.

- Bharti Airtel is approaching the markets to list a firm after 10 years. The firm through this period has set new standards of business innovation, transparency, shareholder rewards and growth.

- BIL has a unique model of passive infrastructure sharing, and cooperation among competitors.

IPO Offering Outline and Valuations:

- Offer is of 18.89 cr. shares in price range Rs 210-240 available from Dec 11-14th.

- This 10% dilution will collect upto Rs 4530 cr, and value the firm at 45,000 cr. market cap.

- Market Lot – 50 Equity Shares

- Maximum Subscription Amount for Retail Investor – Rs. 2,00,000

| Valuations based on FY12 financials |

PE range, TTM

|

PEG range, TTM |

Forward EV/ EBITDA |

Valuation per tower |

| Bharti Infratel |

53 – 60 times |

0.93 to 1.07 times |

9-10.5 times |

50-57 lakhs |

| Comments | Aggressive pricing, but IPOs from leaders come at high prices | Indicates fair valuation compared to growth rates | Is reported to be cheap compared to global peers | Is cheap compared to stake sale deals done in 2009 (78L) and 2007 (120-160L). |

Fig 5: Multiple Valuation approaches

- We can see that the Per Tower valuation has fallen significantly from 2007-09 levels. This can be explained by the current ‘hyper-competition’ phase of this industry. This may ease off in 2-3 years.

- The reported forward EV/EBITDA value claims to be cheaper than global peers. However it should be noted that the Indian industry is very different from these, both from a development phase and a technology point of view, so this is a weak input.

- While the PE range of the offering is high, it is justified by the growth, giving a fair PEG value range.

- CRISIL Research assigns IPO grade ‘4/5’ to Bharti Infratel, indicating ‘above average’ fundamentals.

Opinion, Outlook and Recommendation

- Telecom as a sector is at an early stage of growth in India. For BIL, the business model while capital intensive, generates good cash flows. Utilisation and tenancy can only improve from here.

- The pricing, while apparently aggressive, commands a leadership premium and reflects a first mover advantage. Bharti Infratel is a good long term investment opportunity.

- Airtel has always been a favourite among the institutions. The recent surge of Airtel stock by 36% from its Aug’12 lows is at least partially due to news of the BIL IPO.

- With the recent uptick in the indices, BIL looks set to capture the imagination of newer investors. There may be pop on listing.

- Invest for the long term, at Cut Off price.

- Check back on the website www.jainmatrix.com for updates.

JainMatrix Knowledge Base:

- CARE IPO – they do care about shareholders – LINK

- Bharti Airtel – This is a year of consolidation – LINK

- Telecom – Auctions speak louder than words – LINK

- TBZ: A Glittering IPO Offer – Invest – LINK

- MCX – 800 pound Gorilla of Commodities; Invest – LINK

Subscribers have already received this high quality report. Join this elite group, subscribe to JainMatrix Investments.

- Check back on this site, for updates and a release of the report for public viewing.

- You can also subscribe for my posts by filling the ‘Sign me up’ box on top right of this page.

- Do you find this site useful? Please comment below.

Disclaimer:

These reports and documents have been prepared by JainMatrix Investments Ltd. They are not to be copied, reused or made available to others without prior permission of JainMatrix Investments. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com Also see: https://jainmatrix.wordpress.com/disclaimer/

Leave a comment