Preface / introduction

- JainMatrix Investments has been tracking the Indian telecom sector, since the days of BSNL and MTNL monopoly, the go-go days of mobile introduction, the rise of Bharti Airtel and the entire sector over 2000-10 with 5-6 players, the high competition over 2010-14, the consolidation over 2013-18, and the rise of Reliance Jio.

- The mobile sector is still under stress today, reduced to a 4 player industry, including a PSU. Telecom prices are among the lowest in the world, barely supporting their operations.

- Post Covid, telecom services have enabled many people to Work From Home (WFH) and in general stay safe from infection worries. It is critical infrastructure.

- Player #3 is Vodafone Idea (VIL) with a ₹25,000 crore market cap, revenues of ₹45,000 cr. but operating losses in FY20, a book value of ₹6,000 cr. and a CMP of ₹8.6. Mobile subscribers number 31.9 cr.

- VIL has Adjusted Gross Revenue (AGR) dues to Govt. of India (GoI) of ₹50,399 cr. These are either to be paid immediately (impossible) or over a 20 year period (under negotiation and subjudice due to a running court case).

- Let me start with the worst case scenario –

What if Vodafone Idea goes bankrupt:

- The National Company Law Tribunal (NCLT) may have to be brought in to start a painful 2-3 year process of Insolvency and Bankruptcy Code (IBC).

- The AGR dues to GoI of ₹ 50,399 cr. would be struck off. GoI will get next to nothing back.

- The debt of VIL of ₹ 112,520 cr. owed to banks and institutions will become almost worthless, taking down many lending Banks and funding agencies with it. This can be a worse and more painful disaster than the IL&FS collapse a few years ago.

- Vendors are owed at least ₹ 4,000 cr. for equipment, and would start litigation to recover.

- Subscribers numbering 31.9 crores would be affected. Their services will be disrupted and it will be difficult and time consuming to switch providers.

- The 18,500 VIL employees would lose their jobs. A lot of working telecom assets would be damaged, destroyed or wasted.

- India would lose face with the international business community. Another massive loss by a reputed MNC (Vodafone) in India would spoil our Ease of Doing Business ranks

- The TRAI and Telecom department would become perhaps the worst Indian regulator, as along with our Justice system it has overseen the transition of a 14 player healthy telecom sector, to a monopolistic, damaged, in-reality 2 player industry, in a short 10 year period. The mobile penetration in India has also actually fallen in the last 1 year.

- The sector would become a virtually 2 player monopoly with no competition. In such a market the price of mobile services can easily rise 2-5X within 2 years, as surviving telecom firms will have a free hand. TRAI and Dept. of Telecom will not be able to control the rise, just as they have been unable to control the fall of service prices in the last 5 years.

While its expected for some firms to fail in an open economy, VIL failing is clearly a disaster that should not happen.

Whats the solution?

- This solution should be seen as an emergency one time effort, not a solution that can be repeated or generalized for other companies or sectors.

- All AGR dues to GoI should be paid by VIL equally over a 20 year period, with interest.

- The annual AGR dues should be collected by GoI every year in the form of fresh equity issued by VIL at the then value of market capital of the firm. Thus GoI becomes a stakeholder of VIL to the extent of its equity holdings in it and payments due.

- GoI must have a 1 year lock in period for its VIL shareholding and is free to sell the stake thereafter.

Why this solution will work

There are 5-6 major forces at play in this industry.

- The telecom sector in India is at the cusp of recovery. Demand for services like calls and internet data are booming. Prices for mobile services have been depressed, but are on a recovery since Jan 2020. Further recovery will ensure operating health of current providers. If VIL can survive the next 1 year, it has a good chance of becoming financially healthy.

- GoI will get its AGR dues over a period of time. By not demanding AGR dues immediately, VIL may be able to survive. In fact if VIL does well, then GoI may be able to collect more money than the current owed ₹50,399 cr. as the VIL market cap grows. It also helps if GoI starts solving outstanding disputes with industry faster.

