- 02 Apr 2014

- CMP: Rs 415

- Large Cap – Mkt Cap 14,900 crores.

- Advice: Buy

JainMatrix Investments has published a report on Yes Bank for its Subscribers. A partial report is available below. Edited from it are Financial metrics, Risk factors, Bench-marking, Financial Projections and 2 year target prices for YB stock. The JainMatrix Investment service is available for a subscription fee.

Key Reasons to Invest:

- The 24% fall since May ’13 is temporary in nature and gives an opportunity to invest at lower levels

- Aggressive growth will continue in 20-35% range, with stable NIMs and profitability

- Investments in Retail and SME will provide next phase of expansion

- Resurgent share price indicates a recovery has started

Description and Profile

- Yes Bank (YB) started in 2003, received the only greenfield bank license by RBI in last 15 years.

- Based in Mumbai, Yes Bank’s FY13 revenue was Rs 9551 crore and net profit of 1300 cr.

- Its market cap is 14,929 cr and it is among the top 6 private banks in India.

- The leaders are Rana Kapoor (Founder, MD, CEO), Alok Gupta, Aditya Sanghi and Ajay Desai.

- Share pattern %: Promoter 25.6, FIIs 39.6, MFs/DII 19.3, Retail/HNI 11.9, Corporate 2.5& Others 1.1.

- YB has employee strength of over 9000, the bank branches are 550 and about 1,150 ATMs in India.

- YB is focused on its Retail and MSME Loan portfolio, which has grown sharply, see Fig 1.

Fig 1 – Business Segments, JainMatrix Investments, click image to enlarge

Recent News and Updates

- The recent Q3FY14 results were good. Net profit at 415.6 cr grew 21.4% YoY. NIM at 665 cr grew 13.9% YoY. NIM is at 2.9%. However results were not as good as Q2FY14.

- RBI has permitted YB along with 5 other banks and 3 financial institutions to import gold under the 80:20 scheme. This is expected to lower gold cost and help the country’s external balances.

- YB has raised USD 500 m in foreign currency loans and deposits in FY14 after regulatory relaxations introduced in the fiscal. RBI relaxed regulations by raising the borrowings limit from 50% to 100% of Tier I capital and concessional FCNR (B) deposit swap window. The loan facilities will be used to scale up general corporate lending and small and medium enterprise loan portfolios.

- Ongoing Promoter legal tussle: Madhu Kapur, widow of Yes Bank co-founder Ashok Kapur, opposed in court the nomination of three directors to the lender’s board, an initiative led by her brother-in-law Rana Kapur. And, the Bombay HC admitted the plea.

- Revised monetary policies favor YB. The RBI’s move to boost liquidity has brought down the Marginal Standing Facility rate from 10.25% (in July’13) to 9.0% (in Jan’14). This is positive for YB due to significant wholesale funding.

- Savings rates deregulation in Oct’11 has aided retail customer acquisition, as YB aggressively hiked savings interest rates and shifted focus to growing the retail business.

Unique Strengths and Superior Strategies

- YB has a vision to become “A global bank” and “India’s #4 private sector bank by 2015”. They have invested 60-75 cr. to expand branch network, and plan to open 100 new branches.

- Their Vision-2015 was to create human capital of 12,750 employees, have 900 branch strength and a balance sheet of 150,000 cr. The bank is stretching to meet these objectives.

- YB is focused on research and knowledge lead banking services. It pioneers lending to new sectors that have high potential growth prospects.

- YB has a diversified and De-risked Credit Book.

Fig 2 – Diversified Credit Book, JainMatrix Investments

- YB practices a strong employee value proposition of “Creating and Sharing value” with a vision to build their organization driven by professional entrepreneurship.

- YB is focusing on the SME sector with access to finance and to help them excel in future.

- YB has aggressively grown the CASA deposits to 20.9% from 18.3% last year. YB offers the savings bank interest rate of 7%, which is highest in the industry.

- In an economy that used to be denied good banking, Yes Bank is building its brand around positivity, good services and fast approvals.

Stock Evaluation, Performance and Returns

- YB had its IPO in July’05 priced at Rs 45. It was 31 times oversubscribed. At CMP of Rs 414 today, the stock has given a 28% CAGR return since IPO.

