_________________________________________________________________

- 23-Jan-2014

- CMP: Rs 1569

- Mid Cap – Mkt Cap 7910 crores

- Advice: Buy with a March 2016 target of Rs 3435

JainMatrix Investments presents investors the complete report on Bajaj Finance as part of the Investor Rewards Fortnight.

This is a follow-up report to the one published in Jan 2012, entitled – Bajaj Finance, Auto-matic Growth.

Business Profile

- Bajaj Finance (BFL) is a NBFC promoted by Bajaj Auto 26 years ago. Key management personnel are Rahul Bajaj – Chairman, Sanjiv Bajaj – Non Executive Vice Chairman and Rajeev Jain, CEO.

- The total Income in FY13 was Rs 3111 crore and PAT 591 cr.

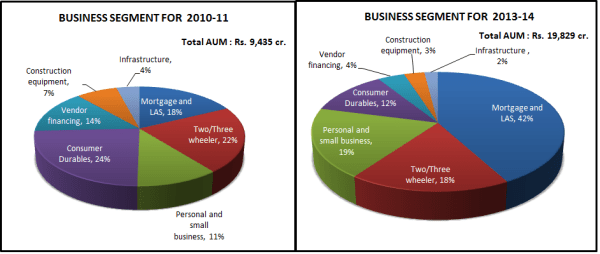

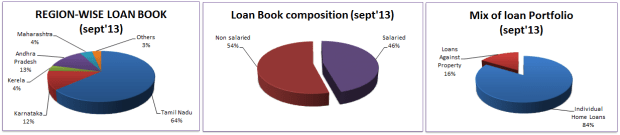

- BFL’s products portfolio includes loans for Consumer Durables, Personal use, Against Property & Securities, for Small Business, Construction Equipment, and Insurance Services. See Figs 1 & 2. About 60% of its business is consumer oriented – B2C, while rest is B2B, with a SME focus.

- About 30% of the 2&3 wheelers of Bajaj Auto are today financed by BFL. In the last 6-7 years, BFL has converted itself into a professional, diversified financing company.

- BFL has a network of 7,000+ distribution franchise across 112 cities, and 80 lakh plus customers.

- In 2013, BFL added 1,565 permanent employees, taking the total employee strength to 3,090. This is a sign of business confidence and investments in expected growth.

Fig 1 – Business Segments, JainMatrix Investments

- Funds sourcing – CRISIL has rated it at FAAA/Stable for FDs (high safety on timely payment of interest and principal), A1+ (short-term debt) and AA+/stable (long-term debt) by CRISIL & ICRA.

- The share-holding pattern is 62.1% Promoters, and public shareholding includes 11.3% individuals, 10.2% FII’s, mutual funds/UTI 7.9%, and bodies corporate 7.3% and 1.2% others.

Fig 2 – Product offerings, JainMatrix Investments

Recent News and Updates

- BFL had a Rights issue in Jan 2013, and raised 750 cr. The issue ratio was 3:19 and pricing Rs 1100.

- BFL extended its consumer electronics financing business recently to digital product financing.

- BFL also launched a rural financing initiative in 7 branches and 30 spokes in Maharashtra.

- The total customers acquired in Q3 FY14 grew by 15%.

- The firm’s borrowing mix from banks & money market is 60:40. This appears a balanced mix.

- The Bajaj Group has applied for a Bank license from RBI, which is expected to be issued in early 2014. There are totally 25 applicants. BFL is the firm proposed to be converted to a Bank if this application is successful. There may however be a need for a restructuring within the Bajaj group as after getting banking license there cannot be any preferential treatment to Bajaj Auto.

- BFL was rated by Aon Hewitt as one of the top employers in India in terms on Employee Satisfaction.

- Other business achievements – It is the first NBFC to launch online personal loans. It is among the few NBFC with active co-branded credit card (with Standard Chartered Bank. It is the first NBFC to tie up with UIDAI to access Aadhar card/eKYC database.

- The recent Q3FY14 results were good. AUM grew 33% to 22,461 cr; customers acquired during Q3 rose 15% YoY to 9,62,204 and deployments climbed 45% YoY to 7,532 cr.

Industry Note

- There are a large number of NBFCs in India (>10,000). These are relatively unregulated companies, unlike Banks that are governed by RBI. In this fragmented market, there is tremendous opportunity to offer Loans and Financial services.

- RBI has projected a 14% growth in loans for Banks; NBFCs should have higher industry growth rates of 24% for the next five years. (ICRA/ industry experts).

- Inflation and Interest rates are at highs in Q4 of FY14, which is difficult for the sector. However the 2 year outlook is a slow fall in both, even as the investment cycle recovers in India.

