Did you know that the DIP SIP is the most efficient way to invest in the stock market? We at JainMatrix Investments recommend investors to invest in equities in a Direct Equity – DIP SIP mode. Let us explain this process.

What is a DIP SIP?

A Systematic Investment Plan or SIP is a smart mode for investing money which allows you to invest a certain pre-determined amount at regular intervals (weekly, monthly, quarterly, etc.). A SIP is a planned approach towards investments where the saving habit becomes a routine. The SIP approach can be used for any investment vehicle, such as FDs, MFs, Direct Equity, etc.

A DIP SIP is a Direct Equity SIP, where the investor invests systematically in the identified stocks.

Why Equity investments?

Historically investments in Equity have given higher returns amongst all the other asset classes if investment was done with discipline and a long term time horizon. See an assets map where we present a number of asset classes and the Risk-Return trade off, Fig 1.

What are the benefits of an Equity DIP SIP?

- Direct equity allows the buyer to become a shareholder, and gains from dividends and is informed directly by the Corporates about splits, bonuses and announcements.

- Ride the Volatile Equity class and reduce Risk with Rupee Cost Averaging

- SIP can be started with very small amount of money, and increased at a later date

- Timing the market is not necessary. But gains are best when markets are below all time highs.

- Long term financial goals can be aligned with SIP

- Disciplined approach towards Investment helps in controlling the emotions

- Investments get aligned with income flow and it becomes a regular habit

The JainMatrix Investments Companies Baskets

JainMatrix Investments launched its Large Cap Companies Basket in Dec 2012, the Mid & Small Cap MSC Companies Basket in Feb 2013 and the Satellite Companies Basket in its current form in Mar 2021. These three baskets are chosen from 120+ stocks that we have researched over the years. The main reason for three separate Baskets is to offer simple investment choices, and to align with the risk appetite of different investors.

- The Large Cap LC Companies Basket consists of 7-8 stock picks from 7-8 different sectors. The blue chip firms chosen are high potential large caps with good fundamentals and safety. The investment period is 2-3 years. The objective is to outperform the Sensex/ Nifty every year by 2-3%.

- The 7 stock picks from the Mid & Small Cap MSC Companies Basket are from 4-7 high potential sectors. These firms have good fundamentals and high growth. The minimum investment period is 1-2 years. The objective is out-performance of Mid and Small cap Index benchmarks.

- The Satellite Companies Basket has 7 stock picks from 4-7 high potential sectors. The minimum investment period is 12-18 months. Here in addition to the fundamentals we pick firms with appreciation triggers and a visible momentum. The objective is out-performance of Mid and Small cap Index benchmarks.

DIP SIP and equity MF SIP compared

Now that you have understood the equity SIP mode of investment, it is imperative to compare DIP SIP – investing directly in Equity with equity Mutual Funds.

1 – Expense Ratios

Investments in equity Mutual Funds are expensive in terms of the expense ratio cost incurred to the investor. Total Expense Ratio (TER) states how much you pay a MF in percentage terms every year to manage your money. This includes the fund management fee, agent commissions, registrar fees, and selling and promoting expenses. The TER that is disclosed every March and September as a percentage of the funds net assets. As you grow your investment portfolio over the long-term, a high expense ratio will eat into your returns through power of compounding. The expense ratio of equity MF’s is typically in the range of 0.5%-2.25%. See Fig 1. You do not directly pay this but it is deducted from the NAV of the MF.

Fig 2 – TER of a sample of equity Mutual Funds

In comparison to this, the JainMatrix Investment Service has a flat annual charge.

2 – Performance

Performance varies widely for equity from year to year. Subscribers to JainMatrix Investments may compare the performance of our portfolios with their owned equity MFs or widely published equity MF performance reports and take their own call on their preferred product or service.

3 – Control

Investors in MFs hand over the investment performance to the fund management team of the MF. They can now decide only to buy, hold or exit.

However in the case of the JainMatrix Model Portfolios, investors retain control over the purchases as the investments are in their own trading/ demat accounts. They can also follow the recommended companies as these are concentrated portfolios. This offers additional flexibility to investors for both entry and exits.