- The share has risen well, but is volatile. After IPO, price rose to 277 in early 2008, fell to 41 in Mar ’09 and peaked at 547 in May ’13. Today, it is 24% below this peak price.

- The Price fall around July-Aug’13 was much sharper for YB (56%) than the CNX Bank (33%).

- This fall is linked to the events of 1) Taper of the monetary easing by Fed Bank in USA 2) A sharp fall in INR/USD value. 3) A case against YB by Promoter/owner Madhu Kapur.

- Also YB which was an investment & trading favorite and had touched its all-time high of 547 in May’13, may have fallen more sharply due to exits by the trading community.

- Total Income, NII & Other income and Profits have grown at 38%, 36% and 41% CAGR over 6 years.

Fig 3 – Yes Bank Financials, JainMatrix Investments

- While total income has grown rapidly, margins have fallen a little in the last 3 years. This is natural as Yes Bank is growing into a Large Cap from a Mid Cap size. See Fig 3.

Fig 4 – Yes Bank, Book Value, dividends, JainMatrix Investments

- The first dividend of Rs 1.5 was paid in ‘10, and since dividend has shown a steady increase, Fig 4.

- The P/B ratio has fallen over 6 years, in spite of price rise, due to rapid growth in Book Value.

- While NIM% has been flat for 5 years, other financial metrics like RoNW, RoE, CAR and CASA are showing YoY improvements. NIM has been between 2.7-3.2% over the past 5 years. This is low by industry standards as CASA is low. Capital Adequacy is at 18.3%, which is good. The ranges of ROE (20-25%) and RONW (15-23%) for last 5 years are high and growing.

- The PE chart 5 shows that average PE over the last 6 years has been 15, with a range 5-25.

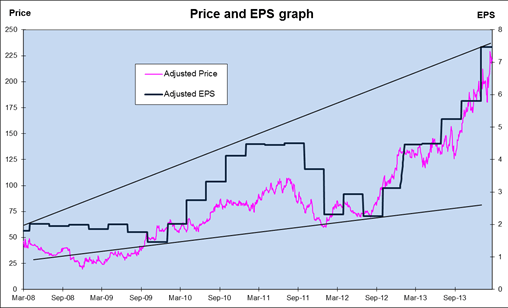

Fig 5-6 – Yes Bank PE and EPS charts, JainMatrix Investments

- PE has fallen today to 9.55 and is in the lowest quartile. This fall was in spite of EPS growth, Fig 6.

- Price and EPS quarterly graph, shows that EPS has been rising very steadily. The Share Price has been roughly following EPS, except for the last one year.

- We expect the EPS of YB to stay within the channel in Fig 6.

- It appears from Fig 6 that the price fall is not based on financials/ EPS but due to other reasons.

- Gross & Net NPA rose by Q3FY14 to 0.39% & 0.08%, but are still at lowlevels for the industry.

- Beta of the stock is 1.98 (Reuters) indicating high volatility.

- Dividend yield is 1.46%, which is good for the banking sector.

- PEG is at 0.36 – indicates safety and an undervalued stock.

Opinion, Outlook and Recommendation

- India is under-banked. There is potential for Banks to invest in new sectors and stimulate growth.

- The banking industry is a proxy to the overall economy, and should grow at 12-17% p.a.

- YB as a new private bank is well placed to exploit the trend of Private sector growing faster than PSBs, will continue to be in the 20-35% range for the next 3 years.

- The recent price fall of 24% since the peak in May ’13 provides an opportunity to invest in YB.

- In Mar’14 YB crossed its 200DMA and has stayed above it for 2 weeks already. It is a bullish sign and may signal a long positive period for the stock.

- YB will continue on the path of solid stock performance and dividends over the next decade. Invest now and systematically to gain for the long-term.

- Our Call is a BUY.

JainMatrix Knowledge Base:

See other useful reports

- JainMatrix Investments Mid-Cap Portfolio Investment Note

- Central Public Sector Enterprises ETF

- Are we in a new Bull Run?

- Engineers India

- Britannia Industries

- Just Dial

- Balkrishna Industries

- Mindtree Ltd.

- Adani Port and SEZ

- Power Grid of India

- BHEL

Do you find this site useful?

- Visit the SUBSCRIBE page to find how you can get more. Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer:

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor. Either JM or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com