Unique Strengths

- BFL shares the strong ‘Bajaj’ brand; and is part of the growth of Bajaj Auto through Auto loans. BFL has a wide presence and leadership in high value Consumer Electronics and retail loans.

- BFL is diversified across customer segments and geographies; this de-risks operations and inspires a confidence in continued growth. BFL has a presence in 7 business sectors (Fig 1) and is nimble enough to shift focus to the performing sectors in order to achieve its targeted growth.

- The group financial services ambitions and new initiatives are going to be routed through BF.

- A strong distribution network, spread nationally with presence across customer segments, industries and geographies. The BFL strategy is to diversify their loan exposure with a 30% cap on each segment. This will provide a de-risked business model.

- With a wide product portfolio, BFL targets cross-selling and up-selling products to its customer base.

Stock Evaluation, Performance and Returns

- Listed since 1994, BFL performed well over the last 6-8 years, as seen in Fig 3.

- A sharp fall in price around Jan-Mar ‘13, was caused in part due to the rights issue.

Fig 3 – Share Price History, JainMatrix Investments

The fall we see around August ’13 is linked to the events of 1) threat of stoppage of the Quantitative Easing program in USA, 2) fall in INR v/s USD value. Most Bank share prices in India fell at this time.

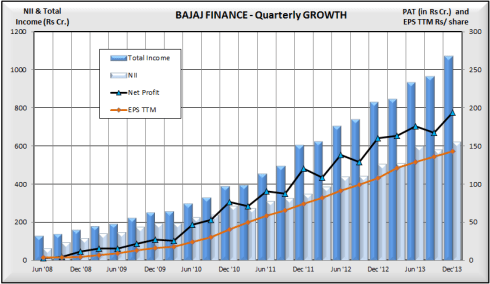

Fig 4 – Bajaj Finance, Quarterly Growth of Income, Profits – JainMatrix Investments

The Growth of Total Income, Net Interest Income, Net Profits and EPS TTM has been very steady since June 2008, see Fig 4.

Fig 5 – Price, P/BV ratio, Dividends, JainMatrix Investments

- The Share price has appreciated by 28% CAGR over the last 9 years. However, post the 2009 fall, the appreciation has been very steep at 86% CAGR over 5 years, mapped in Fig 5.

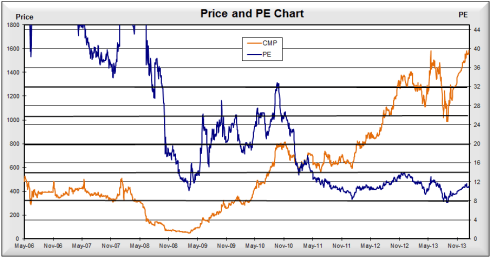

Fig 6 – Price PE chart, JainMatrix Investments

- Price and PE chart Fig 6, indicates that the PE is distributed over a range of 8-32 times, with the 8 year historical average of 20 times.

- It shows that PE is currently near all-time lows even though the Price is at all-time highs. It seems the full effect of the Earnings improvements is not yet reflected in the Price.

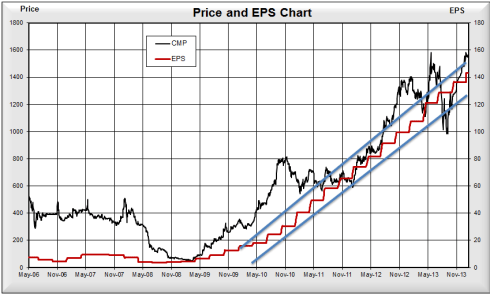

Fig 7 – Price EPS chart, JainMatrix Investments

- The EPS growth has accelerated since 2010, (Fig 7). This is an excellent chart of the firm’s growth. The EPS appears to be in a channel – of blue lines, and on a good growth path.

- Dividend yield by the company is 0.95%. Dividend rate has increased steadily over the last 5 years.

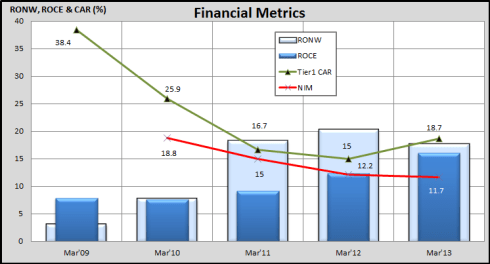

- We can trace the financial metrics of Return on Net Worth, Return on Capital Employed and Tier 1 Capital Adequacy in Fig 8. ROCE is 16% and RONW is 17.6%, in FY13. These are good ratios.

- Today, BFL has a tier-1 capital adequacy ratio at 17.7% (Sept’13). This is at a comfortable level to fund rapid growth and meet the standards for the sector.

