Tag: wealth management

-

Wealth Building and Retirement – the Four Bucket Approach

Summary: The transition from your Working Life and Career to Retirement can be quite demanding. The challenges in this phase extend from psychological to financial and social. In this note, we focus on the financial challenges. The Equity Investor can use the Four Bucket Approach detailed here to think though the changes and plan for…

-

Buying a Car? Here’s the Real Cost

Last week I sold my car. It was a beautiful machine. I bought this Hyundai i10 in 2013. It became the default safe ride for work commutes, local errands and weekend joyrides. Occasionally we travelled intercity in it. Then my son grew old enough, and he learnt to drive in it. He added college commutes…

-

IPOs of Subsidiaries of Listed firms – are Safer and Create Value

20th July 2025 Summary This article investigates a trend in Indian markets — listing of subsidiaries by Corporates that are large conglomerates and sector leaders. Who really benefits from these listings? Are they a source of genuine value creation? To understand this, we map the data on subsidiary IPOs by reputed Indian Corporates between Jul’23…

-

Belrise Industries IPO – Strong as the Chassis

IPO highlights Summary Entire Report in PDF format: Disclaimers and Disclosures

-

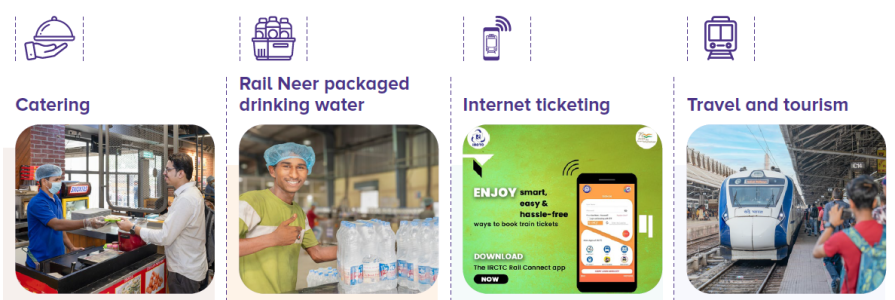

IRCTC Ltd – Navaratna Back on the Rails – BUY

Description and Profile The rest and entire equity research report is available as a PDF, please feel free to download. More such quality reports are available with the JainMatrix Investments paid subscription. PRICING AND PAYMENT OPTIONS Also register for free alerts from JainMatrix Investments, by adding your email on the top right panel here. Disclaimers…

-

Business Standard – Revealing the 100X strategy: ultimate wealth creation

I came across an excellent article on Business Standard. This is very useful for investors new to Equity. Several important concepts are covered here. Do Read – https://www.business-standard.com/economy/analysis/revealing-the-100x-strategy-the-ultimate-instrument-of-wealth-creation-124121701224_1.html Warm regards Punit Jain

-

Mid and Small Cap Stock Trends Nov 2024

27th Nov 2024 JainMatrix Investments, a Research Analyst firm, is pleased to present a note on Mid and Small Cap Market Trends. We have done some research and here are the key findings: Suggestions and Disclaimers