How to execute a DIP SIP?

Checklist for a Direct Market SIP:

- You can use your current Online Stock Broking account for the DIP SIP. If you have to choose among your broker options, choose the one with lower brokerage or better ease of use.

- Decide on the 7-14 stocks you will invest in.

- Decide on the amount you will invest every month – here I would suggest you fix an amount in the range of ₹ 20,000 to 1,00,000 for the DIP SIP and keep up this amount every month. The thumb rule here can be to invest 10-15% of your take home salary or 50% of monthly savings.

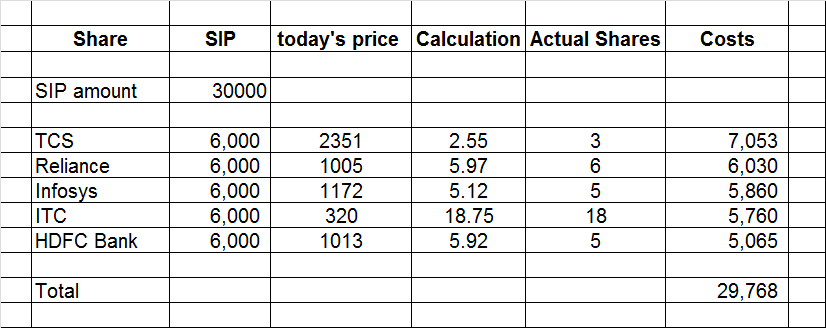

- Create a small calculation excel for helping you decide the actual number of shares to be bought. See Fig 3 – Tool for DIP SIP

- Decide a date for investing. If you are salaried, perhaps 2nd or 3rd every month is a good date as it is right after you have received your salary. Or any other convenient date. Keep a reminder for this.

Choose Your Stocks

This is an important step. My key principles in choosing the stocks are:

- For a high stability low risk portfolio, choose Large Cap (LC) blue chips. They should be Nifty/ Sensex stocks. You do not want too much volatility in this investment.

- For a more aggressive high risk portfolio, choose Mid & Small cap (MSC) stocks with high potential.

- The Satellite Portfolio is higher risk but potentially higher return group of stocks

- Occasionally you may add to the SIP bundle one time equity investment ideas or IPO opportunities

Subscribe to JainMatrix Investments Investment Service to receive proven, high performing portfolios

Start Investing

- Within trading hours, choose your DIP SIP portfolio of stocks. Lets say you chose these 5 shares by mkt cap in Fig 3.

- Lets say you have chosen the amount ₹ 30,000 to be invested every month for your DIP SIP.

- Create a small excel – which can help you calculate the number of shares right now. See fig 3.

- Round off the Actual Shares from Calculation tab to come close to your ₹ 30,000 budget

- Then buy the individual shares through your broking account to execute the DIP SIP

- Your DIP SIP can be done in 10 minutes every month.

Start your DIP SIP today. Subscribe to the JainMatrix – Investment Service to get our top performing Companies Baskets and recommendations and you are ready to go.

Click here to subscribe – LINK

Contact us on – LINK

Happy Investing!!!!!

Search for companies/ sectors of your interest in Search box in the right panel.

Visit and Like JainMatrix FB or Follow on JainMatrix Twitter for reports

Disclaimer

- Punit Jain discloses that all shares mentioned in this report are random samples/ examples chosen. These are not recommendations.

- This document has been prepared by JainMatrix Investments Bangalore (JMI), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JMI. This report should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JMI has not independently verified the accuracy or completeness of the same. Neither JMI nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Investment in the securities market are subject to market risks. Read all the related documents carefully before investing. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from a SEBI RIA Registered Investment Advisor. JMI has been an equity investment adviser commercially since Nov 2012, and a SEBI certified and registered since 2016, under SEBI (Research Analysts) Regulations. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the Research Analyst or provide any assurance of returns to investors.

- Any questions should be directed to punit.jain@jainmatrix.com. Name of the RA as registered with SEBI – Punit Jain, SEBI Registration No. INH200002747. Logo/brand name –