- VIL should be able to service its debts from operating revenues. Thus banks and funding agencies do not have to declare this as NPA. This will avert a disaster.

- Customers would be able to continue with VIL without disruption. They may have to pay more, but India cannot stay the cheapest place in the world for mobile services forever.

- Vendors, employees and business partners of VIL can continue unaffected.

- Corporates in India will gain in confidence. Even Reliance Jio and Bharti Airtel should be happy about VIL’s survival. There is ample room for all players to grow.

We have a precedence

Just a few months ago, the RBI stepped in to save Yes Bank from collapse. In an admirable and swift action, the failing bank was recapitalised and the new stake ownership was spread over several PSBs and other investing institutions.

In a similar manner, perhaps more urgently than Yes Bank as this industry has just 4 players, VIL needs to be saved, and given a chance to not just survive but hopefully prosper.

DISCLAIMER

- This document has been prepared by JainMatrix Investments Bangalore (JM), out of public interest. This is our opinion only and we have not communicated with Vodafone Idea, Reliance Industries, Bharti Airtel, TRAI, Dept of Telecom or SC or any other party directly to come to these conclusions.

- Punit Jain discloses that he has no equity ownership or known financial interests in Vodafone Idea Ltd, Reliance Industries or Bharti Airtel or any group company, to the best of his knowledge. He has shares in Yes Bank since 2005. Punit Jain does have a VIL mobile service subscription since over 10 years.

- This report is for information purposes of recipients and not to be used for circulation. This report should not be considered or taken as an offer to sell or a solicitation to buy or sell any security. The information contained in this report has been obtained from sources that are considered to be reliable. However, JM has not independently verified the accuracy or completeness of the same. Neither JM nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein. Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient’s particular circumstances and, in case of doubt, advice should be sought from an Investment Advisor. Punit Jain is a registered Research Analyst under SEBI (Research Analysts) Regulations, 2014. JM has been publishing equity research reports since Nov 2012. Any questions should be directed to the director of JainMatrix Investments at punit.jain@jainmatrix.com.

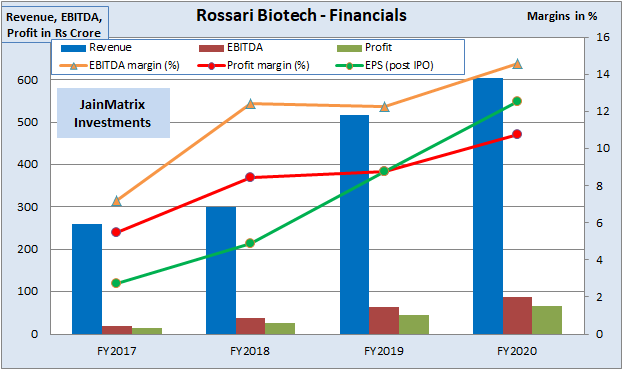

Fig 2 – Free Cash Flows

Fig 2 – Free Cash Flows Fig 3 – Key Product Segments

Fig 3 – Key Product Segments  Fig 4 – Exports

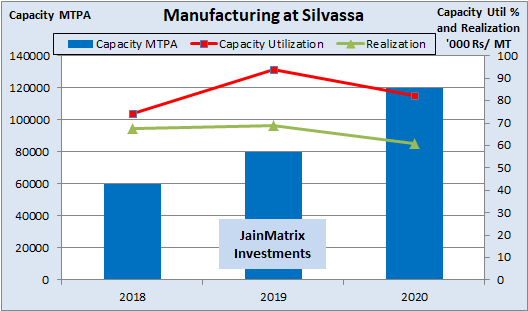

Fig 4 – Exports Fig 5 – Manufacturing

Fig 5 – Manufacturing

Fig 1. CAGR of TRS, source McKinsey & Co

Fig 1. CAGR of TRS, source McKinsey & Co Fig 2. Region wise sales of Chemicals

Fig 2. Region wise sales of Chemicals  Fig 3. Revenue from exports

Fig 3. Revenue from exports