- NIM has fallen to 11.7% but this is driven by higher share of secured loan products.

- Gross NPA increased from 1.14% to 1.15% while net NPAs declined from 0.26% to 0.23 % YoY.

Fig 8 – Financial Metrics, JainMatrix Investments

- P/BV is 2.35 today which is a fair level, not overpriced.

- The PEG today is at 0.48 – indicates undervalued status.

Risks:

- Our base case assumes BFL wins the Banking license, and needs to restructure and invest in itself to re-launch as a bank. The share price will surge post this prestigious win. But in case it does not win this, restructuring costs will be lower and profits higher; but the share price may see some fall.

- High Inflation. If the current high inflation in India cannot be tamed, it will affect BFL business.

- Our base case is a mild economic recovery in India. However, if the Indian economy continues to show flat or poor growth, the BFL growth will be hit.

- Promoter driven consolidation. Bajaj group has other financial firms like Bajaj Allianz (Insurance), Bajaj Financial Solutions (Wealth management and advisory) and Bajaj Finserv. Consolidation will change the outlook and business strategy of BFL.

- The worse performing business lines have been Infra and commercial lending, which have been pared down over the last two years. No fresh losses should emerge from this loan book.

Peer benchmarking and Financial Estimates

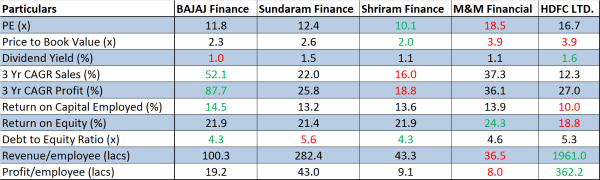

BFL is compared to some of its peers to understand and benchmark its key ratios. See Exhibit 9.

Exhibit 9 – Peer Benchmarking, JainMatrix Investments

- BFL leads in ratios of growth and Returns.

- Behind a national major like HDFC, it leads across most parameters.

- It appears undervalued at Current Market Price.

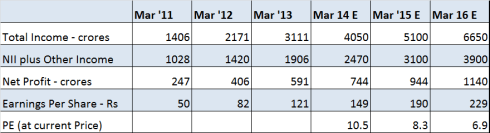

Three-year projections of BFL financials indicate a robust ramp up of revenues and profits, Exhibit 10.

Fig 10 – Financial Projections, JainMatrix Investments

- Review of Projections from the Jan 2012 report on BFL. While the firm actually exceeded our projections for FY12 and the Profits for FY13 were lower by just 9%, we noticed that the volatility in Banking/ NBFC sector pulled down the valuation & price from our estimates by 35% by end FY13.

- In the next 2-3 years, this should reverse and the valuation multiples should rise.

Opinion, Outlook and Recommendation

- Indian market is underserved for loans and financial services. Quick calculations show BFL has 2-3% market share among Indian NBFCs (non-Bank). While small, this indicates a big opportunity for BFL.

- In India, Consumer debt/ GDP is 9%, low compared to S.Korea 80%, European>50% and China 12%.

- BFL is a firm gifted with an outstanding, valuable brand, positive image and good reputation. BFL is well placed to capitalize on this by growing into a financial powerhouse with businesses into insurance, loans and finance.

- In the past few years, BFL has embarked on a business trajectory that, if sustained, can make it a top 5 NBFC in 4-5 years. In essence it may move from mid-cap to large-cap, and shareholders could gain considerably.

- Invest now and systematically for long-term out-performance.

The projection/ targets for Bajaj Finance are:

- March 2015 – Rs 2850 – an 81% gain

- March 2016 – Rs 3435 – an 118% gain

JainMatrix Knowledge Base:

See other useful reports

- Are we in a new Bull Run?

- BF Utilities – This can be a NICE buy

- Repco Home – A Fortune at the bottom of the Pyramid

- Power Grid FPO 2013 – Apply

- Just Dial Ltd – An Equity Research Report

- Future Gazing – Business and the Internet of Things

- Balkrishna Industries – The Tyres Roll Faster

- BHEL – a Power Value Play

- Cairn India – A Formula for Success

- Mindtree Ltd. – A Possible Star

Do you find this site useful?

- Visit the SUBSCRIBE page to find how you can get more. Click LINK

- Register Now to get our Free reports and much more, on the top right of this page, or by filling this Signup Form CLICK.

Disclaimer:

This document has been prepared by JainMatrix Investments Bangalore (JM), and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of JM. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an independent Financial Expert/Advisor. Either JM or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com

Disclosure: It is safe to assume that if the JainMatrix website recommends a stock, the researcher has already invested in it.

")